Skip to content

Skip to content

Woke up here in South East Asia to find this email in my inbox. The House passed the bill so it is on its way to POTUS.

Full bill is here – https://www.congress.gov/bill/116th-congress/house-bill/748/text

IRS details on the Coronavirus Tax Relief and Economic Impact Payments are here – https://www.irs.gov/coronavirus-tax-relief-and-economic-impact-payments

If you don’t file taxes, use the “Non-Filers: Enter Your Payment Info Here” application to provide simple information so you can get your payment.

– https://www.irs.gov/coronavirus/economic-impact-payments

Filers: Get Your Payment – Use the “Get My Payment” application to:

– Check your payment status

– Confirm your payment type: direct deposit or check

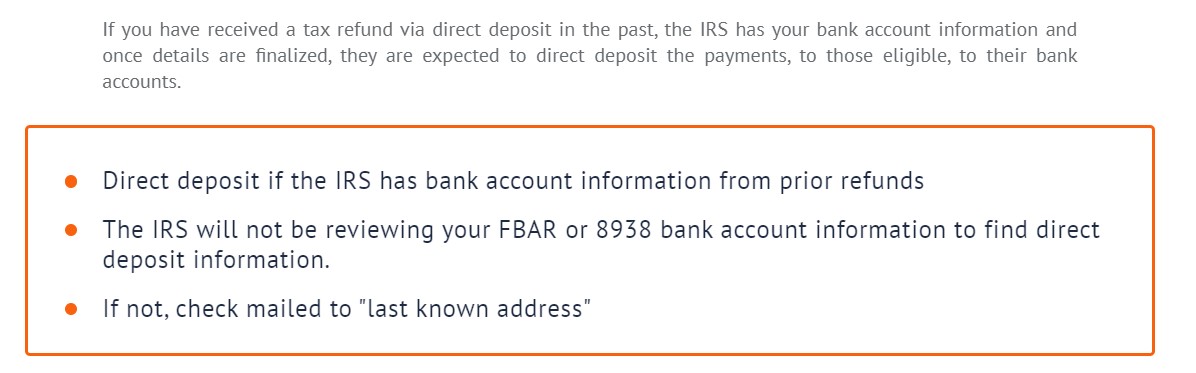

– Enter your bank account information for direct deposit if we don’t have your direct deposit information and we haven’t sent your payment yet

https://www.irs.gov/coronavirus/economic-impact-payments

Change Your Address – How to Notify the IRS –

https://www.irs.gov/taxtopics/tc157

Listed below are highlights of many, but not all, of the provisions included in the Act

The CARES Act includes these major provisions:

- Keeping America Workers Paid and Employed Act

- Assistance for American Workers, Families and Businesses

- Supporting the Health Care Fight Against COVID-19

- Economic Stabilization and Assistance to Severely Distressed Economic Sectors

- Coronavirus Relief Funds to State & Local Governments

Keeping American Workers Paid and Employed Act

The Act authorizes $349 billion of 100% guaranteed SBA loans to certain small businesses (typically 500 or fewer employers but may be higher limits for certain industries).

- Generally, the loan amount would equal 2.5 times an employer’s average monthly payroll for prior 12 months with a cap of $10 million.

- Proceeds from the loans may be used for payroll, mortgage interest, rent, utilities and other debt obligations.

- If a borrower maintains certain payroll levels for the 8-week period after the loan origination date, the borrower may be eligible for loan forgiveness equal to its payroll costs plus certain payments of mortgage interest, rent and utilities

Assistance for American Workers, Families and Businesses

- Bolstering of Unemployment Compensation Benefits

- Expansion of $600/week of unemployment compensation for terminated employments for up to 13 weeks beyond that provided under current state law

- Expansion of unemployment compensation recipients to include self-employed individuals, independent contractors, and other persons not previously eligible.

Rebates and Other Individual Provisions

- Qualifying individual and joint filers will be eligible for advanced tax credit rebates of $1,200 and $2,400, respectively, increasing by $500 for each dependent child. Eligibility for the rebates is phased-out based on adjusted gross income levels and filing status.

- Qualifying individuals may make early withdrawals from retirement accounts of up to $100,000 without being subject to the normal 10% early withdrawal penalty. The withdrawalscan be paid back over a three-year period.

- Taxpayers will be able to deduct up to $300 of charitable contributions, regardless of whether they itemize their deductions.

- The overall limitations on deductions for charitable contributions for individuals are suspended.

- The limitation on corporate charitable contributions is increased from ten percent (10%) of taxable income to twenty-five percent (25%) of taxable income.

- Employers may contribute up to $5,250 toward the repayment of an employee’s student loans on a tax-free basis to the employee.

Who is eligible for stimulus checks?

-

US tax residents with social security numbers, residing anywhere in the world, will receive checks depending on their income, which we outline below. Those with ITINs will not be eligible.

-

This stimulus check is essentially a 0% interest advance from the government for your 2020 tax return. This is NOT the same thing as the 2008 stimulus checks that were sent to battle the recession. See article here –

- The amount taxpayers will receive today will depend on their 2019 income (if already filed), or 2018 if not. The end amount taxpayers will receive will ultimately depend on their 2020 income.

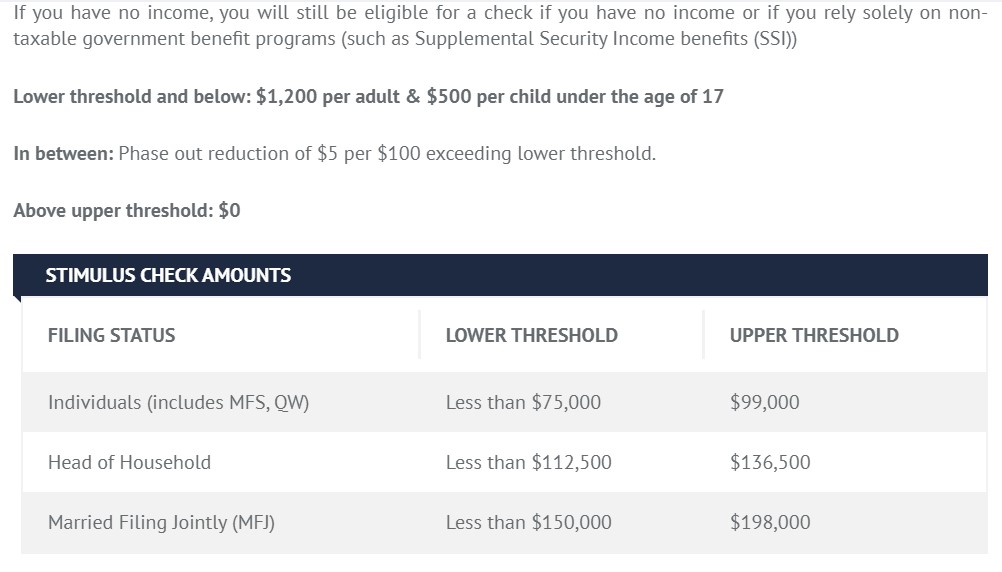

- The figure to look at is the amount of adjusted gross income. If you earned less than the first table (low threshold), you receive the full amount. The amount is reduced by $5 for every $100 exceeding the lower threshold. Once you reach the upper threshold (right column), the amount is completely phased out.

- If you filed your 2019 return, the numbers will be based off of that. If you have not, the 2018 figure will be used. Line item to look for on your tax return: Adjusted Gross Income (Line 8b) If you have no income, you will still be eligible for a check if you have no income or if you rely solely on non-taxable government benefit programs (such as Supplemental Security Income benefits (SSI))

- Some news outlets have reported that if your income is higher in 2020, you will not have to ‘pay the government back’. We believe this may not be correct.

- The amount is not a ‘gift’ but an advance credit, with 0% interest, on your 2020 tax return.

- Generally, if the IRS gives you money that you must pay back later (ie if you underpay your estimated taxes), they charge you interest. They will not charge interest on this credit.

- However, the amount of the credit received will eventually depend on your 2020 adjusted gross income.

- We will update this guide once the IRS releases their FAQ.

- There’s no sign up. The payments will be automatic for those who qualify.

- You do not need to call the IRS. See the special websitethe IRS created for coronavirus updates.

- The stimulus money is not considered income. These are considered a credit towards your 2020 taxes. When a taxpayer’s 2020 taxes are filed on April 15, 2021, these advance payments might be adjusted upward or downward as with any other non-refundable credit.

- When? Press briefings have indicated 3 weeks if the IRS is able to do direct deposit. Paper checks will inevitably take longer, especially for those residing abroad.

Business Provisions

- Employers are eligible for a refundable payroll tax credit of fifty percent (50%) percent of wages paid to employees during the COVID-19 pandemic, capped at $10,000 of qualified wages per employee.

- The Employer portion of payroll taxes related to social security taxes attributable to wages paid during 2020 will be postponed. Fifty percent (50%) of the amount deferred will be payable on December 31, 2021 and the remaining fifty percent (50%) will be payable on December 31, 2022.

- Net Operating Losses for 2018-2020 may be carried back for five years and may also offset one hundred percent (100%) of taxable income. Taxpayers with taxable income in such prior years may file amended returns and immediately qualify for tax refunds.

- For 2018-2020, individuals can use losses from pass-through entities such as limited liability companies and partnerships to offset all non-business income.

- Beginning in 2018, corporations may claim 100% of all corporate alternative minimum tax credits, rather than receive the benefit ratably over several years.

- The limitations on the deductibility of business interest expense are increased from thirty percent (30%) to fifty percent (50%) of adjusted taxable income for years 2019 and 2020.

- The depreciable life of “qualified improvement property” is reduced from 39 years to 15 years, therefore increasing depreciation deductions.

Supporting the Health Care Fight Against COVID-19

Support for America’s health care system

- Coverage for COVID-19 testing and preventative services

- Rural health care services outreach, rural health network development, and small health care provider quality improvement grant programs

- Limitation on liability for volunteer health care professionals

- Guidance on the sharing of protected health information during the emergency

- Expansion of telehealth authority for healthcare providers in a number of contexts

- Increased Medicare and Medicaid funding and extension of a number of Medicare and Medicaid programs and policies in response to the emergency

- The CARES Act also includes a $340 billion surge in emergency appropriations, including

- $100 billion for lost revenues and COVID-19 related expenses to hospitals, public entities, not-for-profits, and Medicare or Medicaid enrolled suppliers and providers that provide diagnoses, testing, or care for individuals with possible or actual cases of COVID-19

- $250 million to improve capacity of hospitals under the Hospital Preparedness Program

- $180 million to carry out telehealth and rural health activities to prevent, prepare for, and respond to coronavirus emergencies

- Changes to over-the-counter (OTC) drug review

- Allows FDA to approve changes to OTC drug monographs without full notice and comment rulemaking

- Provides 18-month market exclusivity period

- Clarifies that an OTC drug not in compliance with the monograph is considered misbranded

- Allows for a sponsor of a non-prescription sunscreen active ingredient who has a pending order to seek review under either the Sunscreen Innovation Act or under the new monograph review process

- Requires the Secretary of Health and Human Services to, within 1 year of enactment, provide Congress with an annual update describing the FDA’s progress in evaluating pediatric indications for certain cough and cold monograph drugs

- A new FDA user fee

- Beginning with fiscal year 2021, fees will be assessed to each person who owns a facility identified as an OTC monograph drug facility, and to each person who submits an OTC monograph order request

- The fees will be dedicated to FDA review of OTC monograph drugs and will allow the FDA to hire additional staff members to adequately provide agency oversight for changes to OTC drugs

- Caps Placed on Paid Leave

- Companies may limit Family and Medical Leave to each eligible employee in the amount of $200 per day and $10,000 in the aggregate

- Companies may limit Emergency Paid Sick Leave to each eligible employee based on leave applicable to his/her own condition in the amount of $511 per day and $5,110 in the aggregate

- Education Provision. Provides certain waivers, payments, and other relief related to education to aid students and certain teachers impacted by coronavirus and to allow certain otherwise allocated funds to be used to fight the coronavirus. Some key highlights of these provisions include:

- Issuance of work study payments to students unable to work due to closures caused by the virus;

- Relief for student grant or loan recipients impacted by coronavirus, including but not limited to adjustments to subsidized loan limits, relief from Pell grant duration limits, relief from the return of Pell grant or student loan funds and relief from certain Pell grant academic grade requirements, for students who withdrew from school as a result of COVID-19;

- Permits foreign institutions to offer distance learning to students receiving certain federal funds for the duration of the national emergency;

- Requires the deferral, without penalty, of student loan payments, principal and interest through September 20, 2020, and requires that each month for which payments are suspended shall be counted towards any loan forgiveness or rehabilitation program; and

- Allows the counting of a partial year of service interrupted by Covid-19 as a full year for TEACH grant teachers and waives certain consecutive years of teaching requirements for loan forgiveness eligibility

Economic Stabilization and Assistance to Severely Distressed Economic Sectors

- $500 billion in funding for the Treasury’s Exchange Stabilization Fund to provide loans, loan guaranties and investments, including:

- $25 billion for air carriers and certain other businesses related to air travel;

- $4 billion to cargo air carriers; and

- $17 billion for businesses important to national security.

- Treasury is to publish procedures regarding applications and minimum requirement for such loans within ten days of passage of the Act.

- Treasury may make loans to “eligible businesses” (defined as a US business that has not otherwise received adequate relief in the form of loans or loan guaranties under the Act) subject to certain requirements, including but not limited to credit availability, security and/or sufficient interest rate, the loan duration is as short as possible but no longer than 5 years, borrowers must maintain employment levels as of March 24, 2020 until September 30, 2020, the borrower cannot engage in stock buybacks or issue dividends, the loan cannot be forgiven

- $454 billion (supplemented by any amounts allocated above not used for the above purposes) for loans and loan guaranties to or investments in programs or facilities established by the Federal Reserve for purchasing obligations or other interests from issuers; purchasing obligations or other interests in the secondary markets or making loans, including loans secured by collateral.

- All requirements of Section 13(3) of the Federal Reserve Act (regarding loan collateralization, taxpayer protection, and borrower insolvency) shall apply to any program or facility.

- Treasury shall seek to establish a program or facility under this section targeted at nonprofits and businesses of between 500 and 10,000 employees, subject to additional loan criteria, including but not limited to: use of the funds to retain at least 90 percent of the borrower’s workforce that existed as of February 1, 2020, borrowers will not outsource offshore jobs for the loan period plus 2 years, the borrower will not issue dividends or engage in stock buybacks, the borrower will not abrogate collective bargaining agreements and must remain neutral in in union organizing efforts throughout the duration of the loan.

- Treasury shall seek to implement a program in connection with this program that provides liquidity to the financial system and supports lending to States and municipalities.

- Provides for Limitations on Certain Employee Compensation

- This section prohibits any eligible business that is a recipient of lending under this Title from raising the compensation of any officer or employee whose compensation in 2019 exceeded $425,000 and from offering such persons any severance pay or other benefits upon termination which exceed twice the annual maximum compensation received by such person until a year after the loan is repaid. Officer or directors of such an eligible person who made more than $3 million in 2019 are prohibited from earning more than $3 million plus 50% of the amount their compensated exceeded $3 million in 2019.

- Provides that the Secretary of the Treasury may require air carriers receiving loans under this Title to maintain schedule air service as deemed necessary by the Secretary of Transportation.

- Suspends certain aviation excise taxes.

- Debt Guaranty Authority

- Authorizes the FDIC to establish temporarily a debt guarantee program to guarantee debt of solvent insured depositories and depository institution holding companies, among other relief.

- Temporary lending limit waiver.

- Provides nonbank financial companies an exception to the OCC’s lending limits and authorizes the COC to exempt any transaction from the lending limits if in the public interest, but such grants of authority are limited and expire at the earlier of December 31, 2020 or the date of termination of the declared national emergency regarding coronavirus.

- Temporary relief for community banks.

- The federal banking agencies are required by interim rule to reduce the Community Bank Lending Ratio for qualifying banks to 8 percent and to provide a reasonable grace period if a community bank falls below such level. The interim rule shall expire at the earlier of December 31, 2020 or the date of the termination of the declared national emergency regarding coronavirus.

- Temporary relief from troubled debt restructurings

- Allows financial institutions to elect to suspend the requirements under US GAAP for loan modifications related to the coronavirus pandemic and to suspend any determinations of loans modified as a result of the effects of the coronavirus and being troubled debt restructuring. The Federal banking agencies must defer to any such suspensions. The applicable period for such suspensions is March 1, 2020 and 60 days from the date of termination of the declared national emergency regarding coronavirus.

- Optional temporary relief from current expected credit losses

- Provides that any insured depository institution, bank holding company, or any affiliate thereof shall not be required to comply with FASB Accounting Standards Update No. 2016-13, regarding measurement of credit losses on financial instruments, including the current expected credit losses methodology for estimating allowance for credit losses during the period from commencement of the Act until the earlier of December 31, 2020 or the date of termination of the declared national emergency regarding coronavirus.

- Non-applicability of restrictions on ESF during national emergency

- Suspends Section 131 of the Emergency Stabilization Act of 2008 (the limitation on the use of the Exchange Stabilization Fund) for guarantee programs for the US money market mutual fund industry and limits the amount of any guarantees established as a result shall be limited to the total value of a shareholder’s account in a participating fund as of the loss of the business on the day prior and shall terminate not later than December 31, 2020.

- Temporary credit union provisions

- Enhances, until December 31, 2020, access to the Central Liquidity Facility for corporate credit unions.

- Conflicts of interest

- Provides that any company in which the President, Vice President, executive department heads, Members of Congress, or any spouse, child, son-in-law or daughter-in-law of such person, owns 20% or more of the voting stock is not eligible for loans, loan guaranties or investments provided for in the Act.

- Congressional oversight commission

- Establishes a Congressional Oversight Commission charged with oversight of the provisions of this Title.

- Credit protection during Covid-19

- Provides that any furnisher to a credit reporting agency who agree to account forbearance or modified payments due to impact on a consumer by COVID-19 shall report such obligation or account as “current” or, if the account was delinquent prior thereto, maintain the delinquent status unless the consumer brings the obligation current. This provision is in effect from January 31, 2020 until the later of 120 days after enactment of the Act of 120 days after the date of termination of the declared national emergency regarding coronavirus.

- Foreclosure moratoriums and forbearance

- Prohibits foreclosures on federally-backed mortgage loans for a 60-period commencing March 18, 2020 and provides up to 180 days of forbearance for borrowers of a federally backed loan who have been financially impacted by coronavirus.

- Provides up to 90 days of forbearance for multifamily borrowers with federally backed multifamily mortgage loans who have been financially impacted.

- The authority under these sections terminates on the earlier of December 31, 2020 or the date of termination of the declared national emergency regarding coronavirus.

- Temporary moratorium on eviction filings

- For the period of 120 days commencing upon enactment of Act, prohibits landlords from commencing legal action to evict tenants or to charge late fees, penalties or other charges related to nonpayment of rent

Coronavirus Relief Funds

- Provides $150 billion in funding to states, territories and tribal governments for expenditures incurred due to revenue declines related to COVID-19.

Division B: Emergency Appropriations for Coronavirus Health Response and Agency Operations

In addition to appropriations related to some of the above-mandated actions and programs, Division B of the Act appropriates billions of dollars for federal, state, local and tribal activities, including but not limited to the following:

- Approximately $35 billion in funds for various arms of the Department of Agriculture

- $9.5 billion in funding to support agricultural producers impacted by COVID -19;

- $20.5 million to the Rural Cooperative Service to make the total available ending authority available for the Business and Industry loan guarantee program $1 billion;

- $100 million to the Reconnect Pilot for grants for the costs of construction, improvement or acquisition of facilities and equipment needed to provide broadband service in eligible rural areas.

- Approximately $1.89 billion in funds for the Department of Commerce

- $1.5 billion for the Economic Development Administration to support economic development grants for states and communities suffering economic injury as a result of COVID-19;

- $50 million to the Manufacturing Extension Partnership to help small and medium-sized manufacturers recover from the economic impacts of COVID-19;

- $300 million for direct financial assistance to fishers, fisher participants and fishing communities impacted by COVID-19.

- $1 Billion to the Department of Justice

- $10.5 Billion to the Department of Defense

- $1.45 billion for the Defense Working Capital Funds to mitigate the impact on production, supply chain, depots and labs of COVID -19;

- $1 billion for the Defense Production Act to increase access to material needed for national defense and pandemic recovery;

- $1.8 billion to address increased health cases among military members, dependents and retirees and the procure of medical equipment;

- $1.6 billion for the expansion of military health treatment facilities;

- $415 million for development of vaccines and related activities; approximately $628 million for the procurement of pharmaceuticals and protection equipment and for biohazard mitigation;

- $1.1 billion or additional shortfalls in the Defense Private Sector Care;

- The bill also provides certain authorizing provisions to DOD regarding restrictions on billings and required contractual provisions.

- $250 million to the IRS to support taxpayer services given the extended filing season and address implementation costs related to the Families First Coronavirus Response Act

- Approximately $50 billion in funds to the Department of Homeland Security

- $178 million to acquire personal protection equipment;

- $45 billion to continue FEMA’s response and recovery activities, funding FEMA facilities and grants to emergency services.

- Approximately $735 million to the Department of Interior

- $360 million in funds to the Department of Labor

- $345 million for the Dislocated Worker National Reserve for states and communities to respond to impacts and layoffs resulting from COVID-19.

- $140.4 billion to the Department of Health and Human Services

- $127 billion to the Public Health and Social Services Emergency Fund

- $6.3 billion for child and family related programs, which includes $3.5 billion in grants to states for assistance to child care providers, $750 million for Head Start programs, $1 billion available for community block grants; and grants to provide low income home energy assistance.

- Approximately $40 billion in funds to the Department of Education

- $19.6 billion to the Department of Veterans Affairs

- $14.4 billion to support VA healthcare services;

- $2.1 billion for medical community care.

- $31.1 billion in funds for the Department of Transportation

- $10 billion to maintain airport operations;

- $56 million to maintain air service to rural communities;

- $25 billion for transport service providers, states and local governments for operating and capital expenses; and

- approximately $1 billion for Amtrak operating assistance.

- $17.4 billion in funds to Housing and Urban Development

- $5 billion for the Community Development Block Grant program;

- $4 billion of homeless assistance grants to state and local governments;

- $1.25 billion to preserve Section 8 voucher rental assistance.