Skip to content

Skip to content What is FIRPTA?

Here’s some information about purchasing real estate in the United States from a foreign owner. People from all over the world invest in United States real estate.

If you’re buying property from a foreign owner, here are some things you need to know.

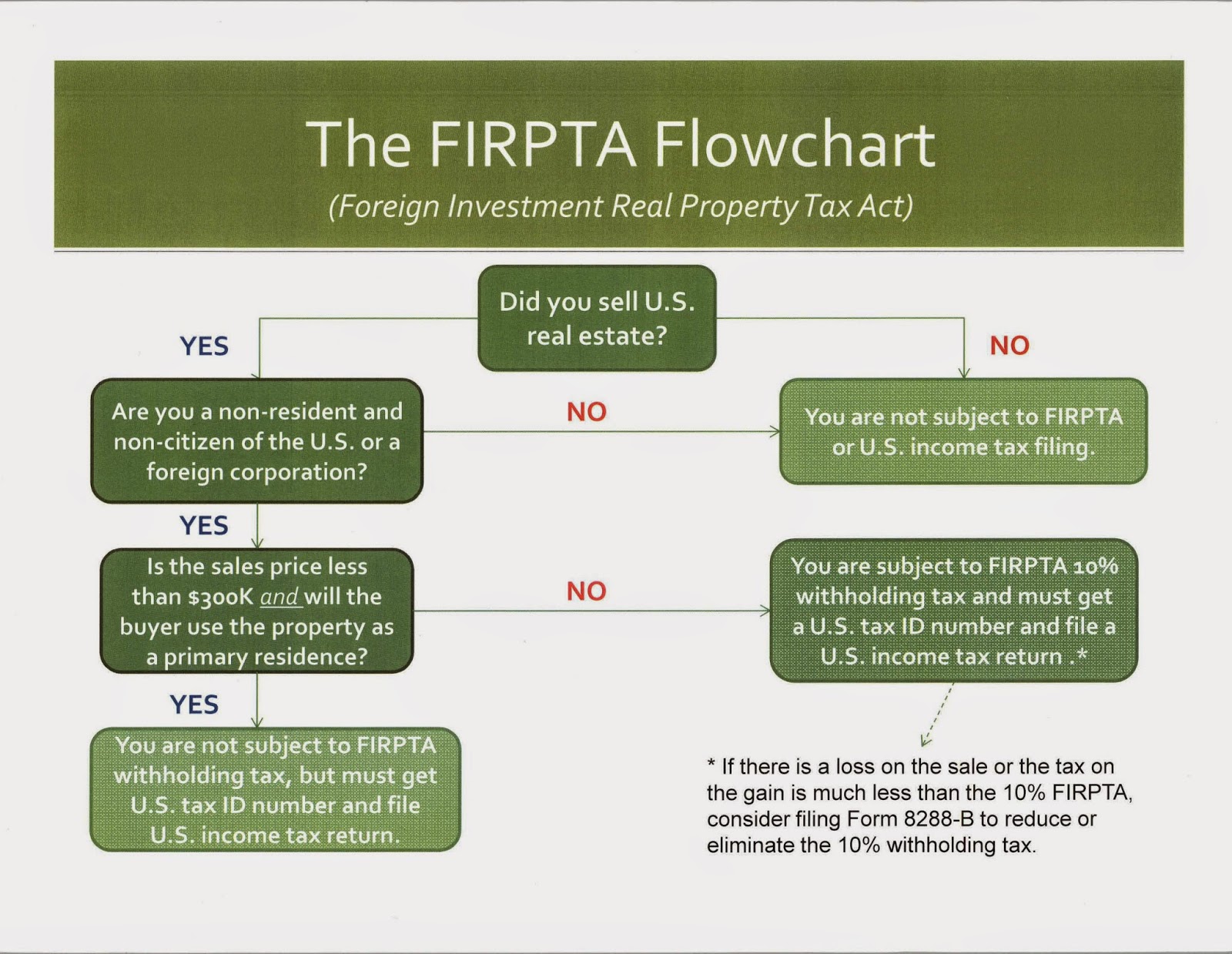

- The Foreign Investment in Real Property Tax Act of 1980, also known as FIRPTA, may apply to your purchase

- FIRPTA is a tax law that imposes U.S. income tax on foreign persons selling U.S. real estate.

- Under FIRPTA, if you buy U.S. real estate from a foreign person, you may be required to withhold 10% of the amount realized from the sale.

- The amount realized is normally the purchase price.

- The withholding is how the IRS collects U.S. tax owed by foreign sellers.

A U.S. real property interest is an interest, other than as a creditor, in real property (including an interest in a mine, well, or other natural deposit) located in the United States or the U.S. Virgin Islands, as well as certain personal property that is associated with the use of real property (such as farming machinery). It also means any interest, other than as a creditor, in any domestic corporation unless it is established that the corporation was at no time a U.S. real property holding corporation during the shorter of the period during which the interest was held, or the 5-year period ending on the date of disposition (applicable periods).

An interest in a corporation is not a U.S. real property interest if:

Such corporation did not hold any U.S. real property interests on the date of disposition, All the U. S. real property interests held by such corporation at any time during the shorter of the applicable periods were disposed of in transactions in which the full amount of any gain was recognized, and For dispositions after December 17, 2015, such corporation and any predecessor of such corporation was not a RIC or a REIT during the shorter of the applicable periods during which the interest was held.

Here’s how FIRPTA works. FIRPTA example

- If the law applies to your purchase, then within 20 days of the sale, you are required to file Form 8288 with the IRS.

- Along with the form, you submit 15% withholding.

- It is important to know about FIRPTA, because if you do not withhold the required amount, file the form on time, and submit the withholding, penalties do apply.

- There are some exceptions. For example, FIRPTA law does not apply if you are buying a residence for $300,000 or less or the property is not a U.S. real property interest.

Below are 3 ways that we can help you…

1. Do you Need an ITIN? We can help

For many foreign investors, their advisors are experienced in international US tax matters so they do not have an ITIN. We are IRS Certified Acceptance Agents and listed on the IRS website – https://www.irs.gov/individuals/international-taxpayers/acceptance-agents-singapore

So we are certified, duly qualified and recognised to assist international real estate investors with matters related to ITIN applications – https://htj.tax/2016/02/so-you-need-itin/, https://htj.tax/2017/08/itin-update/

2. FIRPTA Withholding Certificate? We can help

According to IRS.gov, the withholding amount on the sale of US property can be adjusted if the IRS issues a withholding certificate. A withholding certificate is an application for a reduced withholding based on the gain of a sale instead of the selling price.

If 15% of the selling price is more than the tax you will owe on this sale, then a withholding certificate may be ideal for you.

Important features to know about withholding certificate applications:

- If the withholding certificate can’t be applied for and issued prior to closing, then typically the buyer gets to decide if the funds need to be remitted within 20 days of the closing or if they can remain in escrow pending the approval or rejection of the application.

- The IRS will generally act on these requests within 90 days after receipt of a complete application

- All parties must have or at least apply for a US tax ID for a withholding certificate

- The applicant must be able to prove their basis in the property

- The transferee, the transferee’s agent, or the transferor may request a withholding certificate.

- A transferor that applies for a withholding certificate must notify the transferee in writing that the certificate has been applied for on the day of or the day prior to the transfer.

Read more here – https://htj.tax/2020/01/foreign-investors-in-us-real-property/

3. Remit FIRPTA Withholding Tax? We can help

The sale of US real property by a foreign person is subject to the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA) income tax withholding.

Persons purchasing US real property from foreign persons, certain purchasers’ agents, and settlement officers are generally required to withhold 15% of the amount realized on the sale or disposition. In most cases, the transferee/buyer is the withholding agent. According to IRS.gov, if you are the buyer of US real property, you must find out if the seller is a foreign person. If the transferor is a foreign person and you fail to withhold, you may be held liable for the tax.

The transferee must deduct and withhold a tax on the total amount realized (usually the gross selling price) by the foreign person on the disposition. The rate of withholding generally is 15%.

Transferees must use Forms 8288 and 8288-A to report and pay to the IRS any tax withheld on the acquisition of US real property. This form must be submitted with the required withholding within 20 days of the date of transfer. It is critical for these forms to be prepared correctly as this is the only record the seller will have as proof of funds paid on their account.

In view of the frenzy in the profession over compliance with the new FATCA rules, it seems appropriate to take an overview of how FATCA applies to a major source of inbound investment by foreign individuals – “FIRPTA” investments in U.S. real property. This commentary considers the extent to which FATCA might apply to the most common structures that are used. What is most striking, however, is that the FATCA rules provide for explicit exceptions for a substantial portion of FIRPTA – related income.

It is assumed in this commentary that the investment in U.S. real property is made by an individual who is a nonresident alien (NRA) for U.S. income tax purposes, and a “nonresident not a citizen of the United States” (i.e., a non-U.S.-domiciled alien) for U.S. estate and gift tax purposes. The following structures are examined in this commentary: (1) direct investment in U.S. real property by the NRA; (2) investment through a directly owned “United States real property holding corporation” (RPHC); (3) investment through a directly owned foreign corporation (FC) that owns the U.S. real property in its own name through a U.S. “branch”; (4) investment through an FC that in turn owns a U.S. subsidiary (an RPHC) which holds the U.S. property; (5) direct or indirect investment in U.S. real property by a nongrantor foreign trust that was created in the past by an NRA; and (6) direct investment by a foreign partnership.1

In examining how the FATCA rules apply to FIRPTA investments, three special FATCA rules must be kept in mind. First, the FATCA rules do not apply to income realized directly by individuals (in this case, NRAs), but only to income realized by foreign entities such as foreign corporations, foreign partnerships, and foreign non grantor trusts.2 Second, there is an exception from the definition of “with-holdable payment” for U.S.-source rents, whether from the rent of U.S.-situs real property or from the rent (lease) of U.S.-situs tangible personal property (for example, of furniture and fixtures that are rented out as part of the rental of the real property in which they are located), and this exception also applies after 2016 (when the FATCA rules on withholding on gross proceeds take effect) to gross proceeds from the sale of property that does not generate U.S.-source interest or dividends but only rental income (either actual or hypothetical). Finally, there is a broad exception for transactions that are subject to the §1445 FIRPTA withholding tax rules (although the regulations are still much too scanty on this point), an exception that will also be important after 2016.

In the discussion below, it is assumed that the U.S. real property may or may not be rented out (thus, it might be used as a personal residence by the ultimate NRA investor and never rented out); that it might be subject to a mortgage extended by a foreign lender; and that the property is eventually sold either directly by the NRA investor, by an entity that the NRA controls directly or indirectly, or (in the case of a non-grantor foreign trust) by an entity that was at one time created by an NRA. The reader should always be cognizant of the possible overlap between the “chapter 3” withholding rules in §1441/§1442 and the “chapter 4” FATCA withholding rules.

1. Direct Investment by the Foreign Individual

Because FATCA only applies to foreign entities, no FATCA compliance is required from the individual with respect to either rents that he/she may receive from the property, or gross proceeds from the sale of the property. However, the rents are subject to gross 30% withholding under §1441 (subject to possible treaty reduction) unless the NRA owner provides Form W-8ECI to the lessee in order to establish that the rental income is taxed on a net basis as effectively connected income (ECI). When the property is sold, the withholding provisions of §1445 must be complied with; thus, up to 10% withholding tax may be imposed on the gross proceeds from the sale.

If the individual borrows funds from a foreign lender and if the property generates rental income that is ECI, the related interest expense will usually be deductible under §873. However, where the borrower is an NRA, interest paid by the NRA nevertheless is still classified as foreign-source income under §861(a)(1), and thus no withholding is imposed under either chapter 3 or chapter 4.4 Thus, it will usually not be necessary for the parties to try to structure the loan as “portfolio debt” for purposes of §871(h) or §881(c).

2. Direct Investment in an RPHC

If the U.S. property is owned by an RPHC that is directly owned by the NRA and if the U.S. property is rented out by the RPHC, FATCA will not apply because the lessor is a domestic entity and not a foreign entity. Similarly, if the RPHC pays dividends to the foreign individual, FATCA will not apply because the shareholder is an individual and not an entity, although the NRA would need to give the RPHC Form W-8BEN in order to comply with §1441. Finally, FATCA will not apply when the property is eventually sold, whether that occurs by having the RPHC sell the property and then liquidate, or the NRA sells the RPHC stock. Although the FIRPTA withholding provisions of §1445 (if applicable) would need to be complied with, FATCA would not apply because the foreign shareholder who owns the RPHC is an individual and not an entity.

If, however, the RPHC borrows funds from a foreign lender that is an entity, the interest expense will usually be classified as U.S.-source “fixed or determinable annual or periodical” income (FDAP), and thus potentially subject to withholding under §1441/§1442. If the foreign lender is an individual, no FATCA compliance will be required, although the chapter 3 withholding rules must still be satisfied. However, if the foreign lender is an entity, FATCA compliance may be required — even if the interest is exempt from chapter 3 withholding as “portfolio interest” — unless the interest happens to be paid on a pre-July 1, 2014 “grandfathered obligation.”6Repayment of the principal could also be subject to 30% gross FATCA withholding after 2016 unless the foreign lender has provided the RPHC borrower with proper FATCA documentation.

3. Investment Through a Foreign Corporation (FC) with a U.S. Branch

Because FC is an entity and not an individual, it is potentially subject to FATCA on income that would clearly be exempt from FATCA if realized directly by its NRA shareholder. However, if the property is rented out, the rental income is exempt from FATCA because rents (whether from real property, or from tangible personal property such as furniture and fixtures) are not “withholdable payments” for FATCA purposes. FC should nevertheless comply with the chapter 3 (§1442) rules, usually by making a §882(d) “net election” in order to ensure that the rental income is taxed on a net basis as ECI and by providing the lessee with Form W-8ECI.7

If FC has borrowed from a foreign lender and if the related interest expense is deductible in calculating ECI, the interest is usually classified as U.S.-source FDAP that is not ECI and is subject to the chapter 3 withholding rules. However, FATCA compliance is only necessary if the foreign lender is an entity and not an individual. As noted above, failure to comply with the FATCA rules could result in a 30% tax under chapter 4 even if the interest is exempt from chapter 3 withholding as “portfolio interest,” and after 2016 the repayment of the loan could be subject to 30% FATCA tax on the amount of the gross repayment.

If FC becomes subject to the U.S. “branch tax” under §884, no chapter 3 or chapter 4 withholding rules will come into play on the deemed dividends, because the tax is self-assessed.

When FC eventually sells the U.S. property, it will be subject to the FIRPTA withholding rules of §1445. However, because FATCA withholding on gross proceeds (after 2016) applies only to assets that generate dividends or interest7 (and not rents), FATCA compliance should not be required.

4. Investment Through an FC with an RPHC Subsidiary

If the investment is made through a “two-tier” structure – through a foreign corporation (FC) which is owned by the NRA, and which in turn owns a U.S. RPHC subsidiary (DS), additional FATCA rules can come into play.

Although any rents that are paid to DS are not subject to potential withholding under chapter 3 or 4 (because DS is a U.S. corporation), if DS pays dividends to FC, FATCA compliance is required. However, if FC is located in a “tax haven,” as is frequently the case, the failure to comply with FATCA will result in the same 30% dividend withholding tax under chapter 4 that applies under chapter 3.8 If FC is located in a country whose tax treaty with the United States results in a lower U.S. withholding rate on U.S.-source dividends, compliance with FATCA will usually be advisable in order to obtain the lower treaty rate. As noted above, if DS pays interest to a foreign lender that is an entity and not an individual, FATCA compliance would be required.

When FC eventually sells or liquidates DS, the transaction will be potentially subject to the §1445 FIRPTA withholding rules. In this case, the FATCAexception for the sale of U.S. real property (mentioned above) will not apply, because the asset that is sold is stock that can produce U.S.-source dividends.9 Thus, after 2016 the gross proceeds from the disposition of the RPHC stock are potentially subject to 30% FATCA withholding. However, the FATCA regulations provide for an exception for amounts that are “subject to withholding under section 1445.”10 Unfortunately, the FATCA regulations on this point are extremely scanty. Presumably, however, if the FIRPTA “cleansing” rule of §897(c)(1)(B) applies so that DS ceases to be an RPHC immediately after selling all of its U.S. real property, §1445 will not apply to the disposition of the DS stock. Thus, after 2016 the sale or liquidation of DS could be potentially subject to 30% FATCA withholding if there is no FATCA compliance on the part of FC.

5. Investment by a Non-grantor Foreign Trust

If the U.S. property is directly owned by a non-grantor foreign trust,11 the FATCA results are similar to those that apply to direct investment by an NRA (see 1, above). Thus, rental income is exempt from FATCA (although subject to potential §1441 withholding). If the trust pays interest to a foreign lender that is deductible under §873 in calculating tax on ECI from the rental income, the interest is foreign-source and thus exempt from withholding under both chapters 3 and 4, because the trust is not a U.S. “resident.” Finally, if the property is eventually sold at a gain, the sale is exempt from FATCA because the asset that is being sold does not generate U.S.-source dividends or interest12 (see 3, above).

If instead the foreign trust owns the U.S. property through a directly owned RPHC, through a directly owned FC with a U.S. branch, or through a two-tier structure (i.e., through a directly owned FC with an RPHC subsidiary) – rules similar to those described above for an NRA who uses one of these structures would apply, but with a few differences in the case of a directly owned RPHC. Where the foreign trust directly owns RPHC stock, any dividends that the RPHC pays to the trust are subject to FATCA (as well as chapter 3), because the trust is an entity and not an individual. Similarly, the eventual sale of the RPHC stock by the trust is subject to FATCA after 2016, although the exception for transactions that are “subject to withholding under section 1445” may apply. In both situations, the trust may need to comply with the more extensive compliance rules that apply to “foreign financial institutions” (FFIs) under §1471, if the trust is “managed” by a trustee or advisor that is itself an FFI.

6. Investment by a Foreign Partnership

This structure assumes that the NRA invests in U.S. property through a foreign partnership, but in order to protect the partnership interest from potential U.S. estate tax, the property is never rented out and the foreign partnership is not otherwise engaged in a U.S. trade or business.13 If the partnership pays interest to a foreign lender, the interest is usually not U.S.-source because the partnership is not “resident” in the United States (because it is not engaged in a U.S. trade or business). Thus, it is generally exempt from withholding under both chapters 3 and 4.

If the partnership itself sells the U.S. property, the fact that the property is not an asset that could generate interest or dividends would protect it from FATCA withholding after 2016. However, the partnership would need to comply with the §1445 withholding rules. If instead the NRA sells the partnership interest, FATCA would not apply because the seller is an individual and not an entity, although in this case as well the NRA would need to comply with §1445.

This commentary also will appear in the October 2014 issue of the Tax Management International Journal. For more information, in the Tax Management Portfolios, see Caballero, Feese, and Plowgian, 912 T.M., U.S. Taxation of Foreign Investment in U.S. Real Estate, Tello, 915 T.M., Payments Directed Outside the United States — Withholding and Reporting Provisions Under Chapters 3 and 4, Nauheim, Cousin, Ewell, Limerick, Lakritz, and Lee, 6565 T.M., FATCA — Information Reporting and Withholding Under Chapter 4, and in Tax Practice Series, see ¶7140, Foreign Persons — FIRPTA, and ¶7170, U.S. International Withholding and Reporting Requirements and FATCA.

Copyright©2014 by The Bureau of National Affairs, Inc.

1 For a discussion of all of these structures, see Bissell, 903 T.M., Tax Planning for Foreign Investment into the United States by Foreign Individuals, at X. See also Caballero, Feese, and Plowgian, 912 T.M., U.S. Taxation of Foreign Investment in U.S. Real Estate.

2 It should be cautioned, however, that if an individual owns securities or other assets that are held in nominee form through a “foreign financial institution” (FFI) or through a “non-financial foreign entity” (NFFE), the FATCA rules apply even though the beneficial owner of the underlying asset and the income that it generates is an individual.

3 Although a direct investment in U.S. real property is potentially subject to U.S. federal estate tax if the value of the property at death exceeds $60,000, the U.S. property may be partially or completely exempt from U.S. estate tax if the alien is resident in a country whose estate tax treaty with the United States has an enhanced unified credit with a worldwide exemption of up to $5,340,000 (2014 amount). See the Canada-U.S. Income Tax Treaty, and the U.S. estate tax treaties with Australia, Finland, Greece, Ireland, Italy, Japan, Norway, South Africa, and Switzerland.

4 The reason is because interest paid by an individual is U.S.-source income under §861(a)(1) only if it is paid by a “resident” of the United States. Thus, even though an NRA is engaged in a trade or business within the United States and incurs interest expense that is fully deductible under §873, the interest income remains foreign-source income in the hands of the lender, whether the lender is a U.S. or a foreign person. See Blessing and Lubkin, 905 T.M., Source of Income, at II.D.1. See also Reg. §1.861-2(a)(2).

5 Although the RPHC stock is potentially subject to U.S. federal estate tax if the value of the stock at death exceeds $60,000, the estate tax may be reduced or eliminated as a result of the enhanced unified credit under the estate tax treaties cited in n. 3, above. In addition, the U.S. estate and gift tax treaties with Austria, Denmark, France, Germany, the Netherlands, and the United Kingdom provide for a broad U.S. estate tax exemption for U.S.-situs intangible property (such as stock in a U.S. corporation, whether or not it is an RPHC), regardless of the value of the company at death. See Bissell, 903 T.M., Tax Planning for Portfolio Investment into the United States by Foreign Individuals, at II.E.4.a.

6See Bissell, Foreign `Blocker’ Corporations with No FATCADocumentation: What Happens Now?” 43 Tax Mgmt. Int’l J. 488 (Aug. 2014).

7 Because a §882(d) net election only applies to rents from “real property,” the election technically would not apply to income from the lease of tangible personal property (such as furniture and fixtures). Thus, rental income from tangible personal property is only taxed on a net basis under §882 if on the basis of the actual facts the income is ECI.

7 §1473(1)(A).

8See Bissell, Foreign `Blocker’ Corporations with No FATCA Documentation: What Happens Now? 43 Tax Mgm. Int’l J. 488 (Aug. 2014).

9 §1473(1)(A)(ii).

10 Reg. §1.1445-6(c)(1). The question remains whether a FATCA exemption applies where the foreign person disposing of the RPHC stock obtains a “withholding certificate” that exempts the disposition from any §1445 withholding tax, or where the disposition is otherwise exempt from §1445. It is also not clear whether this exception applies if the disposition is “subject to withholding under §1445” but if the parties fail to comply with the §1445 rules.

11 This structure has become more common in recent years, because the maximum 20% long-term capital gains rate from the sale of the property is lower than the regular corporate income tax rates of up to 35% that are imposed if the property is owned by a U.S. or foreign corporation and is sold at a gain. At the same time, if properly structured and operated, the trust usually protects the NRA grantor from potential U.S. estate tax with respect to the underlying U.S. property.

12 §1473(1)(A).

13See Bissell, 903 T.M., Tax Planning for Foreign Investment into the United States by Foreign Individuals, at X. See also Caballero, Feese, and Plowgian, 912 T.M., U.S. Taxation of Foreign Investment in U.S. Real Estate.

Source: http://www.bna.com/fatca-meets-firpta-n17179895768/

Note: The above reference link was live, but it has since been taken down.

We have helped thousands of foreigners who have invested in US Real Estate as they seek to understand their US tax reporting responsibilities. Allow us to help you as well?

Frequently Asked Questions

Question 1: If a U.S. real property interest (USRPI) is jointly owned by spouses, one foreign person and one U.S. person, and the USRPI is disposed of, may the spouse who is a U.S. person report 100% of the amount realized from the disposition and the spouse who is a foreign person report 0% of the amount realized to avoid the withholding required under Internal Revenue Code section (IRC) 1445?

No, the amount realized cannot be allocated entirely to one transferor when two or more transferors own the USRPI.

If one or more foreign persons and one or more U.S. persons jointly dispose a USRPI, the amount subject to withholding under IRC 1445 is determined in the following manner:

- The amount realized is allocated among the transferors based on their capital contributions to the USRPI. For this purpose, a husband and wife are treated as having contributed 50% each.

- The transferee/buyer withholds on the total amount allocated to foreign transferor(s).

- The amount of credit for the withholding to be allocated to each foreign transferor is allocated in accordance with the foreign transferors’ agreement. The foreign transferors must request that the withholding be credited as agreed upon by the 10th day after the date of transfer. If no agreement is reached, the transferee will credit the withholding by evenly dividing it among the foreign transferors.

Question 2: In the situation where a U.S. real property interest (USRPI) held in the name of a grantor trust is disposed of and the grantors are a married couple, one U.S. person and one Foreign person, is withholding under IRC 1445 required?

Yes, withholding under IRC 1445 is applicable in situations where a USRPI held in the corpus of a grantor trust is disposed of when a Foreign person is considered a grantor with respect to all or a part of the USRPI. Based on the grantor trust rules (IRC 671 through IRC 678), an individual is the grantor of the asset(s) he or she contributes to the corpus of a trust that he or she is determined to still have control over under the grantor trust rules.

For example, if a USRPI is purchased equally by a husband, who is a U.S. person, and wife, who is a Foreign person, in their names and then contributed to the corpus of a trust. After the contribution, the husband and wife are determined to still have control over the USRPI under the grantor trust rules. Then the husband and wife are considered grantors, each owning 50% of the USRPI. So, for the purposes of IRC 1445, when the USRPI is disposed of, withholding would be applicable to the foreign spouse’s 50% of the sales proceeds.

Additionally, if a USPRI is purchased in the trust’s name from monies contributed to the trust in equal amounts by both the husband and wife (one U.S. person and one foreign person) and both spouses are considered to be grantors of the monies contributed to the trust used to purchase the USRPI, then both spouses are grantors of the USPRI once it is purchased. In the case, for purposes of IRC 1445, when the USRPI is disposed of, withholding would be applicable to the foreign person’s 50% of the sales proceeds.

Question 3: In which year does a transferor/seller report the disposition of a U.S. real property interest (USRPI) on their income tax return if the date of transfer shown on the Form 8288-A is the subsequent year to the year the USRPI was actually transferred due to a withholding certificate request being filed in the year of the actual disposition but the determination by the IRS is not made until the subsequent year?

When a transferor/seller disposes of a USRPI, it should be reported, for income tax purposes, in the year the disposition occurred. The date of disposition on the Copy B of Form 8288-A, Statement of Withholding on Dispositions by Foreign Persons of U.S. Real Property Interests PDF, may be different than the actual date of disposition in the situation where a withholding certificate request is made. In these situations, the Internal Revenue Service (IRS) is required to change the date of disposition on the form to the date of the withholding certificate request approval or denial letter sent to the requester.

For example, a transferor/seller sends the IRS a request for a withholding certificate on December 10, 2018 for a disposition of a USRPI that is to take place on December 15, 2018. The IRS reviews the request and issues the withholding certificate denial letter on March 10, 2019. Although the actual date of the disposition is December 15, 2018, the date of disposition on Copy B of Form 8288-A would be March 10, 2019, the date of the denial letter. However, the transferor/seller is required to report the disposition on her or his 2018 income tax return as the actual date of the disposition is December 15, 2018.

Question 4: Is withholding under IRC 1445 applicable in the situation where a foreign person enters into a contract to purchase a U.S. Real Property Interest (USRPI) from another person but assigns the right to purchase the USRPI to a third person before the contract’s closing date on the contract?

Withholding under IRC 1445 is applicable when a foreign person assigns their right to purchase a USRPI to another party.

For example: withholding under IRC 1445 is applicable if a foreign person (FP) signs a contract to buy a house in State A from a builder for $400,000 with a closing date of January 31, 2020. Before January 31, 2020, FP decides to sell the right to purchase the house for $30,000 to another individual (WH). WH is required to withhold $4,500, 15% of the of $30,000 amount realized by FP, and remit it to the Internal Revenue Service with Forms 8288, U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests, and 8288-A, Statement of Withholding on Dispositions by Foreign Persons of U.S. Real Property Interests.

Question 5: Does the exclusion of gain from the sale of a personal residence, under IRC 121, apply to nonresident aliens (NRAs)?

The exclusion of gain for the sale of a personal residence under IRC 121 may apply to NRAs when they sell their U.S. personal residence. Because NRAs cannot file joint returns unless they are married to U.S. persons, NRAs would need to take their own share of the principal residence exclusion amount on separate tax returns. Consequently, the maximum amount of excludable gain for NRAs that file Form 1040NR, U.S. Nonresident Alien, is $250,000. For the exclusion to apply, NRAs would have to meet the eligibility test required for the exclusion. To determine if a nonresident alien meets the Eligibility Test, you can review the five steps of the Eligibility Test in Publication 523, Selling Your Home, as well as review Topic No. 701, Sale of Your Home.

If an NRA qualifies to claim the IRC 121 exclusion, the statutory withholding under IRC 1445 on the amount realized from the sale could exceed the maximum tax liability on the sale. Therefore, an NRA may request a withholding certificate from the Internal Revenue Service to provide to the buyer. The withholding certificate would allow the buyer (through escrow/closing agent) to withhold tax at an approved reduced rate.

Question 6: How is it determined whether a U.S. Real Property Interest (USRPI) is acquired by the transferee/buyer to be used as a “residence” in order to meet the reduced withholding under IRC 1445 when the amount realized is between $300,000 and $1 million or the exception from withholding when the amount realized is $300,000 or less?

In order for a USRPI to be considered a “residence” of the transferee/buyer for the reduced or eliminated withholding, one or more transferees/buyers have to have definite plans to reside at the USRPI for at least 50 percent of the number of days that the property is used by any person during each of the first two 12-month periods following the date of transfer. The number of days that the property will be vacant is not taken into account in determining the number of days such property is used by any person. A transferee/buyer shall be considered to reside at a property on any day on which a member of the transferee/buyer’s family, including brothers and sisters (whether whole or half-blood), spouse, ancestors and lineal descendants, resides at the property.

For example, a transferee/buyer (BUYER) purchases, in her name only, a USRPI for $299,000 and states she is going to reside in the USRPI. BUYER is not married but has an adult daughter. The property is purchased on January 1, 2017. BUYER and her daughter live in the USRPI together through the end of April 2017. On May 1, 2017, BUYER takes a temporary position overseas where she lives for 8 months while her adult daughter lives in the USRPI. BUYER returns on January 1, 2018 and lives in the USRPI with her daughter until May 31, 2018 when BUYER takes another temporary overseas job until February 22, 2019.

Although BUYER only resided at the USRPI for approximately 33% of the days during 2017 and 42% of the days during 2018, her daughter resided there 100% of the days during 2017 and 2018. Therefore, the USRPI is considered a “residence” of BUYER for 2017 and 2018.

Question 7: If a transferee/buyer purchases a U.S. Real Property Interest (USRPI) from a foreign person for $300,000 or less and plans to use the USRPI as their personal residence for the next two years but does not fulfil this requirement over the two years, what actions are required of the transferee/buyer with respect to withholding?

If a transferee/buyer of a USRPI fails to withhold from the amount realized in reliance upon the exception that the transferee/buyer planned on using the USRPI as a personal residence for the next two years, but did not in fact reside at the USRPI for the minimum required time, the transferee/buyer shall be liable for the failure to withhold (if the transferor/seller was a foreign person and did not pay the full U.S. tax due on any gain recognized upon the transfer). However, if the transferee/buyer establishes that the failure to reside the minimum number of days was caused by a change in circumstances that could not reasonably have been anticipated at the time of the transfer, then the transferee/buyer shall not be liable for the failure to withhold.

Question 8: When may the Internal Revenue Service (IRS) change the date of transfer that a withholding agent designated on Forms 8288 and 8288-A?

The IRS may change the tax year designated on Form 8288, U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests, and Form 8288-A, Statement of Withholding on Dispositions by Foreign Persons of U.S. Real Property Interests, if the tax year originally entered was incorrect. This could be because the date was the wrong transfer date or there was a withholding certificate request filed and the date of the withholding certificate issued was subsequent to the date of transfer.

For example, if a request for a withholding certificate is filed on November 15, 2016, the actual date of transfer is December 1, 2016 and the IRS issues the withholding certificate on February 2, 2017, the date of transfer for Forms 8288 and 8288-A purposes is February 2, 2017. The tax year on the Form 8288 and Form 8288-A is changed by the IRS to February 2017, the date the withholding certificate is issued. See IRM 3.22.261.21.2. However, the transferor/seller reports the transfer on the income tax return for the year the actual transfer occurred, which is 2016.

Question 9: How may a transferor/seller ensure a transferee/buyer or closing agent will not withhold under IRC 1445 on dispositions of U.S. Real Property Interests (USRPI) when the dispositions are exempt from withholding because the amount realized is $300,000 or less and the USRPI will be used as a personal residence by the transferee/buyer?

The transferor/seller can ensure that there will be no withholding under IRC 1445 in situations where the amount realized on the disposition of a USRPI is $300,000 or less and the transferee/buyer is planning on using the USRPI as a personal residence by ensuring the all parties are well informed. This includes making sure the transferee/buyer and the closing agent are aware of the exception to withholding and making sure the transferee/buyer informs the closing agent that they plan on living in the USRPI as a personal residence. The instructions for the Form 8288, U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests, and Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities, provide information on this exception from withholding.

Question 10: When would a transferee/buyer complete a Form 8288-B to request a withholding certificate for a transferor/seller?

A transferee/buyer or the transferor/seller (or authorized person), may complete the Form 8288-B, Application for Withholding Certificate for Dispositions by Foreign Persons of U.S. Real Property Interests, and file it to request a withholding certificate for reduced or no withholding under IRC 1445. A transferee/buyer may file the Form 8288-B in situations where

- the transferee/buyer is more familiar with the administrative procedures related to withholding under IRC 1445, or

- the transferee/buyer may be aware that a reduced rate of withholding or no withholding is applicable, and filing the Form 8288-B and getting an approved withholding certificate would reduce their administrative burden of withholding and remitting tax and completing and filing Form 8288 and Form 8288-A.

Question 11: If a foreign transferor/seller has a current address outside the U.S. and applies for a withholding certificate, how can the transferor/seller ensure the withholding certificate is provided to the escrow agent/closing company timely by the Internal Revenue Service (IRS)?

A foreign transferor/seller who is residing overseas at the time they request a withholding certificate may put the escrow or closing company’s information in Box 5 of the Form 8288-B, Application for Withholding Certificate for Dispositions by Foreign Persons of U.S. Real Property Interests, to ensure that the closing agent timely receives IRS correspondence with respect to a determination made on a request of a withholding certificate.

Question 12: May a foreign person request and receive an Individual Taxpayer Identification Number (ITIN) prior to entering into a contract to dispose of a U.S Real Property Interest (USRPI) if they have no other valid reason to obtain an ITIN?

No, a foreign person, who does not have a valid reason to obtain an ITIN, cannot request an ITIN prior to entering a contract to dispose of a USRPI. A foreign person, who does not have and is not eligible to receive a social security number, can only apply for and receive an ITIN using Form W-7, Application for IRS Individual Taxpayer Identification Number, in certain situations including but not limited to a requirement to

- file a U.S. federal tax return,

- claim a reduced withholding under an applicable income tax treaty, and

- to be claimed as a dependent on another individual’s income tax return.

Therefore, absent any other valid reason to obtain an ITIN, the IRS will deny an application for an ITIN submitted prior to entering into a contract to dispose of a USRPI. As soon as there is a legally binding contract for the sale of a USRPI, the foreign person/seller is eligible to request an ITIN by filing Form W-7 under Exception #4, Third-Party Withholding – Disposition by a Foreign Person of a U.S. Real Property Interest.

Question 13: How long does the Internal Revenue Service (IRS) take to act on a withholding certificate application if the transferor/seller does not have a Taxpayer Identification Number (TIN) and applies for an Individual Tax Identification Number (ITIN) at the same time as the withholding certificate application?

The IRS will normally act on a withholding certificate application within 90 days of receipt of all information necessary to make a proper determination.

If a transferee/buyer or transferor/seller does not have a TIN and an ITIN is requested at the same time as the withholding certificate request, the ITIN request is processed within 10 days of receipt. The completed Form W-7 needs to include the completed form 8288-B, Application for Withholding Certificate for Dispositions by Foreign Persons of U.S. Real Property Interests, with the entire package forwarded to the IRS at the address given in the Form W-7 instructions.

Question 14: Is FIRPTA withholding required in situations where U.S. real property is disposed of and the real property is located in a community property state and titled only in the name of a U.S. person even though that U.S. person is married to a nonresident alien (NRA)?

Whether FIRPTA withholding is required on the disposition of U.S. real property that is located in a community property state and titled only in the name of a U.S. person who is married to an NRA is dependent upon the facts and circumstances. Generally, FIRPTA withholding is required when an NRA disposes of a U.S. real property interest (USRPI). Under community property law, title to property generally carries relatively little weight in determining whether property is separate or community property. Since the community property system has been adopted in several U.S. states and these community property laws are not all the same in all of the states, determining whether real estate is separate property or community property in one of these community property states needs to be determined based upon the facts and circumstances and the specific state’s community property laws. See Publication 555, Community Property, for additional information.

Question 15: Is FIRPTA withholding required when a nonresident alien (NRA) disposes of a U.S. real property interest (USRPI) by contributing it to a U.S. corporation in exchange for stock of that U.S. corporation in a nontaxable exchange under Internal Revenue Code (IRC) section 351?

Generally, FIRPTA withholding does not apply when an NRA exchanges a USRPI for stock in a U.S. corporation if 1) the disposition of the USRPI falls under one of the nonrecognition provisions of the IRC where gain or loss is not required to be recognized on the disposition such as under IRC 351, 2) the USRPI contributed to the U.S. corporation is exchanged for another USRPI which would be subject to U.S. taxation upon its disposition by the NRA, 3) the NRA provides the withholding agent the required notice under penalties of perjury that the disposition is not subject to gain or loss under a nonrecognition provision in the IRC, and 4) the withholding agent forwards a copy of the NRA’s notice along with the required cover letter to the IRS by the 20th day after the date of the disposition.

Question 16: Is FIRPTA withholding required when a nonresident alien (NRA) disposes of a U.S. real property interest (USRPI) by contributing it to a foreign corporation in exchange for stock in that foreign corporation?

Generally, unless provided otherwise in the regulations, FIRPTA withholding is required in the situation where a NRA disposes of a USRPI by exchanging it for shares of stock in a foreign corporation where the foreign corporation treats the contribution by the NRA as either paid in capital or a contribution to capital and the foreign corporation has not made the election under Internal Revenue Code (IRC) 897(i) to be treated as a U.S. corporation for purposes of FIRPTA withholding. In this situation, the shares of stock of the foreign corporation received by the NRA are not considered a USRPI and are not subject to U.S. taxation upon the NRA disposing of the stock in the future. Therefore, FIRPTA withholding would be required on the amount realized on the disposition of the USRPI to the foreign corporation in exchange for shares of the foreign corporation.

Question 17: Is FIRPTA withholding required in the situation where a U.S. real property interest (USRPI) owned by at least one nonresident alien and one or more others is disposed of and the transferee/buyer intends to use the USRPI as a residence and the total amount realized on the disposition of the USRPI is greater than $300,000 but no one transferor’s/seller’s allocable portion of the total amount realized is greater than $300,000?

Yes, FIRPTA withholding would be required. A NRA would not be exempt from FIRPTA withholding in the situation where the transferee intended to use the USRPI as a residence and the amount realized on a disposition of a USRPI is greater than $300,000 but each of the transferors’ allocable portions of the amount realized is $300,000 or less. The Internal Revenue Code (Code) provides the exemption to FIRPTA withholding titled “Residence where Amount Realized does not exceed $300,000”. This exemption from FIRPTA withholding is applicable if the transferee is acquiring the USRPI as a residence and the amount realized is $300,000 or less. The term “amount realized” is defined in the Code as the sum of the total cash paid by the transferee, the total fair market value of property transferred by the transferee, and the total amount of debt or liability assumed by the transferee and not each transferors’ allocable portion of the amount realized. Therefore, if the amount realized on the disposition is greater than $300,000, this specific exemption is not applicable.

Question 18: Is FIRPTA withholding required in the situation where a nonresident alien (NRA) disposes of stock in a foreign corporation whose only asset is a U.S. real property interest (USRPI)?

No, generally FIRPTA withholding is not applicable when an NRA disposes of stock in a foreign corporation that has U.S. real property as its only asset as the stock in the foreign corporation is not considered to be a USRPI. FIRPTA withholding is not applicable unless an NRA disposes of a USRPI. However, if the foreign corporation makes the election under Internal Revenue Code (IRC) 897(i) election to be treated as a U.S. corporation and that corporation is determined to be a U.S. real property holding corporation (USRPHC), then the stock would be considered a USRPI and FIRPTA withholding would be applicable on the disposition of the stock.

Question 19: What description should be put on Line 3 of the Form 2848, Power of Attorney and Declaration of Representative, to identify the tax as FIRPTA related?

The general language to put on Line 3 of the Form 2848 in a FIRPTA related matter includes inserting “Withholding Tax – IRC 1445” in the “Description” area, inserting “Forms 8288, 8288-A, 8288-B” in the “Tax Form number” area, and inserting the year (YYYY) the USRPI was disposed of in the “Tax Year/Periods” area.

Note: This page contains one or more references to the Internal Revenue Code (IRC), Treasury Regulations, court cases, or other official tax guidance. References to these legal authorities are included for the convenience of those who would like to read the technical reference material. To access the applicable IRC sections, Treasury Regulations, or other official tax guidance, visit the Tax Code, Regulations, and Official Guidance page. To access any Tax Court case opinions issued after September 24, 1995, visit the Opinions Search page of the United States Tax Court.