Skip to content

Skip to content

Estate’s

Control Sheet

Date other state(s) fiduciary income tax return(s) due:

Alternate valuation date:

Email:

All section

references are to the Internal Revenue Code (“IRC”) unless otherwise indicated.

“DNI” refers to distributable net income; “IRS” to the Internal Revenue

Service; “QTIP” to qualified terminable interest property;

“ERTA” to the Economic Recovery

Tax Act of 1981, Pub. L. No. 97-34, 95 Stat. 172; “TRA 1997” to the

Taxpayer Relief Act of 1997, Pub. L. No. 105-34, 111 Stat. 788, “EGTRRA” to the Economic

Growth and Tax Relief Reconciliation Act of 2001,

Pub. L. No. 107-16,

“JGTRRA” to the Jobs and Growth Tax Relief Reconciliation Act of 2003, Pub. L.

No. 108-27, the “2010 Tax Relief

Act” to the Tax Relief,

Unemployment Insurance Reauthorization, and Job Creation

Act of 2010, Pub. L. No. 111-312,

and “ATRA” to the American

Taxpayer Relief Act of 2012,

Pub. L. No.112-240.

I. Introduction

A.

Overview

1.

During the course of the estate’s administration, an

executor performs four basic functions. The executor:

a.

Marshals assets;

b.

Determines and raises cash needs;

b.

Pays reasonable funeral expenses, debts, administration expenses, and taxes; and

c.

Distributes assets in accordance with the decedent’s will.

2.

In the performance of these tasks, the executor is

faced with various alternatives, time limitations, and elections. Depending on

the uniqueness of the estate, the executor may be faced with a multitude of

elections and should be cautious in the exercise or non-exercise of each

of them. The executor must consider the estate tax, gift tax, income tax, and generation- skipping transfer

tax consequences of each election.

An equitable adjustment may be required because of an executor’s

election or the executor’s failure to make an election. The compression and reduction of the income

tax rates for individuals, trusts,

and estates caused

by the Tax Reform Act of 1986, Pub. L. No. 99-514, 100 Stat. 2085, has

greatly influenced an executor when he or she makes an election. Non-tax

factors, such as the beneficiaries’ needs or a

beneficiary’s age may also have to be considered.

B.

Notice of Fiduciary Relationship – Section 6903

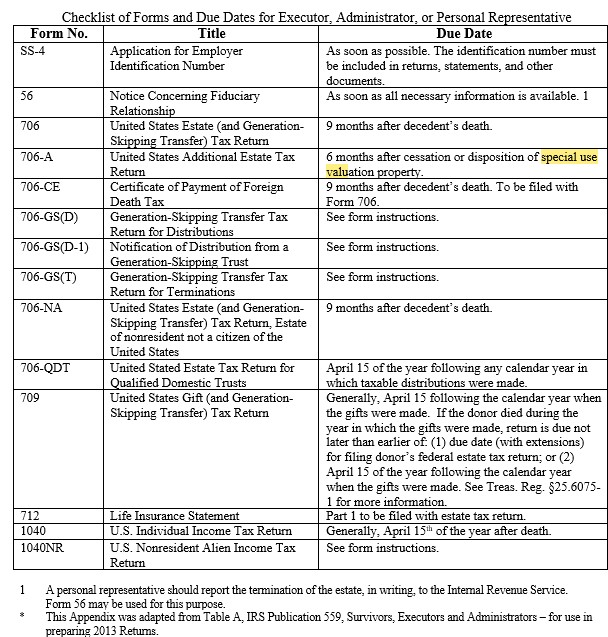

1.

An executor is required to provide written notice to

the Internal Revenue Service of the creation or termination of the fiduciary

relationship. §6903; Treas. Reg. §301.6903-1.

2.

Written notice is generally provided

by Form 56, Notice Concerning Fiduciary Relationship.

3.

Treas. Reg. §301.6903-1(b)(2) provides the requirements for notices filed

after April 24, 2002. The

notice must be signed by the fiduciary and filed with the service

center where the return of the person for whom the fiduciary is

acting is required to be filed. The notice must state the name and address of the person for whom the fiduciary is

acting, and the nature of such person’s liability; that is, whether

it is a liability for tax, and if so, the type of tax and the year

or years involved.

4.

If notice of fiduciary capacity is not provided to the

Internal Revenue Service, notice of deficiency sent by the IRS to the deceased

taxpayer’s last know address will be sufficient compliance with the requirements of the Internal

Revenue Code, even though the taxpayer is deceased. Treas. Reg. §301.6903-1(c).

II. Decedent’s Final Income Tax Return

A.

Overview

1.

The final return is due on the regular date for filing

had the decedent lived for the entire taxable year, generally April 15. Treas.

Reg. §1.6072-1(b).

2.

It includes income

and deductions of the decedent

for a period beginning with the first day of the taxable year (generally January 1)

and ending with the date of death.

3.

The executor should consider securing an automatic six

month extension of time to file the decedent’s final federal (using IRS Form

4868) and state personal income tax returns, if additional time is required.

4.

The executor of an individual’s estate is not required

to make installment payments of a taxpayer’s

estimated income tax in respect

of income earned in the period

prior to death,

where the installments are not due until after death. IRS Letter Ruling 9102010.

5.

The executor should prepare and submit IRS Form 4506

to the appropriate IRS Center, if necessary, to secure the decedent’s prior

years’ income tax returns. §6103(e).

6.

The executor should make certain that decedent’s final

Form W-2 does not include salary, commissions, and bonuses paid after death

that are reportable as income in respect of a decedent on the estate’s

fiduciary income tax returns.

7.

Note that a decedent’s final income tax return must

report all income actually distributed to that individual before death from a

simple trust regardless of the date on which the trust’s fiscal year ends.

§652. Income required to be distributed, but is in fact distributed to that individual’s estate,

is included in the estate’s

gross income as income in respect of a decedent under section 691. Treas. Reg.

§1.652(c)-2.

8.

Similar rule applies

with respect to distributions made from an estate or a complex

trust. §662; Treas. Reg.

§1.662(c)-2.

9.

For partnership tax years beginning

after December 31, 1997, the death of a partner

will result in the closing of

the partnership’s tax year with respect to that partner. §706(c)(2)(A). The

partnership’s tax year

continues for the

remaining partners. Consequently, partnership income or loss received by the partner

through date of death will be reportable on that individual’s final personal

income tax return. Is there any possibility of deferring or accelerating this

income or loss prior to death?

10.

The executor or administrator must sign the return, if

an executor or administrator has been appointed.

a. a. The surviving spouse and the fiduciary must sign the return if it is a

joint return.

b.

If no fiduciary

has been appointed, on a joint

return, the surviving spouse should sign the

return and write “Filing as surviving spouse” in the signature area.

11.

The executor should

prepare and file IRS Form 1310 (Statement of Person Claiming

Refund Due a Deceased Taxpayer), with evidence of the fiduciary’s

appointment to the appropriate Service Center, if income tax refund is due.

a.

Form 1310 will normally be filed by a fiduciary

claiming a refund for the decedent on Form 1040X or Form 843.

b. b. The executor need not file Form 1310

if:

i.

A surviving spouse is filing an original or amended joint return with

the decedent.

ii.

A personal representative is filing an original Form

1040, Form 1040A, or Form 1040EZ for the decedent and is attaching a court certificate

showing his or her appointment.

B.

Joint Return Versus

Separate Return

1.

The executor and surviving spouse can file a joint

return on behalf of the decedent and surviving

spouse, if the decedent was

married at the time of death and

the surviving spouse

has not remarried before the end of the surviving spouse’s

taxable year. §6013(a)(2). However, a joint return is not available if either spouse

is a nonresident alien at any time during the taxable

year. §6013(a)(1).

a.

A joint return

includes income and deductions of the decedent

for the period

ending at the date

of death and includes a surviving spouse’s

income and deductions for the entire

year. Treas. Reg. §1.6013-1(d)(1).

b.

Liability for the entire tax shown on the return is

joint and several. §6013(d)(3). The executor

should consider whether

he or she is assuming

a risk for the surviving

spouse’s unknown tax liabilities.

c.

Liability for joint tax must be allocated. The estate tax deduction for income taxes due is limited to that amount for which the

decedent’s estate would be liable under local law. Absent contrary evidence, that deductible amount is determined as follows:

the decedent’s separate tax liability divided by the combined separate

tax liability of the decedent and the surviving

spouse, multiplied by the total joint tax liability. Treas. Reg. §20.2053-6(f).

d.

Consider filing a joint return

if the decedent’s deductions exceed

income, to avoid

the loss of excess deductions

in the final tax year. Excess capital losses and excess charitable deductions

may be otherwise wasted, unless the surviving spouse has or can generate

capital gains or other income in the final tax

year.

e.

Review decedent’s previously filed income tax returns

for carryovers (charitable contributions, capital losses, and net operating

expenses) that may otherwise be lost if not taken on a joint return with the

surviving spouse. Consider accelerating income to offset these losses (for example, making

§454(a) election re Series E Savings Bonds or

accelerating payouts under a deferred compensation plan).

f.

The primary advantage of filing a joint return is that

the income is subject to more favorable tax rates; otherwise, the less favorable tax rate schedules

for married persons filing separately must be used by each of the parties.

For example, in 2014 with

$100,000 of taxable

income, the federal income tax saving can amount to $4,921.

g.

The disadvantage of filing a joint return is the

potential exposure to the estate by becoming jointly and severally liable with

the surviving spouse for the entire tax and penalties.

2. The surviving spouse may

make a joint return with the deceased spouse

if:

a. a. The decedent has made no return for the taxable year;

b. b. No executor has been appointed at or before the time of making the

joint return; and

c.

No executor is appointed before the last day

prescribed by law for filing the surviving spouse’s return. Treas. Reg.

§1.6013-1(d)(3).

3.

The executor may disaffirm a joint return filed by a surviving spouse.

a.

The joint return

must be made in the form of a separate

return for the taxable year of the decedent concerning which the joint

return was made. Treas. Reg. §1.6013-1(d)(5).

b.

It must be made within one year after the last day

prescribed by law for filing the surviving spouse’s return (including extensions). Id.

c.

The separate return made by the executor shall

constitute the return of the deceased spouse for the taxable year.

d. d. The penalty and interest for delinquent returns,

as provided in sections 6651 and 6601, are applicable to the return made

by the executor in disaffirmance of the joint

return.

4.

The executor should consider making an election to

file a joint return for the prior taxable years in which the decedent filed

separate returns, for which a joint return could have been made by the decedent

and the decedent’s spouse under section 6013(a). §6013(b)(1); Treas. Reg.

§1.6013-2(a).

C.

Request for Prompt Assessment – Section 6501(d)

1.

Under section 6501(d), a request for prompt assessment

must be in writing, filed after the return in question has been filed, and

filed with the district director for the internal revenue district in which the

return was filed.

a.

The request must:

i. Be transmitted separately

from any other document;

ii. Set forth classes of tax and

taxable periods; and

iii. Clearly indicate that it is

a request for prompt assessment.

2.

Its effect is to limit the time in which an assessment

of tax may be made, or to start court proceedings in court without

an assessment, to a period

of 18 months from the date the request

is filed with the proper district director. Treas. Reg. §301.6501(d)-1(b).

3.

The special 18-month

period of limitations does not apply to any return filed after the request

has been filed unless an additional request is filed. Id.

4.

Requests for prompt assessment can be made on IRS Form

4810, to insure that the requirements of Treas. Reg. §301.6501(d)-1 are

satisfied. However, such a request may precipitate an audit.

D.

Request for Discharge from Personal Liability –

Section 6905(a)

1.

A request for discharge from personal liability must

be in writing, filed after the return in question has been filed, and filed with the internal revenue

office where the estate tax return is required to be filed. If no estate tax return is required to be filed,

the application should

be filed where the decedent’s final income tax return is required to be filed. §6905(a); Treas. Reg.

§301.6905-1(a).

a.

Within nine months after receipt of the application, the executor shall be notified

of the amount of taxes due and, upon

payment thereof, shall

be discharged from personal liability for any deficiency thereafter

found to be due.

b.

If not notified,

the executor will be discharged at the end of the nine-month period

from personal liability for any deficiency thereafter found to be due.

c.

A discharge under this section

from personal liability

applies only to the executor

in her personal capacity

and applies only to the executor’s own assets; it does not apply to the

executor’s liability in her fiduciary capacity to the extent of the estate’s

assets in her possession or control.

2.

An executor should request a discharge from personal liability on IRS

Form 5495.

3.

A request for discharge from personal liability may precipitate an audit.

E.

United States Savings Bonds – Section 454(a)

1.

Cash-basis owners of Series E savings bonds

and similar obligations normally do not elect to report each year the increase in their

redemption price as taxable income.

2.

If a decedent failed to make this election, the

executor may do so and the bonds previously unreported interest will be

included in the gross income on the decedent’s final income tax return.

§454(a); Rev. Rul. 68-145, 1968-1 C.B. 203.

3.

The executor may make this election on the decedent’s final income tax return if the bonds

are held in a revocable trust

and the decedent

did not make the election. Rev. Rul. 79-409,

1979-2

C.B. 208.

4.

If a section 454(a) election is made:

a. a. The executor must make the election for all bonds – Series

E, EE, and Series H and HH U.S.

savings bonds (bonds acquired by the decedent in exchange for Series E or EE

savings bonds).

b.

b. The income tax liability attributable to the accrued

interest constitutes a deduction for federal estate tax purposes.

c. c. The section 691(c) deduction is lost.

d. d. The election presents

a good opportunity for accelerating income on the decedent’s final return; the estate may need additional income to avoid a loss of excess

deductions in the final year.

e.

The election may be advantageous if the decedent is in

the 10 percent or 15 percent bracket and the beneficiaries of the bonds

are in the 35 percent

or 39.6 percent bracket.

f.

Neither the estate nor any subsequent beneficiary is bound to report interest

annually in subsequent years

unless they elect to do so. Treas. Reg. §1.454-1(a)(1). Consequently, the beneficiary who receives the bonds may defer

tax on the interest accrued on them until redemption.

5.

If a section 454(a) election is not

made:

a. a. Unreported interest is income in respect of a

decedent, taxable under section 691(a) to the

estate or beneficiary, and subject to the income

tax deduction allowed under section 691(c).

b.

The executor may make the election on a subsequent fiduciary income tax return. This practice may be desirable if there is a short

first taxable year for an estate with little other income.

c. c. The executor can redeem bonds to allow the estate

to report a portion of accrued income over a number of taxable years;

however, the executor should plan the redemptions to avoid any loss of

interest.

d. d. The executor should consider distributing the bonds to

residuary beneficiaries of the estate who would

report all accrued

interest on their own personal

income tax returns

in the earlier of the tax year in which they make a section 454(a)

election, or in which they redeem the bonds. Rev. Rul. 64-104, 1964-1 C.B. 223.

e. e. Bonds are includable in the gross

estate at a value equal

to the sum of the principal and accrued interest, regardless of

whether the executor made the section 454(a)

election.

F.

Medical Expenses

1.

The executor may deduct unpaid medical expenses either

as a medical expense on the decedent’s income tax return or on the estate tax return, at the election

of the executor.

§§213(c), 2053(a)(3).

2.

If the executor

pays the expense

during the one-year

period after death,

medical expenses may be

deducted on the return for the year when the expenses were incurred, but the executor

must waive the right to deduct those expenses for federal estate tax

purposes. Treas. Reg. §1.213-

1(d)(2).

3. A 7.5 per cent threshold applies for income tax purposes.

a.

If the decedent

has not satisfied the 7.5 per cent threshold before

death, the portion

of the medical expenses paid

after death required to meet the threshold amount may not produce any tax

benefit.

b.

The portion of medical expenses

below the 7.5 per cent threshold may not be claimed for estate tax purposes, if medical expenses

above the 7.5 per cent threshold are deducted on the income tax return. Rev. Rul.

77-357, 1977-2 C.B. 328.

c.

This provision does not apply to medical expenses that

the decedent incurs on a dependent’s behalf.

4. If the executor takes the

deduction for medical expenses for income tax

purposes:

a. a. If the expenses

were incurred in the year before the final year, the executor

will have to deduct those expenses on that year’s

return, possibly requiring an amended return.

b.

The deduction may reduce the final income tax liability, thus reducing the deduction of that liability on the estate tax

return, thereby increasing the estate tax.

c.

If no estate tax is due, this may cause the credit shelter bequest

to be decreased and the marital deduction bequest to be

increased – the executor must take the potential future estate tax into

consideration.

d.

This deduction is normally more valuable for estate

tax purposes. If this deduction is taken on the estate tax return, the section 2053 deduction for the decedent’s income tax liability

will increase.

e.

A determination of where to deduct medical

expenses will give

the executor the power to change dispositive consequences and may require

some sort of equitable adjustment, as in the case of administration expenses and casualty losses.

G.

Executor’s Compensation – Accept or Decline

1.

Fees and commissions paid to the executor for services rendered

are deductible by the estate either on the estate tax return or

the estate’s income tax return (or partially on each), as the executor chooses.

§§642(g), 2053(a)(2); Treas. Reg. §1.642(g)-2.

2.

The compensation is also taxable income. §61.

3.

The executor must consider these factors:

a. a.. Whether the executor is also a beneficiary of any portion of the estate.

b.

The personal liability assumed by the executor. For

example, see 31 U.S.C.A. §3713, which imposes personal liability on fiduciaries

for paying debts or distributing assets, which result in insufficient funds

available to satisfy a decedent’s tax obligations.

c. c. The estate’s net incremental estate tax bracket and

income tax bracket versus the executor’s marginal income tax bracket.

d.

If beneficiaries are of a younger generation than the

executor, the executor’s waiver passes the fees down without incurring estate

or gift tax.

4.

Taking commissions brings income tax advantages to the estate and beneficiaries.

a.

The commissions reduce

the estate’s taxable

income during the tax year;

however, check local law to

determine whether a court order is required for the advance payment of

commissions.

b. b. Excess deductions are passed through to the beneficiaries in the final

year. §642(h).

i.

Section 67 makes this planning technique less valuable

to individuals since those excess deductions are no longer

deductible except to the extent that they exceed two per cent of the individual’s adjusted

gross income.

ii.

However, it is still a viable planning

technique for individuals whose miscellaneous

itemized deductions already exceed two per cent of adjusted gross income.

iii.

They may be able to keep the estate open for a longer

period of time by using the deduction for commissions to offset additional

estate income.

5.

If a fiduciary is taking commissions, determine

whether local law authorizes the payment of

compensation in excess of the commissions prescribed by statute, if he or she

renders extraordinary services.

6.

The IRS issued

guidelines on when the executor

may waive the right to receive commissions without incurring income tax

or gift tax liability. Rev. Rul. 66-167, 1966-1 C.B. 20. The executor may do so:

a. a. If the executor

formally waives the right to compensation for services within

six months after the initial appointment.

b.

If the executor

fails to claim fees or commissions at the time of filing

usual accountings, and all other attendant facts and circumstances are consistent with a continuing intention to serve gratuitously.

c.

“If the timing, purpose, and effect of the waiver make

it serve any other important objective, it may then be proper to conclude that

the fiduciary has thereby enjoyed a realization of income by means of

controlling the disposition thereof, and at the same time, has also effected

a taxable gift by means of any resulting transfer

to a third party of his

contingent beneficial interest

in a part of the assets under his fiduciary control.” Rev. Rul.

66-167, 1966-1 C.B. 20; see also Breidert

v. Commissioner, 50 T.C. 844 (1968), acq., 1969-2 C.B. xxiv.

III. Estate’s Fiduciary Income Tax Return – Form 1041

A.

Selection of the Tax

Year

1.

Section 644, which requires all trusts to adopt a

calendar year as their taxable year, does not

apply to estates.

a. a. This provision eliminates the ability of trusts to

defer taxes on amounts distributed to trust beneficiaries.

b.

The rule does not apply to tax-exempt trusts

(described in section 501(a)) and wholly charitable trusts (described in

section 4947(a)(1)). §644(b).

2.

Under the current law, the selection of an estate’s

tax year is still one of the most important elections that the executor must make.

3.

The election is made on the first

fiduciary income tax return, which

is due three and one half

months after the close of the taxable year. Treas. Reg. §1.6072-1(a).

a. a. It allows the executor to use hindsight in making the election.

b.

The primary objectives of the election are to:

i. Equalize the income tax

brackets of the estate and beneficiaries.

ii. Defer payment of income taxes.

iii.

Use the estate’s $600 exemption and separate taxpayer status.

iv. Satisfy the immediate

financial needs of the beneficiaries.

c.

Before the election is made, the executor should

project the anticipated income and estimate allowable deductions for a

succeeding 12-month period.

4.

Make the election by the statutory due date of the

first return. An estate’s taxable year is adopted by filing its first Federal

income tax return

using that taxable

year. Treas. Reg.

§1.441-1(c)(1). Any change

to another accounting period requires the prior approval of the Commissioner.

Treas. Reg. §1.441-1(e).

5.

For tax years ending after May 16, 2002, the filing of an application for an extension of time to file

the estate’s first income tax return with the payment

of the tax due will no longer

establish the estate’s taxable period for tax reporting purposes. Rev.

Rul. 69-563, 1969-2 C.B. 104, obsoleted by T.D. 8996, 67 Fed. Reg. 35009 (5/16/02), which published Treas. Reg. §1.441- 1(c)(1).

6.

The estate’s first

tax year need not run a full 12-month period.

Depending on the anticipated

flow of income and actual

deductible expenses, a shorter period

should sometimes be used for the first tax year.

a.

A situation may exist wherein during the early months

of administration, the estate receives substantial sums of non-recurring items

of income, such as salaries, bonuses, commissions, deferred compensation, and

other forms of income in respect of a

decedent.

i.

If the first year is terminated before the receipt

of substantial sums of income,

the tax on this income can be

deferred more than one year.

ii.

The executor may want to split the income into two separate

tax years, to avoid the bunching of income in any one year.

b.

The beneficiaries may require substantial distributions shortly after

the decedent’s death.

If a distribution is made in an initial short tax year, the estate

should have little distributable net income that would be tracked out to the

beneficiary when the distribution is made.

c.

The executor may select a short fiscal year to reduce

income receivable in the current year, if income tax rates are expected to decrease.

7.

The selection of the proper fiscal year may defer the

beneficiary’s realization of taxable income.

Beneficiaries report distributions for their taxable

year with which

or within which

the estate’s year ends. §662(c).

a.

Example – The decedent dies August 1, 2014 and the

estate selects the first fiscal year ending January 31, 2015. Any distribution

to a beneficiary during this period will be deductible for the fiscal year ending January 31, 2015 and taxable to the beneficiary for the year ending December 31, 2015. Consequently, the beneficiary will not have to pay taxes on the income until April 15, 2016.

b.

Section 644 has substantially reduced

the use of tax deferral, when the testamentary trust is involved.

c.

The executor should consider an initial long year if the beneficiaries have no immediate need for a distribution and an estate

has not received substantial sums of non-recurring items of income.

d.

An initial long year may be attractive if the estate incurs substantial deductible expenses

early in the period of administration.

8.

The executor may select a long fiscal

year to receive as much income as possible in current tax year, if increase in income tax rates

is expected.

9.

The executor may also select a calendar year.

10.

The election of the tax year requires careful analysis.

a. a. The executor must analyze the income earned and the deductible expenses incurred.

b.

The executor must make the election early enough so as

not to lose the opportunity to select a short fiscal year.

11.

During first nine months of the estate’s

administration, the maximum of earning assets are usually present. If the

executor fails to adopt a fiscal year, the estate must file its income tax return on a calendar-year basis.

Treas. Reg. §1.441-1(b)(4).

B.

Treating Qualified Revocable Trust as Part of Decedent’s Estate

for Federal Income

Tax Purposes – Section 645

1.

For estates of decedents dying after August 5, 1997,

the TRA 1997 added new section 646, later redesignated section

645, which grants

an election to treat a qualified revocable trust as part of the

decedent’s estate for federal income tax purposes. To be treated as a

“qualified revocable trust”, the trust must be one that was treated as owned by the decedent

as a result of a power

held by her or him. §645(b)(1).

a.

The election must be made by both the trustee

of the revocable trust and the executor

of the estate, if any. §645(a).

b.

The election must be made no later than the due date

for filing the estate’s income tax return for its first year, including

extensions. §645(c).

c.

Once made, the election is irrevocable. Id.

2.

The election is effective for two years from the date

of decedent’s death, if no federal estate tax return is required, or six months

after the final determination of estate tax liability, if a federal estate tax

return is required. §645(b)(2).

3.

The procedure for making the election to treat the

revocable trust as part of the estate was initially found in Revenue Procedure

98-13, 1998-1 C.B. 370.

4.

To make the election, a required statement must be attached

to a U.S. Income Tax Return for Estates and Trusts (Form 1041). The

statement must provide the following:

a.

Identify the election as a section 645 election;

b.

Contain the decedent’s name, address, date of death,

and taxpayer identification number (TIN);

c.

Contain the trust’s name, address and TIN; however, if

the trust does not have a TIN because the trust

was reporting under

the alternate grantor

trust reporting requirements of Treas. Reg. §1.671-4(b)(2)(i)(A), the trustee must

obtain a TIN,

unless a Form

1041 does not have to be

filed (see Rev. Proc. 98-13, 1998-1 C.B. 370, Sec. 3.01(3));

d.

Contain the estate’s name, address and

TIN;

e.

Represent that the trust for which the election is

being made was treated under section 676 as a grantor trust owned by the decedent

due to the decedent’s power to revoke the

trust; and

f.

Be signed by both the estate’s executor or

administrator and a trustee of the qualified revocable trust. Rev. Proc. 98-13,

Sec. 3.01(6).

5.

The original required

statement must be attached to the estate’s

Form 1041 for its first

taxable year. A copy of the required statement must be attached to the

trust’s Form 1041 for the taxable year ending after the date of decedent’s death.

The election is considered made upon

the earlier of such filings. Once made, the election is effective from the date

of decedent’s death. Rev. Proc. 98-13, Sec.3.02.

6.

If the section 645 election is made, the income,

deductions and credits attributable to the qualified revocable trust for the period

subsequent to decedent’s death, must be excluded from the

trust’s Form 1041 for the taxable year ending after

the date of decedent’s death

and must be reported on the

estate’s Form 1041. Id.

7.

If there is no probate

estate, and neither

an executor nor an administrator will be appointed, a trustee of the qualified revocable trust must sign every Form

1041 for the estate. Id.

8.

Qualified revocable trust secures similar income tax

treatment as an estate when the section 645 election is made.

a.

Trust will now be allowed

a charitable deduction for amounts permanently set aside for charitable purposes, without

requirement that such amount be paid in order to secure a charitable deduction (see §642(c)).

b.

Trust will now be able to report

its income on a fiscal

year basis rather

than on a calendar

year basis.

c.

The active participation requirement under the passive loss rules will now be waived for qualified revocable trusts for two

years after the settlor’s death (see §469(i)(4)).

9.

On December 18, 2000, the IRS issued proposed

regulations under section 645 which contained different procedures for making

the election and for filing the short year return for a Qualified Revocable

Trust (QRT).

a.

In most situations, Rev. Proc. 98-13 required a trust that made a section 645 election to secure a taxpayer identification number

(TIN) and to file a Form 1041 for the trust’s short taxable year beginning at decedent’s date of death and ending on December

31 of that year.

b .

Under the proposed regulations, if a section 645

election was made for the trust, the trustee and the personal representative,

if any, may choose not to secure a TIN for the trust or file a Form 1041 for

the trust’s short tax year – the section 645 was considered made only after

a Form 1041 was filed,

with the requisite election statement attached, for the first taxable

year of the related estate,

or, if there was no personal representative, the first taxable year of the trust filing

as an estate. Prop. Reg. §1.645-1(c). Here,

the trust’s income,

deductions and credits were included on the combined Form 1041 for the electing

trust and the related estate under the related estate’s TIN. Prop. Reg. §§1.645- 1(d)(1)(i) and (ii)(A).

c.

In response to numerous requests that taxpayers be

permitted to use the procedures set

forth in the proposed regulations prior to the date final

regulations were issued,

the IRS had indicated that it

would allow estates and qualifying revocable trusts of decedents who died after December

31, 1999 and before the effective date of the final regulations to choose either the election

and reporting procedures set forth in Rev. Proc. 98-13, or those enumerated in

Prop. Reg. §1.645-1(c) and Prop. Reg. §§ 1.645-1(d)(1)(i) and (ii)(A). (Notice

2001-26, 2001-13 I.R.B. 942).

10.

The IRS has now issued final regulations under Section

645, effective for estates and trusts of decedents dying on or after December

24, 2002. Rev. Proc. 98-13 and Notice 201-26 are obsolete as of December 24, 2002.

11.

The section 645 election may be made whether or not an

executor is appointed for the estate. Treas. Reg. §1.645-1(c).

a.

If an executor is appointed, the executor and the

trustee of the QRT make the 645 election by filing a form provided by the IRS

for making the election (election form). Treas. Reg. §1.645-1(c)(1)(i).

b.

If an executor

is not appointed, the trustee

of the QRT makes the 645 election

by filing the election form.

Treas. Reg. §1.645-1(c)(2)(i).

c.

The election form,

IRS Form 8855,

“Election to Treat

a Qualified Revocable Trust as a Part of an Estate,” was issued in March 2004.

12.

Regardless of whether there is an executor for the

estate and regardless of whether a section 645 election will be made for the

QRT, a taxpayer identification number (TIN) must be obtained for the QRT following the decedent’s death.

The trustee must furnish the TIN to the

payors of the QRT. Treas. Reg. §1.645-1(d).

13.

If the trustee

of the QRT elects to make a section 645 election, the trustee is not required

to file a Form 1041 for the QRT for the short taxable

year beginning with the decedent’s death and ending on

December 31 of that year. Treas. Reg. §1.645-1(d)(2)(i).

14.

Regardless of whether or not there is an executor, the

trustee of the QRT must file a Form 1041 for the short taxable

year beginning with the decedent’s death and ending

on December 31 of that year, if a section 645 will not be made for the trust, or if the trustee and executor, if any,

are uncertain whether

a section 645 election will be made for the QRT. Treas. Reg.

§1.645-1(d)(2)(ii).

15.

Election period terminates on earlier of the day on

which both the electing trust and related estate, if any, have distributed all

of their assets or the day before the applicable date. Treas. Reg.

§1.645-1(f)(1).

a.

b.

C.

Payment of Estate

Income Tax

1.

Estates and trusts are required

to make estimated payments of income tax in the same manner as individuals. §6654(1).

a.

Estates in the first two years following decedent’s death are exempted from this requirement.

b.

Any grantor trust to which the decedent’s residuary

estate is payable is exempted from this requirement in the first two years

following decedent’s death. §6654(1)(2).

c.

Private foundations and charitable trusts that are taxed on unrelated business

income under

§511 are also exempted from this requirement. §6654(l)(3).

d.

Trusts are required to make estimated payments commencing with the

first taxable year, except

as provided in (b) and (c) above.

e.

Although trusts compute their taxable income as of a

date that is one month earlier than the cutoff

date used by individual for making estimated

payments, the due date for the estimated payments is the same for both.

1.

A trustee can elect to treat any portion of excess estimated payments for any tax

year as a payment made by the beneficiary or beneficiaries. That sum or amount

will be treated as a distribution paid or credited to a beneficiary on the last day of the applicable tax year. §643(g).

a.

The election must be made on Form 1041-T, Allocation of Estimated Tax Payments to Beneficiaries, and the election must be

filed within 65 days following the close of the trust’s tax year. §643(g)(2).

b.

The sum or amount so treated shall be treated

as a payment of estimated

tax made by the

beneficiary on January 15 following the close of the trust’s tax year. §643(g)(1)(C).

2.

In the case of a taxable year reasonably expected to

be the last taxable year of an estate, a fiduciary may elect to treat any

amount of an estimated tax payment made by an estate as a payment made by the

beneficiaries. §642(g)(3).

A.

Treatment of Property Distributed in Kind – Section

643(e)

1.

Section 643(e) governs all non-cash distributions. The

distribution of appreciated (or depreciated)

property results in a gain (or loss) to the trust or estate, only if an election is made

to recognize the gain (or loss). §643(e)(3).

2.

If a section 643(e) election is made:

a.

The gain or loss will be recognized by the estate

or trust as if the property had been sold to the beneficiary at the property’s

fair market value. §643(e)(3)(A)(ii).

b.

The estate or trust will be allowed

a distribution deduction equal to the fair market

value of the property distributed. §643(e)(3)(A)(iii).

c.

The beneficiary will receive ordinary income equal to

the fair market value of the property distributed (to the extent of the

beneficiary’s share of DNI from the trust or estate). Id.

d.

The beneficiary’s basis in the distributed property

will be the property’s fair market value on the date of distribution.

§643(e)(1).

3.

If a section 643(e) election is not

made:

a.

The distribution is treated as carrying out DNI only

to the extent of the lesser of the property’s

adjusted basis or its fair market value at the time of distribution. §643(e)(2).

b.

The beneficiary will receive ordinary income equal to

the lesser of the property’s adjusted basis or its fair market value (to the

extent of the beneficiary’s share of DNI from the trust or estate). Id.

c.

The beneficiary’s basis in the distributed property will

be the same as the trust’s or estate’s basis.

d.

The recognition of any gain or loss will be deferred

until the beneficiary sells the property.

4.

The executor must make the election on the income

tax return for the taxable

year in which

the distribution was made.

a.

The election shall apply to all distributions made by

the executor or trustee during the taxable year.

b.

Once made, the election is irrevocable, except

with the Secretary’s consent.

§643(e)(3)(B).

5.

This provision does not apply to distributions

described in section 663(a) – distributions of property to satisfy a specific

bequest or certain charitable distributions.

§643(e)(4).

6.

A primary benefit

of making a section 643(e)

election is to offset the trust’s or estate’s capital losses in current tax year.

7.

Advise a trustee

against making the section 643(e)

election for assets

worth less than their cost basis, to avoid creating loss that

would be non-deductible under section 267(a)(1).

8.

An interesting planning opportunity arises if a

trustee of a discretionary trust distributes appreciated property in kind to a charitable – minded trust beneficiary and the trustee

does not make a section 643(e)

election. If the beneficiary transfers the property to a charity, the gift will qualify

for a charitable income tax deduction at its fair

market value on the date

of transfer

– without recognition of any capital gains by the

trust or the beneficiary.

9.

Regardless of whether

the section 643(e)

election is made, inform each beneficiary of the cost basis of all assets distributed in kind.

B.

The 65 Day Rule – Section 663(b)

1.

A trustee of a complex

trust has for many years

been able to elect to treat certain

distributions made within 65 days after the close of the trust’s tax year as having been made earlier,

on the last day of that

previous tax year. §663(b).

2.

For taxable years beginning after August 5, 1997, the TRA 1997, which amended

section 663 (b), has made

this election available to an executor of an

estate.

a.

The election will

provide greater flexibility in timing distributions for tax purposes, since

an executor can now make a decision

based on known information rather than estimated projections.

b.

Due to the great disparity between the federal

income tax rates

applicable to individuals and estates, this election

will allow an executor to better coordinate the income tax planning for an

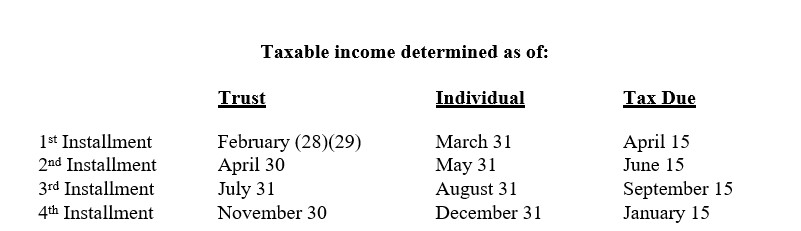

estate and the beneficiaries. The following Tables can be used to determine the federal income

tax liability for an estate

or trust for tax years beginning in 2014 and 2015.

3.

The election is made by checking the box on line 6,

page 2, of the Form 1041 under “Other Information.”

a.

The election must be made no later than the due date for filing

the fiduciary income

tax return, including extensions. Treas. Reg. §1.663(b)-2(a)(1).

b. The election is irrevocable

after the last day prescribed for making it.

Id.

c. The election is effective

only for the taxable year for which it is made. Treas. Reg.

§1.663(b)-1(a)(2).

4.

Does the 65 day rule apply to an estate in final tax year?

A.

Final Tax Year

1.

Since the estate is a separate entity for income tax

purposes, there are tax advantages in maintaining the existence of an estate as

long as possible.

a.

The estate will be considered terminated when all

assets have been

distributed except for a

reasonable amount set aside for unascertainable or contingent liabilities (not including claims

by a beneficiary in that capacity). Treas. Reg. §1.641(b)-3(a).

b.

If the estate’s administration is unreasonably

prolonged, the estate will be considered terminated for income tax purposes

after the expiration of a reasonable period for the performance by the executor

of all duties of administration. Id.

c.

The estate can be kept open if reasonable grounds or a

bona fide purpose exist for holding the estate open:

i.

The payment of estate tax in installments under section 6166.

Rev. Rul. 76-23,

1976- 1 C.B. 264.

ii.

The prosecution of a tax refund claim. McCauley v. U.S., 193 F. Supp. 938 (E.D.

Ark. 1961).

iii.

The payment of claims from estate income to avoid the

sale of valuable assets at a sacrifice. Carson

v. U.S., 317 F.2d 370 (Ct. Cl. 1963).

d.

The IRS will not issue advance rulings

or determination letters

on whether the period of administration or settlement of an

estate is reasonable or unduly prolonged. Rev.

Proc. 98-3, 1998-1 C.B. 100, superseded by Rev. Proc. 99-3, 1999-1 C.B. 103, superseded by Rev. Proc. 2000-4, 2000-1 C.B. 115.

2.

The executor can achieve income tax savings by the wise selection of an

estate’s final year.

a.

Excess deductions are lost in any other year.

b.

Only in the year of termination can beneficiaries take

advantage of excess deductions (deductions in excess

of estate’s or trust’s gross income). §642(h).

However, section 67 makes

this election less valuable to the extent

that a portion of those

excess deductions may not be

deductible to an individual beneficiary, except to the extent that those

deductions exceed two per cent of that individual’s adjusted gross income.

c.

In the year of termination, excess deductions pass to

“beneficiaries succeeding to the property of the estate or trust.” §642(h).

Generally, these beneficiaries are the residuary beneficiaries of an estate

or the remaindermen of a trust. Treas.

Reg. §1.642(h)-3(c),(d).

i.

The excess deductions are passed through

to beneficiaries on Schedule K-1 of Form 1041.

ii.

They are useful only to beneficiaries who itemize

since they are not allowable in determining the beneficiary’s adjusted gross

income. Treas. Reg. §1.642(h)-2(a).

d.

Since the two per cent floor imposed by section 67(a)

does not apply to trusts and estates, the executor may consider terminating the

estate in favor of trusts or other estates, where otherwise appropriate and

authorized. §67(c).

e.

The estate’s $600 personal exemption is lost in its final year.

3.

Avoid the “bunching of income” and excess income build-up in the final year.

a.

Upon the termination of an estate that is on a fiscal

year, it is possible for a residuary beneficiary to receive more than 12 months income

in one taxable year. For example, if an

estate with a fiscal year

ending March 31,

2015 terminates on November 30,

2015, the residuary beneficiary will be taxed on a full year’s

income, to the extent of distributions

and distributable net income, plus income for the final eight-month period.

Selection of a January 31,

2016 termination date would avoid this “bunching of income.”

b.

In the final year, all of the estate’s net income is

distributed to the beneficiaries, and is therefore taxable to them. Consider

terminating the estate shortly after the close of the prior taxable period to

reduce the total income earned during the final year.

4.

The executor should coordinate the timing of the

estate’s termination with the beneficiaries’

income tax planning.

a.

The executor should

advise residuary beneficiaries of their right

to claim deductions for losses and excess

deductions of the estate or revocable trust

pursuant to section

642(h), and of their potential income tax liability for income received

in the final year.

b.

Advise beneficiaries of need to accelerate receipt of

other income, to offset excess deductions and losses passed through in the

estate’s final year.

I.

U.S. ESTATE TAX RETURN –

FORM 706

A.

EXTENSION OF TIME TO FILE ESTATE TAX RETURN –

SECTION 6081(a)

1.

Generally, the U.S. Estate Tax Return (Form 706), must be filed within nine months after the date of death. §6075(a).

2.

Unless an extension of time for filing the estate tax return has been granted,

if there is no

numerically corresponding date in the ninth month,

the due date is the last date of the ninth

month. For example, if the decedent dies on July 31, 2015, the estate

tax return is due on April

30, 2016. If the due date falls on a Saturday, Sunday,

or a legal holiday, the return is due

on the next succeeding day which is not a Saturday, Sunday,

or legal holiday.

Treas. Reg. §20.6075-1.

3.

Effective for estate tax returns due after July 25,

2001, an executor will be allowed an automatic

six-month extension of time to file the Form 706. An automatic extension will be

allowed if the application:

a.

Is filed on or before the date prescribed in §6075(a) for filing the

return;

b.

Is filed with the appropriate IRS office designated in

the application’s instructions (except as provided in Treas. Reg. §301.6091-(b)

for hand-carried documents); and

c.

Includes an estimate of the full amount of estate and

generation skipping transfer tax due. Treas. Reg. §20.6081-1(b).

4.

The application should be made on IRS Form 4768 (Application for Extension of Time to File

a Return and/or

Pay U.S. Estate

(and Generation-Skipping Transfer) Taxes). It should

be made before

the expiration of time within

which the return

must otherwise be filed and failure to do so may indicate

negligence and constitute sufficient cause for denial. Treas. Reg. §20.6081-1(c).

5.

The Internal Revenue

Service may, upon a showing

of good and sufficient cause,

extend the time for filing the estate tax return for a period

not to exceed six months from the usual

date the return is due in certain situations. Treas. Reg. §20.6081-1(c). Such

an extension may be granted to an estate

that did not request an automatic extension of time to file the Form 706. In that case, the Form 4768

must also contain an explanation showing good cause for not requesting the

automatic extension. Id.

6.

An extension of time to file the return will not

operate as an extension of time to pay the

estate tax. Treas. Reg. §20.6081-1(e).

7.

Note the penalty

for filing a late return

– 5 percent (of the amount of tax) for the first month

and an additional 5 percent

for each additional month or part thereof, up to a maximum of 25 percent. §6651(a)(1).

8.

The executor should give serious consideration to

securing an automatic six-month extension of time to file the estate tax return

when assets pass to a QTIP trust. If the surviving spouse dies or becomes seriously ill within the six-month extension period, the executor may wish to make a partial QTIP election (or elect not to make a QTIP election)

to reduce the combined estate taxes. The executor may wish to pay some estate tax in first estate, causing a reduction of surviving spouse’s

estate, to equalize brackets and to secure a section 2013 credit for transfers

previously taxed for estate taxes attributable to the spouse’s income interest

on taxable portion.

B.

Deferral of Payment of

Estate Tax – Section 6161

1.

Generally, the U.S. Estate Tax Return (Form 706) is due nine months after the date of

death, and the tax must be paid in full with the return. §§6075(a); 6151(a).

2.

A district director or a director of a regional

service center may extend the time for payment of the estate tax for 12 months

from the usual date payment is due.

§6161(a)(1). If an

extension is granted, the time for payment of the estate tax is postponed until

21 months after the date of death.

3.

If reasonable cause exists, a district director is

authorized to grant an extension for a reasonable period not to exceed 10 years from the due date for payment of any part of

the estate tax owed by the estate.

If the estate tax has

been deferred under

section 6166, the extension

of time for reasonable cause cannot be extended beyond

12 months after the due date for the last

installment. §6161(a)(2). An extension may be granted if:

a.

The estate includes sufficient liquid assets to pay

the estate tax when otherwise due; however, the assets are located in several

jurisdictions, not immediately subject to the executor’s control.

b.

A substantial part of the assets of the estate

consists of the rights to receive payments in the future (annuities, copyright royalties, contingent fees, or accounts receivable).

c.

The estate includes a claim to substantial assets that

cannot be collected without litigation.

d.

The estate does not have sufficient funds

to pay estate

tax and also

provide funds to pay a reasonable family allowance and

to satisfy claims against the estate. Treas.

Reg. §20.6161-1(a).

4.

An application for an extension of time for payment of the estate tax must:

a.

Be in writing;

b.

Identify the period of time for which the extension is requested;

c.

Include a statement of the reasonable cause, if the application

is based upon reasonable cause; and include a declaration that the statement is

made under penalties of perjury. Treas. Reg. §20.6161-1(b).

5.

The application should

be made on IRS Form

4768 (Application for Extension of Time

to File a Return and/or Pay U.S. Estate (and Generation-Skipping Transfer) Taxes).

a.

The General Instructions accompanying the Form 4768

indicate that the request must be filed with the Department of the Treasury,

Internal Revenue Service Center, Cincinnati, Ohio 45999.

b.

The application will not be considered unless

it is filed on or before the date fixed for payment of the tax. Id.

6.

The executor should consider including in the section

6166 election a request under Treas. Reg. §20.6161-1(b), that the election be

treated alternatively as a request for extension under section 6161, if the

estate does not qualify for section 6166.

7.

An extension for the payment of the

tax:

a.

Will not relieve the executor

from the duty of filing a timely return. Treas. Reg.

§20.6161-1(c)(3).

b.

Will not relieve the estate from liability for payment

of interest on tax deferred during the period of the extension. Treas. Reg.

§20.6161-1(c)(2).

i

The amount deferred

bears interest from the due date of payment at a rate of interest adjusted quarterly according

to section 6621. §6601.

ii

The interest rate on an underpayment is equal to the

short-term federal rate plus three percentage points. §6621(a)(2).

iii

For the calendar quarter beginning April 1, 2015, the

section 6621 interest rate is three percent. Rev. Rul. 2015-5, 2015-13 I.R.B. 788.

c.

The district director may require a bond in an amount

up to twice the deferred amount. §6165.

8.

The IRS will not grant an extension if the deficiency

is on account of negligence, intentional disregard of rules and regulations, or fraud with intent to evade tax.

§6161(b)(3). If

the request for extension is denied, a written appeal may be made by registered or certified mail or hand delivery to the appropriate regional commissioner

within 10 days after the denial is mailed to the executor. Treas. Reg. §20.6161-1(b).

C.

Administration Expenses

and Casualty Losses

1.

Administration expenses and casualty losses,

herein “administration expenses,” can be used

as deductions in computing the decedent’s taxable estate and the

estate’s taxable income in whatever proportion the executor wishes to allow for

either purpose. §§642(g); 2053(a)(2); Treas.

Reg. §1.642(g)-2. For a comprehensive article on this topic, see Mariani, “Form 1041

vs. Form 706: Where to Deduct Administration Expenses,” Trust & Estates, June 1984, p. 37.

2. Types of administration expenses are:

a.

Executors’ commissions;

b.

Attorneys’ fees;

c.

Court fees;

d.

Accountants’ fees;

e.

Appraisers’ fees;

f.

Brokerage fees for selling estate property;

g.

Auctioneers’ fees for selling estate property;

h.

Costs incurred to store, insure, or maintain estate property;

i.

Expenses incurred to collect assets,

pay debts, and distribute assets

to persons entitled

to them; and

j.

Interest on federal and state income tax deficiencies that accrue after death.

3.

Generally, administration expenses can be deducted

against only one tax. §642(g). This rule

does not apply to deductions for taxes, interest, business

expenses and other

items accrued at decedent’s death; these

“deductions in respect of a decedent” are deductible for estate tax purposes

under section 2053(a)(3) and for income tax purposes under section 691(b). Treas. Reg. §1.642(g)-2. The rule also applies

to selling expenses

incurred in disposing of an estate’s property. Expenses can be used either

as an offset against recognized gain or an administrative

expense deduction for estate tax purposes, not both. §642(g).

a.

Will administration expenses be deducted on the Form

1041 or Form 706? The logical

starting point for this analysis

is a comparison of the estate’s estate tax bracket

with its income tax bracket,

and the effect that election will have upon the beneficiaries.

i.

An income tax deduction will be less valuable, because

of a reduction and compression of income tax rates for trusts and estates, as

reflected in section 1.

ii.

Before comparing brackets, determine the estate’s net

incremental tax rate (the federal estate tax bracket minus a credit for state

death taxes) for a more accurate comparison.

b.

What about the pre-ERTA maximum marital deduction

formula? Claiming administration expenses on an estate tax return will reduce

the value of the adjusted gross estate, thereby reducing the value of the

maximum marital deduction bequest by one half of the dollar amount of expenses.

This will be troublesome if the surviving spouse is the decedent’s second

spouse and also executor.

c.

Conflicts of interest

can be a problem. The executor may benefit personally by taking all of the deductions on the estate’s

income tax return. Consider seeking the advice and direction of the probate

court having jurisdiction over the estate. Matter

of Fales,, 106 Misc. 2d 419, 431 N.Y.S. 2d 763 (N.Y. County Surr. Ct.,

1980); Matter of Rappaport, 121 Misc. 2d 447, 467 N.Y.S. 2d 814 (Nassau

County Surr. Ct., 1983).

d.

Unless the will provides otherwise, statutory law, case law, and in some states equitable principles sensibly require

income interests to reimburse principal interests for the increase in estate taxes

caused by section

642(g) election. New York Estates,

Powers and Trusts Law §11-1.2 codifying the

results in In re Estate of Warms, 140

N.Y.S. 2d 169 (N.Y. County Surr.

Ct., 1955); Matter of Estate of Bixby’s, 140

Cal. App. 2d 326, 295 P.

2d 68 (Dist. Ct. App.1956); Maryland Estates and Trusts §11-106(a).

e.

The election decision must take account of the reduction of the

estate’s DNI.

f.

Administration expenses allocable

to tax-exempt income

are not deductible for income tax purposes; the executor

should claim the unused portion

on the estate tax return

if the executor deducts them.

g.

The executor should pass through excess deductions in

the final year to beneficiaries, who can deduct these expenses on their

individual returns, to the extent that the deductions exceed two per cent of the beneficiaries’ adjusted gross income.

Treas. Reg.§1.642(h)-2.

h.

Claiming inordinately high administration expenses

on the federal estate tax return may precipitate an audit of the Form 706.

i.

The administration expenses

are deductible on the estate’s

income tax return

only in the year

in which paid; if the expenses exceed income in any year other than the final year,

those “excess deductions” are lost. The deductions can be claimed on the estate

tax return when it is filed, long before expenses are paid.

j.

The executor must consider the effect of the election on the section

691(c) deduction.

k.

For section 2044

property, the executor must determine whether

claiming administration

expenses on the Form 1041 rather than on the Form 706 will increase the estate

tax payable on a QTIP trust created by the decedent’s pre-deceased spouse,

requiring an adjustment with that trust.

l.

The executor must consider whether

claiming expenses on the Form 1041 rather than on the Form 706 will permit more estate

tax to be deferred under section 6166.

m.

The executor must consider the effect on the apportionment of estate taxes.

n.

The executor must consider the effect on the state

death tax credit allowable under section 2011.

o.

The executor must consider the effect on the credit

for tax on prior transfers allowable under section 2013.

p.

The executor must consider the effect on the credit

for foreign death taxes allowable under section 2014.

4.

If administration expenses are claimed as deductions

on the estate’s income tax return, a statement must be filed in duplicate to

the effect that the items have not been allowed as deductions on the estate tax return

and that all rights to have the items subsequently allowed as

deductions are waived.

§642(g); Treas. Reg. §1.642(g)-1. The waiver is irrevocable and must

be filed before the expiration of the statutory period for the income tax return.

a.

Claiming deductions for estate tax purposes on the

initial estate tax return does not preclude a subsequent allowance and waiver

for income tax purposes, if the estate tax deduction is not finally allowed and

a statement is filed.

b.

If doubt exists, the executor should claim the

deduction on both the estate tax and income tax returns.

i.

The technique is permitted, if the estate

tax deduction is not finally

allowed and the statutory period for filing the

waiver statement has not run.

ii.

This technique will preserve maximum

flexibility.

D.

Alternate Valuation Election – Section 2032

1.

The alternate valuation date is the date six months

after the date of death for property not disposed of before that time. If the

property is disposed of within that six-month period, the alternate valuation

date is that date on which the property was distributed, sold,

exchanged, or otherwise

disposed of. §2032(a). The actual sales price of the stock sold in an arm’s

length transaction during the six month period following the date of death, not

the median between the high and low on the date of the sale,

fixes the value

for alternate valuation purposes. Rev. Rul.

70-512, 1970-2 C.B. 192.

2.

Before the enactment of the Tax Reform Act of 1984:

a.

The election had to be made on a timely

filed return, including

the additional period of

extension of time granted by the district director.

b.

The election could

not be made on a late return,

even if there was reasonable cause for a late filing. Estate of Calkins v. U.S., 79-2

U.S. Tax Cas. (CCH) 13,306

(E.D.N.Y. 1979).

c.

Because of the substantially increased unified gift

and estate tax credit and unlimited marital deduction, the availability of this election

granted the executor

a new technique to obtain a free step-up in basis of the property.

d.

If the estate

was not subject

to estate tax and assets

appreciated within six-month

period, alternate valuation date election would increase the income tax cost basis

of the property without any estate tax cost.

3.

The Tax Reform Act of 1984, Pub. L. No. 98-369, 98

Stat. 494, applies to the estates of decedents dying after July 18, 1984.

a.

The election is available only when both the value

of the gross estate and the estate

tax (after allowable credits) are reduced. §2032(c).

i.

This provision was added to discourage the executor’s

election of an alternate valuation date merely

to reduce a beneficiary’s income

tax liability upon a later sale

of the property. In such instances, the election was an abuse of the underlying

purposes of section 2032 – to reduce the overall estate tax liability when

assets had declined in value after

the decedent’s death.

ii.

The election is not available if a federal

estate tax return

is not required to be filed. If no federal estate tax return is

required, determine whether an alternate valuation election is allowable under

local law.

iii.

The election is not available if the “optimum” marital

deduction formula clause is used, since there would be no tax to be reduced.

b.

The election may be made on an estate tax return filed any time within one year after the

time prescribed by law (including extensions) for filing

such returns. §2032(d)(2). Thus, the election can be made up to 27 months after death.

However, note the potential consequences of filing a Form 706 late:

i.

A late filing

may cause the loss of section 6166 relief since

the section 6166 election

must be made on a timely filed return. §6166(d).

ii. Interest and penalty charges

will be imposed for a late filing.

c.

The election is irrevocable. §2032(d)(1).

4.

The election must also decrease any generation-skipping tax due. §2032(c)(2).

5.

If there is no day in the sixth month following the

decedent’s death that corresponds numerically

to the date of death,

the correct alternate valuation date under

section 2032(a)(2) is the last day of the sixth month. Rev.

Rul. 74-260, 1974-1 C.B. 275.

6.

The election is made by checking “Yes” to the box on line 1, page 2 of the Form 706 under the “Elections by the Executor.”

7.

The executor must examine the following considerations:

a.

How will the election affect the income tax basis-gain

or loss on subsequent sales or other disposition and the basis for depreciation purposes?

b.

What will be the effect

on the election to pay federal estate

taxes under section

6166 in installments-will it

reduce the value of the interest in a closely held business below 35 per cent

of the adjusted gross estate?

c.

What will be the effect on marital or charitable deductions?

d.

Will the election assist the estate in meeting the

requirements of the section 2032A special use election?

e.

Should any adjustment be made among any interests

under the will, revocable trust agreement, or otherwise because of the section

2032 election?

f.

Should the executor make election if the decedent

owned, or gave away within three years before death, a policy insuring someone

else who died within six months after decedent’s death? Advise the executor

against doing this.

8.

What about conflicts between beneficiaries? The

beneficiary of a parcel of real property or other asset that has declined in

value will desire the date of death value to secure a higher basis for income

tax purposes; the residuary beneficiary of a decedent’s estate who has the

obligation to pay estate taxes under the decedent’s will would want the section

2032 election to be made to reduce his or her tax burden.

E.

Special Use Valuation – Section 2032A

1.

If certain conditions are met, real property used for farming

or for a closely held business may be

valued on the basis of its actual

use, rather than on the traditional basis of highest

and best use. §2032A.

2.

The amount by which qualifying real property can be reduced

under section 2032A is $750,000.

§2032A(a)(2). The potential

maximum federal estate

tax saving amounts to $346,500. For estates of decedents dying after 1998, the $750,000

limitation has been increased to an amount equal to $750,000

multiplied

by

a

cost-of-living

adjustment.

§2032A(a)(3).

For estates of decedents dying in 1999, the value of the property may be

reduced by up to $760,000.

Rev. Proc. 98-61,

1998-2 C.B. 811. The value

of the property may be reduced by up to $770,000 for estates of decedents dying

in 2000. Rev.

Proc. 99-42, 1999-2

C.B. 568. For estates of decedents dying in 2001, the value of the property may be reduced

by up to $800,000. Rev. Proc. 2001-13, 2001-1 C.B. 337. The value of the

property may be reduced by up to $820,000

for estates of decedents dying in 2002. Rev. Proc. 2001-59, 2001-2

C.B. 623. For estates of decedents dying

in 2003, the value of the property

may be reduced by up to

$840,000. Rev. Proc. 2002-70, 2002-46 I.R.B. 845. The value of the property may

be reduced by up to $850,000

for estates of decedents dying

in 2004. Rev. Proc. 2003-85,

2003- 49 I.R.B. 1184. It may be reduced by up to $870,000 for estates of

decedents dying in 2005. Rev. Proc. 2004-71, 2004-50

I.R.B. 970. For estates of decedents dying in 2006, the value of

the property may be reduced by up to $900,000. Rev. Proc. 2005-70, 2005-47

I.R.B. 979. It may be reduced

by up to $940,000 for estates of decedents dying in 2007. Rev. Proc. 2006-53,

2006-48 I.R.B. 996. It may be reduced by up to $960,000 for estates of

decedents dying in 2008. Rev. Proc. 2007-66, 2007-45 I.R.B. 970; it may be

reduced by up to $1,000,000 for estates of decedents dying in 2009. Rev. Proc.

2008-66, 2008-45 I.R.B. 1107. For estates of decedents dying in 2010, the sum remains at $1,000,000. Rev. Proc. 2009-50,

2009-45 I.R.B. 617; it may be reduced by up to $1,020,000 for estates of decedents dying

in 2011. Rev. Proc.

2010-40, 2010-46 I.R.B.

663. For estates

of decedents dying in 2012, it may be reduced

by up to $1,040,000. Rev. Proc. 2011-52,

2011-45 I.R.B. 701; it may be reduced

by $1,070,000 for estates of decedents dying in 2013.

Rev. Proc. 2012-41, 2012-45 I.R.B. 539. It may be reduced by $1,090,000 for

estates of decedents dying in 2014. Rev. Proc. 2013-35, 2013-47

I.R.B. 537. For estates of decedents dying in 2015, the value of

qualified property may be reduced by up to $1,100,000. Rev. Proc. 2014-61,

2014-47 I.R.B. 860.

3.

The purpose of this provision is to assist estates of

farmers and owners of closely held businesses

by providing an alternate means

for valuing real property that is used in farming

or other small business purposes for federal estate tax purposes,

thereby reducing the overall estate tax liability and encouraging the heirs to

continue the operation of the farm or closely held business.

4.

The qualifications for the special use valuation are:

a.

The decedent must have been a resident or citizen of the United States. §2032A(a)(1).

b.

The property – “qualified real property” – must meet

the conditions in section 2032A(b)(1):

i.

The property must be located in the United States.

ii.

The property must be devoted to a qualified use on the date of

decedent’s death.

iii.

The property must pass to a qualified heir and a requisite agreement

must be filed.

c.

The decedent’s equity

in the real and personal

property used in the farm or closely

held business must be at least 50 per cent of the adjusted

value of the decedent’s gross estate. §2032A(b)(1),(3).

d.

The decedent’s equity in the qualified real property

must be at least 25 per cent of the adjusted value of the decedent’s gross

estate. Id.

e.

The decedent or a member of his family must have

materially participated in the operation of the farm or closely held business for five of the eight years preceding

death, decedent’s disability, or the commencement of receipt of social security. §2032A(b)(1),(4).

5.

The election to use a special use valuation must be made on the first federal

estate tax return filed. The election once made is

irrevocable. §2032A(d)(1).

a.

The requirement that the election

be made on a timely

filed return (including extensions) was repealed by Economic Recovery

Tax Act of 1981. The election may now be made

on a return filed late, so long as it is the first return. However, note the

potential consequences of filing a Form 706 late.

i.

Since many estates that qualify for section 2032A

election also qualify for section 6166 relief, a late filed return may cause

the loss of the section 6166 election since

the section 6166 election must be made on a timely filed return. §6166(d).

ii.

Interest and penalty charges may be imposed for a late filing.

b.

The election is made by checking “Yes” to line 2 of Part 3 of the Form 706 and attaching to the Return a completed

Schedule A-1 with the required statements and

appraisals.

c.

Each person in being who has a present or contingent

interest in the qualified real property for which the election is made must

sign an agreement consenting to the application of a recapture tax for that property. §2032A(d)(2); Treas. Reg. §20.2032A- 8(c)(1).

i.

A sample form of an agreement satisfying this provision is set forth

in Rev. Proc.

81- 14, 1981-1 C.B. 669. This form has been updated

by the IRS to include

a reference to the recapture of the

generation-skipping transfer tax and is designated as “Part 3. – Agreement to

Special Valuation Under Section 2032A” of Schedule A-1 of the Form 706.

ii.

The tax benefits realized by the estate where special

use valuation has been elected may be fully or partially recovered if the

qualified real property subsequently passes out of the family or ceases to be

used as a farm or closely held

business within 10 years of decedent’s death, or if there is insufficient

material participation by members of decedent’s family following death. §2032A(c).

d.

Attached to the return must also be a statement containing detailed information required by the Treasury