Skip to content

Skip to content Unfortunately, there is content on the internet about CPF that may be misleading. So much so that it is hard for US exposed taxpayers to know what to trust. As one of the few tax firms with “boots on the ground” in Singapore, we feel confident in our ability to deal with those exposed to the tax rules of both Singapore and the US.

- Working in Singapore under a contract of service.

- Employed under a permanent, part-time or casual basis.

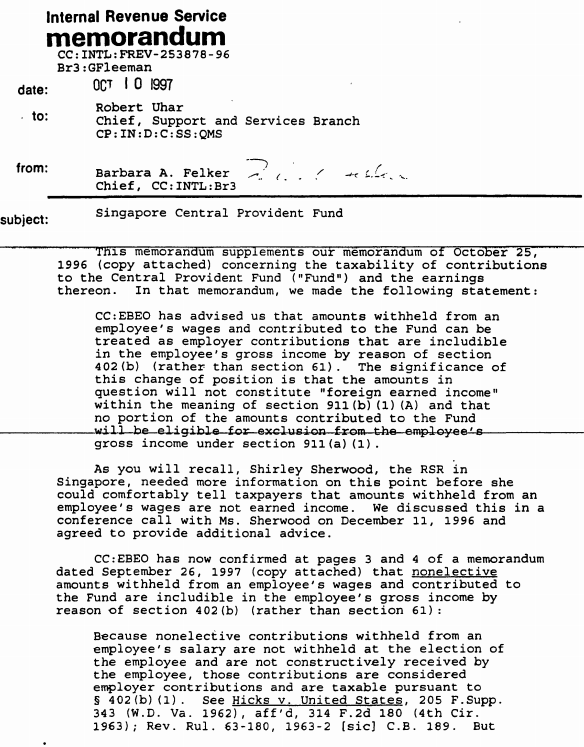

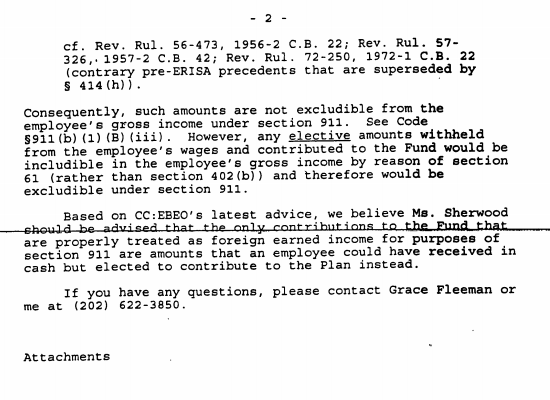

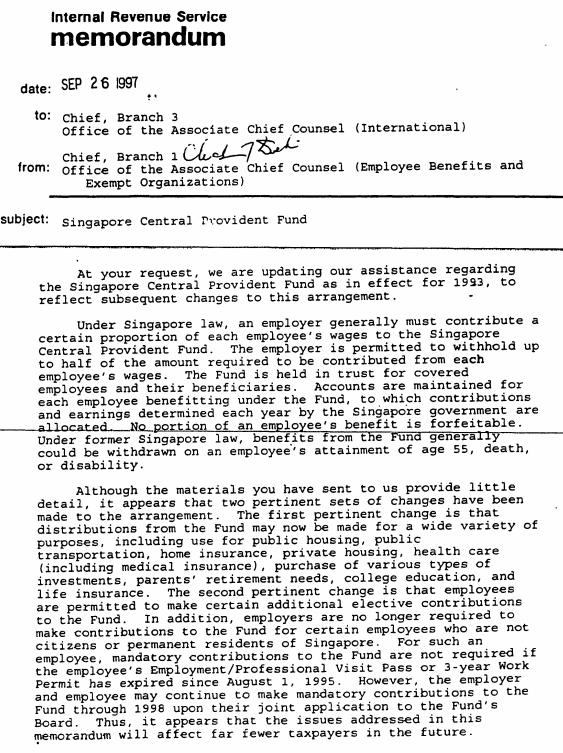

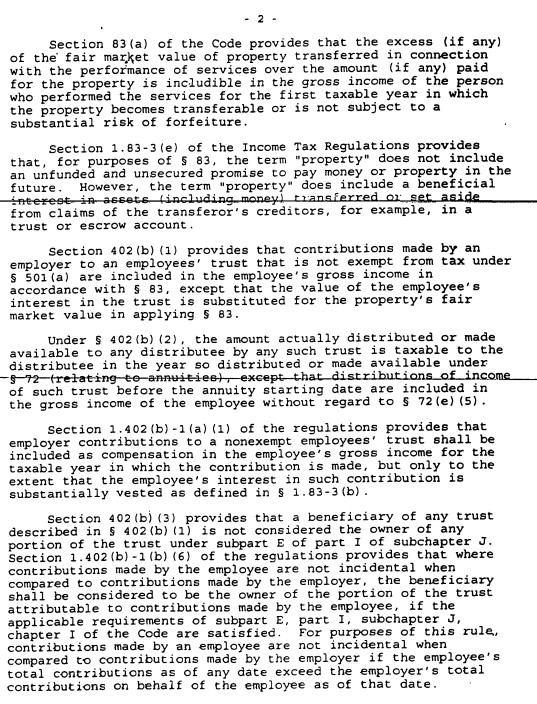

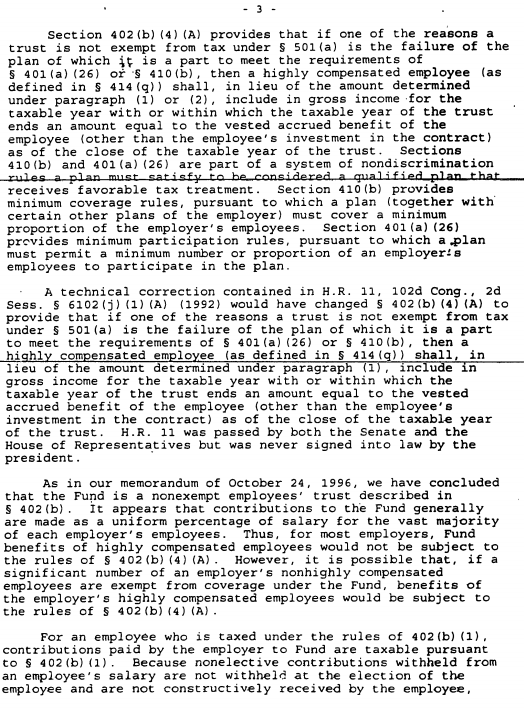

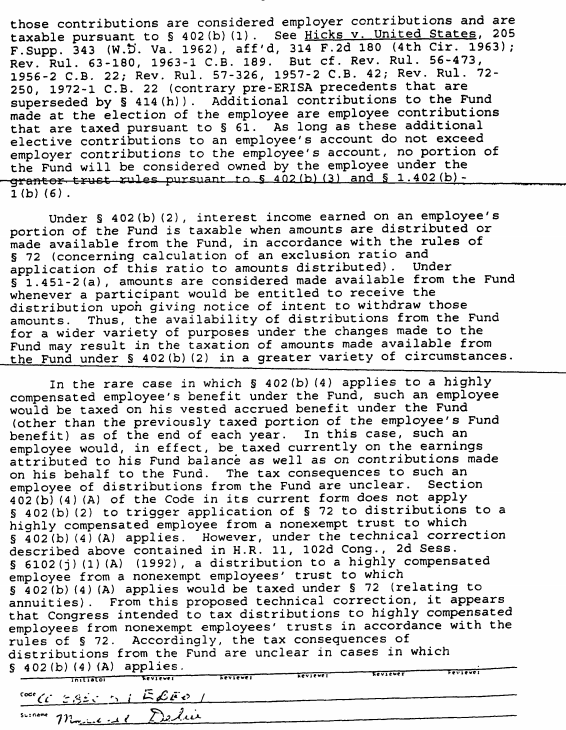

Our position is that Singapore’s CPF is taxable by the US for US exposed persons. Please see the screenshots below in support of our position.

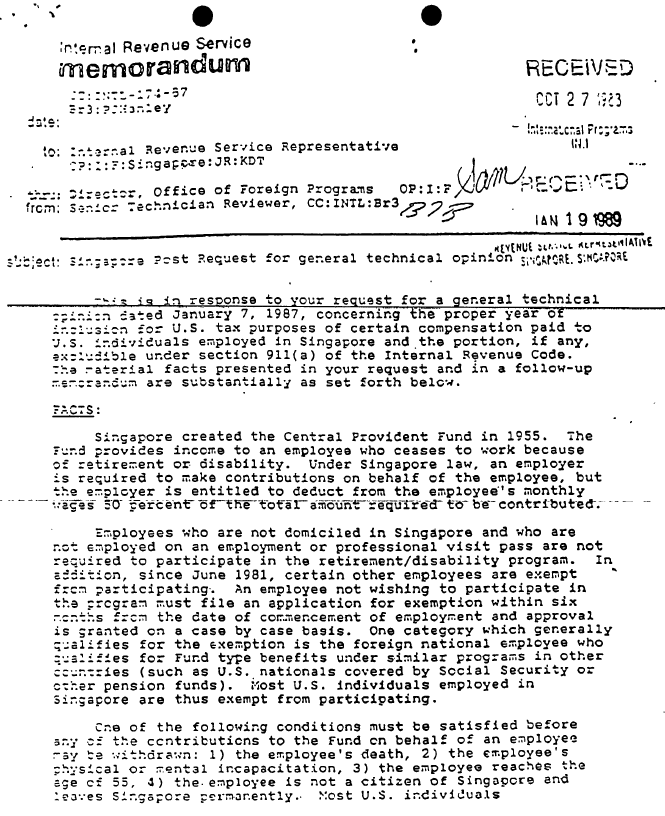

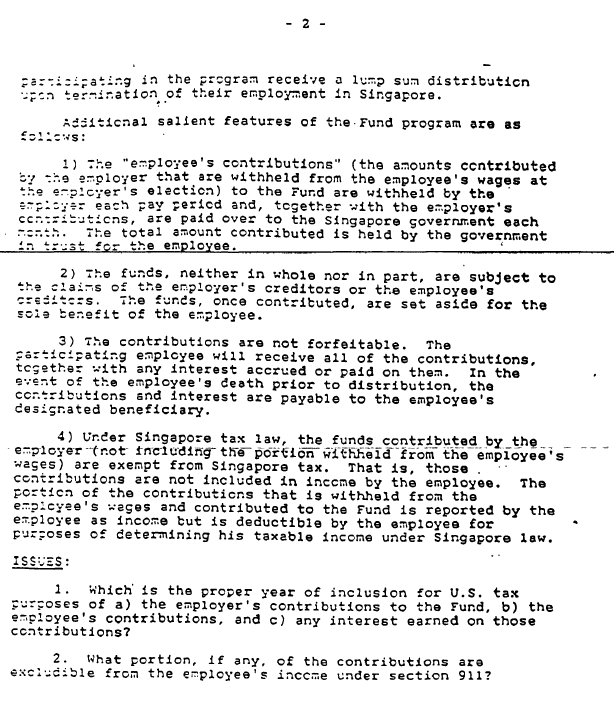

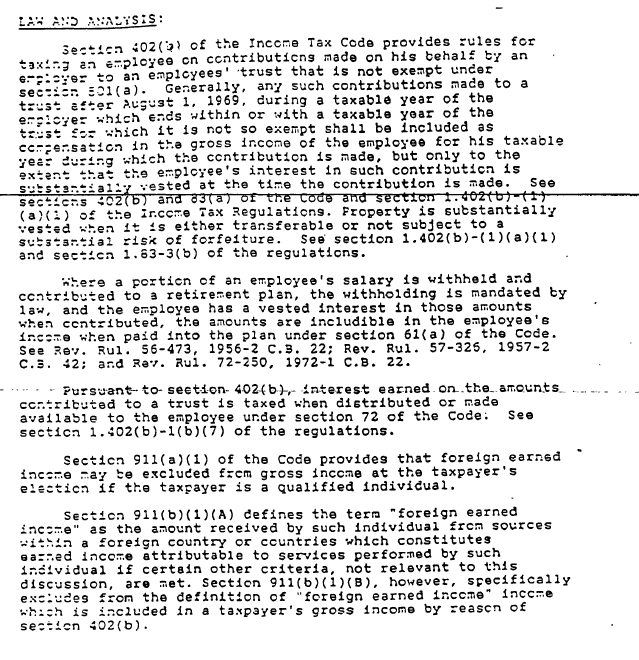

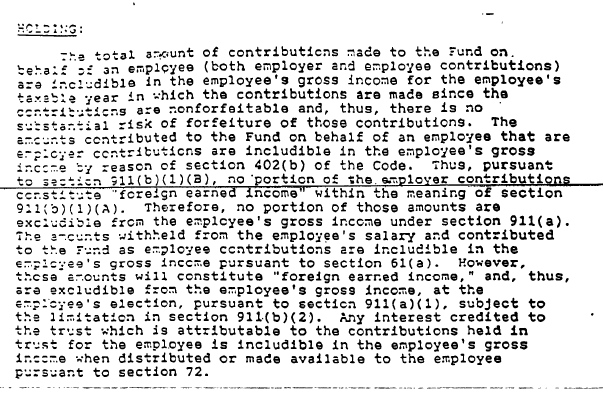

We start with a 1989 memo and continue with a 1997 memo. Be careful when dealing with unqualified professionals with no experience in or with Singapore…

DERREN JOSEPH:

Ma’am,

AUDIENCE:

Can you talk about the CPF in Singapore?

DERREN JOSEPH:

Yeah, there was a lot of uncertainty, but back in the nineties when the IRS had an office at the US Embassy here in Singapore, they put out like a, a paper that clarified everything. So, removed the mystery from it. So essentially they, I, so it’s not deductible first of all. So that much is clear. Not deductible from a US perspective. From Singapore, yeah, us. No, the employer contribution to the CPF is taxable to you from a US perspective. So you add that to your taxable income and yes, it goes on the FinCEN 114 Form, the FBARS. So you do put it and if you add the threshold where you trigger 8938 or the FATCA form, it goes there as well.

DERREN JOSEPH:

The interest. So you get your annual statement from CPF, you just download it December and that goes with your schedule P. So yeah, that’s it.

AUDIENCE:

Can you talk about CPF life?

DERREN JOSEPH:

So that is after tax income.

ATTY. BUTLER SNOW LLP:

So yes, so the growth is taxed, you get a credit for what you already pay taxes on contribution would come up in the Euro contribution but the growth is taxable so you’ll do that. The other thing to keep in mind where it gets really tricky, I mentioned earlier there are rules where the US wants to disincentivize people who have a US tax resident from investing into foreign corporations. So the CFC controlled foreign corporation rules and PFIC passive foreign investment companies. So the CPF itself, as Derren mentioned, there are revenue rulings. We’re gonna treat this like a business trust. Basically you’re gonna pay up on what the employer contributes as if it was like their salary and not deferred like it would be here and then the growth is gonna be income to you when you eventually take it out.

ATTY. BUTLER SNOW LLP:

But the complication is what are they investing in. If it’s like a tax where they’re just paying you out, you’re gonna be okay. But if you start to do any investments like into a fund or or anything like that, those could be CFC or PFIC. And now not only is the growth could be taxable, but it might be only taxed because you might have to throw back to when you originally acquired the foreign fund for the foreign investment that was negatively taxed from the US perspective. So it’s not just the CPF itself, it’s what’s going on below the CPF. You gotta be careful about

AUDIENCE:

What if my CPF is just cash?

ATTY. BUTLER SNOW LLP:

As simple as that. Can’t get still not simple, it’s not like an American, but it is the simplest it can get.

AUDIENCE:

What if I leave Singapore and cash out the CPF?

DERREN JOSEPH:

It’s Tax Income right?

ATTY. BUTLER SNOW LLP:

Generally the amount you’ve already paid us employer contributions up every year, you don’t owe more tax on that. But the growth, that’s a realization that’s cashed out a CPF. Typically while since you’re waiting for later, you’re not having to pay for that growth. But once you leave and it’s kind of cashed out to you and if you roll it over into something else, there isn’t a mechanism. Like there are other parts of the code that allows you to roll over like 401K’s and IRAs and all that. There isn’t such a thing for foreign pensions particularly because there isn’t a particular treaty in place here in Singapore. But even in treaty countries sometimes there’s not a rollover rule for foreign pensions that are written. So in essence you’re gonna have to pay on the game when that happens.

AUDIENCE:

What if I move to a rollover country?

ATTY. BUTLER SNOW LLP:

I’m not aware we’ve to dig into it but I’m not aware of anything that would be retroactively. I think the rule is gonna be about the CPF. There isn’t a treaty that says you gotta rollover. And so I don’t think the rollover… You can go into a rollover from a non rollover, but I’d have to check. We can talk afterwards. I’d like to check to get back to you if it’s a simple answer. If not, you know, it’s a typical thing. People ask me, how much do you charge? And I say a thousand bucks. Two questions. What’s your second question?

DERREN JOSEPH:

On that subject, do you wanna comment on the SRS as well? The Supplemental Restraint System.

ATTY. BUTLER SNOW LLP:

Yeah. Yeah. So those are, I don’t think that’s as absolutely designed and SRS is really, that’s a tricky one to the point that this gentleman is making before he left. So I do SRS for myself and my wife, but I understand I’m not really getting much because every penny I save in Singapore tax is just more tax I’m paying in the US and they won’t let me near anything resembling an investment. So I get like 0.05% interest everywhere on what I use it as is. It’s a nice little, it’s a nice little parkway savings for the tax system, which is incredibly awesome, incredibly easy.

But… second, you are no longer here. It all comes to the bank and so we got that SRS that’s funded at least to the amount you’re now on a manual carrier forward basis. You know you’ve got something you can just turn over to the government rather than you have cash thinking SRS, it’s not tax. So what you’re putting into it is part of your income in the US you’re paying if you’re not getting the break here in Singapore. So, so in essence, think of it like you got two, you got two buckets, this bucket says 38 and that’s the US and this bucket says 21 and Singapore and first you, you fill the 21, then you gotta top up to the 38. But once, once you make an SRS contribution, you reduce bucket one to zero, but you still gotta fill the 38 in the US so it doesn’t really gain from the US.

DERREN JOSEPH:

22?

ATTY. BUTLER SNOW LLP:

22. Yeah.

OUTRO:

So if you’re a six, seven, or eight figure investor, entrepreneur, or business owner who needs a tailor-made solution from a qualified team of professionals, we can help you achieve the international lifestyle, the freedom, and even the tax savings you’re looking for. Visit us@hj.tax and live that international life.