Skip to content

Skip to content

All things eventually come back into vogue, and the tax world is no different. In the early part of the 1980’s, C corporations were everywhere. Then, as part of the 1986 reform, Congress repealed the General Utilities doctrine, reinstating double taxation upon liquidation of a corporation and relegating the “C” to the entity choice of last resort.

C corporations have returned to prominence. Why?

For starters, there’s a new 21% corporate rate — down from 35% — and the potential to exclude all gain from the sale of stock five years down the road under Section 1202 that is specific to a C corporation. In addition, while the Tax Cuts and Jobs Act also added a 20% deduction for owners of flow-through businesses, many business owner — think: doctors, lawyers, accountants, actors, and athletes — aren’t eligible for the deduction. As a result; the effective federal corporate rate is pretty much equal as a C corporation when compared to an S corporation or partnership for many business owners, causing them to consider converting to a C corporation in pursuit of some of the non-tax benefits of operating in that capacity, a move that would have been largely unthinkable three years ago.

With the rise in businesses forming as or converting to C corporations, we’re going to take a deep dive into Section 351 and the tax treatment of the formation of a corporation. And remember, these rules apply equally if you form a C or S corporation.

Let’s start with a hypothetical business. You hold assets — some tangible, some intangible — that are appreciated. Will transferring those appreciated assets to a corporation trigger that gain? In addition, you’ve been reporting on the cash basis, and thus have zero basis receivables. Will handing those receivables to the corporation force you to recognize immediate income under assignment of income principles?

The answer to both questions is no, provided you do things right. As we’ll soon see, the tax law is structured so as to encourage the incorporation of an ongoing business in a tax-free manner, even if appreciated assets change hands in the process. As is always the case, however, there are exceptions to this general rule and more than a few traps for the unwary along the way.

So let’s do what we do in this space…let’s lay it all out and learn some stuff.

Section 1001, In General

Assume your assets — tangible and intangible — are worth a total of $1,000,00 and have a tax basis of $400,000. If a buyer comes along and pays you $1 million cash for the assets, the result is clear: under Section 1001, you will recognize gain for the difference between the amount realized ($1M) and the tax basis of the sold assets ($400,000), or $600,000. Nothing tricky here.

But say, instead, you transfer those same assets to a corporation in exchange for stock worth $1,000,000. As a general rule, NOTHING CHANGES. Even though you’re not getting cash, the result is the same. Check out Section 1001(b):

the amount realized on a sale is not just cash received, but the fair market value of any property you get in the exchange. In this case, you gave up assets with a basis of $400,000 and got back stock worth $1,000,000, so you’re in the same place as if you had sold for cash: you’ve got gain of $600,000.

If this were the case upon the transfer of assets to a corporation in exchange for stock, however, incorporating an ongoing business would be awfully painful from a tax perspective. And generally speaking, Congress tries to make it easy for a business to change its form (except for LEAVING corporate status, because of the need for double taxation). As a result, there has been a version of what is now Section 351 in the law for the last century, providing an exception to the general rule of Section 1001 and allowing transfers of appreciated property to a corporation — if a number of requirements are met — to go currently untaxed.

Why are we given such a substantial break? In the eyes of the IRS, if we transfer appreciated property to a corporation in exchange for stock constituting control in that corporation, we haven’t “cashed out” our investment in the property. Instead, we are simply continuing that investment in the property in a different form; i.e., through the corporation we now control. It’s the same reason we’re allowed to swap property for property tax-free in a like-kind exchange under Section 1031 or sell the stock or assets of a corporation in exchange for stock of the purchasing corporation in a tax-free reorganization under Section 368.

Hence the need for Section 351. Now, let’s figure out how it works.

Section 351, In General

Flip to Section 351(a): within its first paragraph, you’ll find that you can contribute property to a corporation without the recognition of gain or loss if THREE requirements are met:

- You must contribute property; rather than services or other enumerated items as described in Section 351(d),

- You must receive ONLY stock in the corporation in exchange for the property, and

- Immediately after the transaction, you — or importantly — a group of transferors — must “control” the corporation, which for our purposes right now, is satisfied if the transferors own at least 80% of the stock of the corporation.

Do all that, and no gain (or loss) is recognized in the transaction. But here’s the thing – the gain is not EXCLUDED; it is merely DEFERRED. If the shareholders sell the stock received in the transaction the next day, we need a mechanism in place to make sure the deferred gain is recognized. Likewise, if the corporation sells the property the next day, the same deferred gain needs to be triggered. We will find that this is accomplished via the “substituted basis” rules of Section 358 and the “carryover basis” rules of Section 362.

So here’s what we’re going to do. We’ll take these requirements one by one and deal first with a fairly basic transaction. Then we’ll layer on some complexity in the form of boot received and the assumption of liabilities.

What is Property?

Section 351 requires that you contribute “property” to a corporation in exchange for stock. But what is property? The statute defines it by exclusion; it doesn’t tell us what is property, but it does tell us what isn’t.

Where the statute comes up short in defining property, however, administrative rulings and judicial precedent pick up the slack. For example, Revenue Ruling 69-357 tells us that cash is considered property, which makes sense. Now, you might think, “why do we care if cash is property; the transfer of cash can’t trigger gain?” You’d be right, but don’t forget, we’re going to have to measure control in the corporation, and only stock issued for property is measured for purposes of that control. As a result, if stock issued for cash were not considered as being exchanged for property and counted towards the control test, Section 351 wouldn’t be particularly useful.

Likewise, we’re told that tangible personal property, real property, and even intangible property (See Section 936(h)(3)(B) and Revenue Ruling 64-56) are treated as property for purposes of Section 351. We’re also told that cash basis accounts receivables are property, and more importantly, the transfer of those receivables does NOT trigger acceleration of the income under assignment of income principles (See Revenue Ruling 80-198). Thus, if you incorporate a sole proprietorship by transferring zero basis receivables with a face value of $100,000 to a corporation in exchange for stock, you recognize no income; rather, the corporation will recognize the income when the receivables are collected.

Here’s what’s not property — services. If you receive stock for services, the value of that stock is taxed as compensation under Reg. Section 1.61-2, and you are not treated as having contributed property to the corporation. As a result, any stock received by someone providing services to a corporation is NOT counted towards the control test.

Ex: A and B transfer property to a newly organized corporation for 78% of the stock, and C, as part of the same transaction, receives 22% of the stock for services. The transfer does not qualify under Section 351 because C’s stock is not counted towards the control test; thus, A and B do not own the requisite 80% of the corporation.

There’s a twist, however: under Reg. Section 1.351-1(a)(1)(ii), if a transferor receives stock for a mixture of property and services, all the stock received by the transferor will count towards the control test unless the property transferred is of nominal value.

Same facts as above, except C transfers both property and services to the corporation for 22% of its stock. While C’s receipt of the stock for services is taxable, in this case, the stock is counted towards the control test. Thus the transaction is governed by Section 351.

For these purposes, the IRS has stated that property is of minimal value if its value is less than 10% of the value of the services provided.

In addition to services, Section 351(d) provides that open account debt of the corporation is not considered property, nor is interest that accrued on any debt of the corporation after the transferor acquired the debt, but these items are not commonly encountered in practice.

Transferor Must Receive Only Stock in the Corporation

If we want a transfer of property to a corporation to be entirely tax-free, you must receive ONLY stock. This isn’t particularly complicated aside from a couple of minor considerations:

- Certain “plain vanilla preferred stock” as defined by Section 351(g) is NOT counted as stock, but rather taxable boot (more on that later). It IS treated as stock, however, for purposes of measuring control.

- Stock rights and warrants are not stock unless they are virtually certain to be exercised.

- If a shareholder already owns 100% of a corporation, the shareholder does not need to receive any additional shares upon a subsequent contribution of property. This is rightfully referred to as the “meaningless gesture” doctrine; after all, if the transferor already owns 100% of the corporation, what’s the point of getting more stock?

What is Control, and When Must It Be Met?

As defined by Section 368(c), control is met for Section 351 purposes if the transferor — or a group of transferors — owns at least 80% of ALL voting shares, and then at least 80% of EACH class of nonvoting shares.

Ex. X Co. has 500 shares of voting stock A, 10 shares of nonvoting stock B and 100 shares of nonvoting stock C outstanding. Z who owned none of the stock prior to the transaction, transfers property to the corporation in exchange for 2,000 shares of voting stock A, 5 shares of nonvoting stock B, and 2,000 shares of nonvoting stock B. Even though Z owns more than 80% of ALL shares of X Co., Z does not own 80% of EACH class of nonvoting shares (Z owns only 5 of 15 shares of Class B shares). Thus, the Section 351 control test is not satisfied.

More importantly, Section 351 contemplates multiple transferors. For example, A, B and C may decide to form a corporation with A transferring hard assets, B transferring intangible assets, and C transferring cash. A, B and C will be treated as a transferor “group,” and control will be measured by the total amount of shares the combined group owns after the transaction, including any shares they owned BEFORE the transfer. Stated another way, you don’t have acquire control of 80% in the transfer, you just have to posses control of 80% AFTER the transfer.

Ex. Corporation Z has one class of common stock outstanding, which is owned by A (800 shares), B (200 shares), and C (200 shares). A and B transfer land they jointly own to Z in exchange for 400 additional shares (200 each) of the Z common stock. After the exchange, A (1,000 shares) and B (400 shares) own 1,400 of the total 1,600 shares outstanding, or 87.5%. As a result, together they control Z after the exchange, and the exchange qualifies under IRC § 351(a).

You have to be part of the transferor group (you have to currently contribute property) for your previously held stock to count towards the control test for any current contributors:

Ex. Corporation Z has one class of common stock outstanding, which is owned by A (800 shares), B (200 shares), and C (200 shares). A and B transfer land they jointly own to Z, with A receiving 400 shares of common stock of Z and B receiving a Z promissory note. B is not a member of the control group, because B did not receive stock in exchange for his interest in the land. As a result, A is the only member of the control group; since A’s ownership percentage after the exchange is only 75% (1,200 shares of a total 1,600), A’s exchange of his interest in the land for stock of Z does not qualify under IRC § 351.

Here’s what you can’t do….you can’t have an existing shareholder contribute a tiny piece of property to the corporation for the sole purpose of helping NEW transferors qualify under Section 351. These are referred to as “accommodation transfers” pursuant to Reg. Section 1.351-1(a)(1)(ii).

Individuals A and B each own 1,000 shares of the common stock of Corporation C. No other stock is outstanding. A transfers land to C in exchange for 1,000 additional shares of C common stock, and B transfers $5 to C and receives 5 additional shares of C common stock. B’s stock is not treated as issued for property under Reg. § 1.351-1(a)(1)(ii) ; thus, the stock owned by B is not taken into account in determining whether the control test is met. As a result, A’s transfer of land in exchange for C stock does not qualify under IRC § 351(a) .

The statute requires that the transferor or transferors control the corporation “immediately after” the transfer. But what if the group owns 80% for a moment in time, but then two days later, one shareholder sells enough stock to an unrelated buyer that the ownership of the group drops below 80%?

The law on this topic has evolved over the years through the courts, but currently, the prevailing guidance dictates that if at the time a transferor acquires the stock from the corporation, he or she had a binding written commitment to sell the stock received from the corporation, then control is measured AFTER the second disposition of the stock.

To the contrary, if a transferor received stock from the corporation with no binding written commitment to sell the stock, control is measured immediately after the receipt of the stock, and a subsequent disposition of the stock, regardless of how soon it comes after the initial transfer, will not invalidate the previously satisfied control test.

Putting it All Together and Preserving Deferral

Going back to our hypothetical, we transferred assets with a basis of $400,000 and a FMV of $1 million to a corporation in exchange for stock worth $1 million. We have satisfied the three requirements of Section 351:

- We transferred property,

- Got only stock in return, and

- Controlled the corporation immediately after the transfer.

Thus, the $600,000 of gain is not recognized on the transfer. The gain, however, must be merely DEFERRED, rather than excluded, and to preserve that deferral, we’ll have to look to Sections 358 and 362

Section 358

At this stage in the game, we only care about a part of Section 358; the part that provides that a transferor’s basis in the stock received is equal to the basis of the assets given up in the exchange; in this case, $400,000. This way, if we sell the stock the next day for its value of $1 million, the $600,000 of gain that was previously deferred is recognized. This is what is known as “substituted basis.”

Section 362

Likewise, Section 362 provides that the corporation’s basis in the assets received is equal to the transferor’s basis in those assets, or $400,000. That way, if the corporation sells the assets the next day for their FMV of $1 million, the $600,000 of deferred gain is recognized. This is what is known as “carryover basis.”

That’s Section 351 in its cleanest form. But the Code didn’t get to be what it is by being clean, which means we’ve got some complexities to layer on. Let’s do it.

Receipt of Boot

Here’s what we’ve established thus far: if you transfer appreciated property to a corporation SOLELY for stock, no gain or loss is recognized. But what if in addition to stock, you also receive cash or other non-stock property (what we refer to as “boot”)?

Section 351(b) provides that in this case, you recognize gain equal to the LESSER OF:

- The boot received, or

- The gain that WOULD have been realized on the transfer of the appreciated property in a fully taxable transaction (i.e, the gain realized on the transfer).

Ex. Individuals A and B organize Corporation C. A transfers $5,000 to C in exchange for C common stock worth $5,000; B transfers a building to C with a $5,000 FMV and $3,000 basis, in exchange for $4,000 worth of C common stock and $1,000 of cash.

B recognizes gain equal to the lesser of:

- The boot received of $1,000, or

- The realized gain of $2,000: this is the excess of the cash received ($1,000) plus the FMV of the stock ($4,000) over B’s basis in the property transferred ($3,000)

Thus, B recognizes $1,000 of gain.

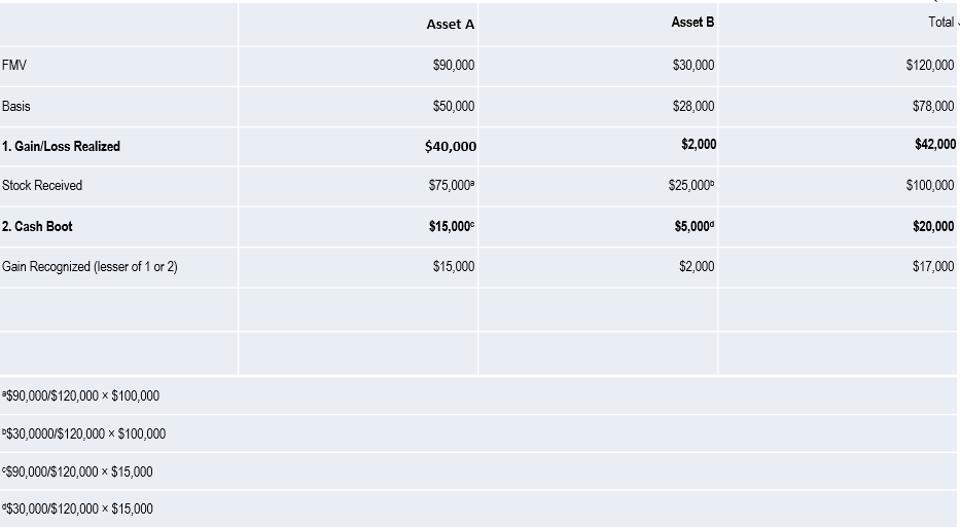

Things get a little more complicated if you transfer multiple assets. In this case, Rev. Rul. 86-55 provides that you don’t determine the boot and realized gain on a COMBINED basis; rather, the boot has to be allocated among all assets transferred in accordance with relative FMV, and then gain is recognized for EACH ASSET based on the lesser of the allocated boot or the realized gain on THAT ASSET.

X transfers two assets to Z Co in exchange for Z stock worth $100,000 and $20,000 cash. The transfer qualifies as a Section 351 transfer. The character of each asset and its fair market value and adjusted basis is as follows:

Asset A: capital asset held for 3 years, FMV of $90,000, basis of $50,000

Asset B: ordinary income asset with a FMV of $30,000, basis of $28,000.

The gain is determined as follows:

Boot within gain, multiple assets

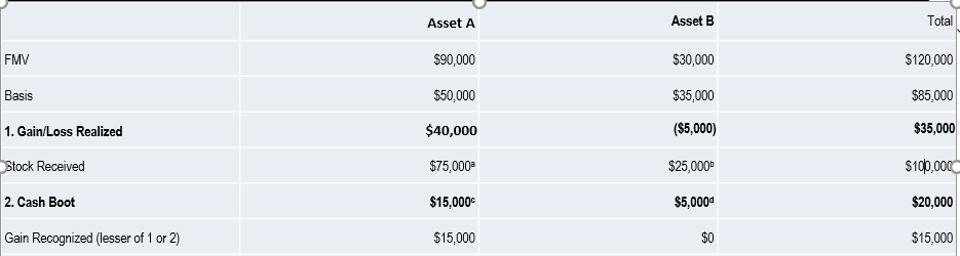

Ex. X transfers two assets to Z Co in exchange for Z stock worth $100,000 and $20,000 cash. The transfer qualifies as a Section 351 transfer. The character of each asset and its fair market value and adjusted basis is as follows:

Asset A: capital asset held for 3 years, FMV of $90,000, basis of $50,000

Asset B: ordinary income asset with a FMV of $30,000, basis of $35,000.

The gain is determined as follows:

Boot within gain

In this case, because there is no realized gain on the transfer of Asset B, there is no boot recognition.

Character of Gain and Holding Period

The character of gain recognized under Section 351 is also determined on an asset-by-asset basis. Thus, in the two examples above, any gain recognized on the transfer of Asset A would be long-term capital gain, and any gain recognized on the transfer of Asset B would be ordinary income.

It’s worthy of note that if the property transferred were subject to depreciation recapture — say, the asset had been purchased for $5,000, depreciated to $3,000, and transferred to a corporation for stock worth $4,000 and cash of $1,0000 — the transferor would recognize gain of $1,000, and the entire gain would be taxed as ordinary income pursuant to Section 1245. In other words, Section 1245 recapture doesn’t override Section 351, but any gain recognized under Section 351 will be subject to the recapture rules.

Next, let’s take a look at holding period. In the transaction, the transferor received stock worth $100,000. The holding period of that stock tacks to the holding period of the property transferred, but pursuant to Section 1223(1), only if the property transferred is a capital asset or Section 1231 asset. If assets that don’t fit into these classes are also transferred, the holding period of the stock received is split between tacked and non-tacked based on relative FMV. Thus, in our examples above, 3/4 of each share of stock would have a 3-year holding period, and 1/4 of each share of stock would have a holding period beginning on the date of the transfer.

For the corporation, the holding period of the assets received is determined under Section 1223(2) and should include the holding period of all assets transferred, regardless of whether the assets are capital assets, Section 1231 assets, or otherwise.

Assumption of Liabilities

Let’s say you sell an asset with a basis of $200, a FMV of $1,000, and with a $300 mortgage. If the buyer pays you the full $1,000 and tells you to pay off the mortgage, clearly you’d include the full $1,000 in your sales price and recognize $800 of gain. But what if the buyer says, “I’ll pay you $700 and assume your $300 mortgage.” In this case, the results are EXACTLY the same. Your amount realized under Section 1001 includes not only the $700 of cash received, but also the $300 of debt assumed by the buyer, the idea being that since YOU are no longer on the hook for repaying that debt, you have been enriched to the tune of $300. So just like a straight sale for cash, you’ll have a sales price of $1,000 and $800 of gain.

Thus, a general principle of the tax law is that the assumption of liabilities in a transaction is treated as if the seller received cash in that amount. It follows, then, that if you contribute property subject to a liability to a corporation in exchange for stock, the assumption of that liability must be treated as cash boot, right?

Wrong. Think about it: if that were the case, it would be awfully hard to incorporate an existing business, because most businesses have liabilities, either of the bank debt or payables variety. Thus, Section 357 creates a general rule and then a couple of exceptions:

General rule: debt transferred to a corporation in a Section 351 transfer is NOT treated as cash boot for recognition of gain purposes.

Exception 1: If the debt was taken out for tax avoidance purposes — or for non-business reasons — then ALL debt in the transfer — not just the offending debt — is treated as cash boot. Of course, that means the liabilities are still only taxable to the extent of any realized gain on the transfer.

Exception 2: This is the big one. If the total amount of liabilities transferred to the corporation exceed the total of the tax basis of the assets transferred to the corporation, then the excess of the liabilities over the basis is AUTOMATICALLY treated as gain, even if there is no REALIZED gain on the transaction. It is very important to note that for these purposes, liabilities do NOT include cash-basis liabilities that would give rise to a deduction when paid. Thus, items like accounts payables transferred by a cash-basis basis to a corporation would NOT count towards the Section 357(c) computation.

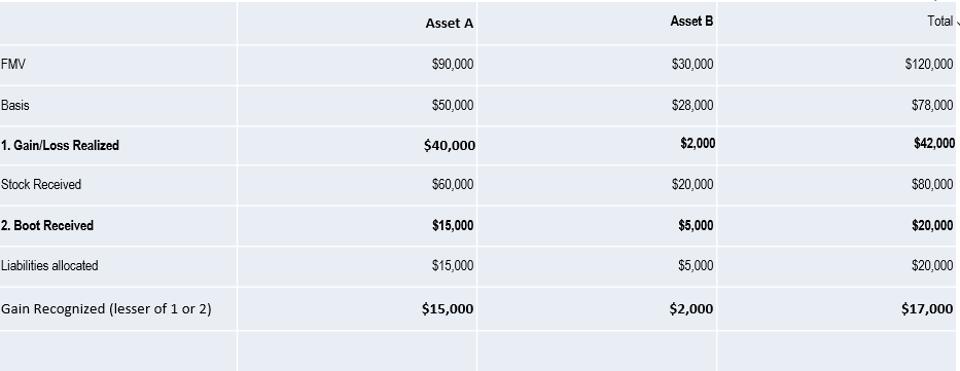

Ex. X transfers two assets to Z Co in exchange for Z stock worth $80,000 and $20,000 cash. The transfer qualifies as a Section 351 transfer. The character of each asset and its fair market value and adjusted basis is as follows:

Asset A: capital asset held for 3 years, FMV of $90,000, basis of $50,000, and encumbered by a $20,000 mortgage.

Asset B: ordinary income asset with a FMV of $30,000, basis of $28,000.

The liabilities do not exceed the basis of the assets; thus they are NOT treated as boot. They are treated as amount realized on the transfer in computing realized gain, however. The regulations require the liabilities to be allocated among the assets in accordance with FMV.

liabilities

Now, let’s take a look at the application of Section 357(c):

X transfers two assets to Z Co in exchange for Z stock worth $60,000. The transfer qualifies as a Section 351 transfer. The character of each asset and its fair market value and adjusted basis is as follows:

Asset A: capital asset held for 3 years, FMV of $90,000, basis of $20,000, encumbered by a mortgage of $40,000.

Asset B: ordinary income asset with a FMV of $30,000, basis of $28,000, encumbered by a $20,000 mortgage.

X recognizes gain of $12,000, the excess of the $60,000 of debt assumed by Z Co. over the $48,000 of combined basis X held in the transferred assets. The gain is not limited by any realized gain on the transferred assets. The gain is allocated between Asset A and B based on their relative FMV, thus, $9,000 is allocated to Asset A and $3,000 to B. A has $9,000 of LTCG and $3,000 of ordinary income.

Basis with Boot and Liabilities

When you have a Section 351 transfer with boot and liability assumptions, the computation of the transferor’s basis in stock and the corporation’s basis in the assets is a little more complicated.

Shareholder’s basis in stock received:

The formula for computing the shareholder’s basis in the stock received is as follows:

Basis in the property given up + gain recognized – boot received – liabilities assumed. Thus, for these purposes, liabilities assumed ARE treated as boot in the sense that they also reduce basis.

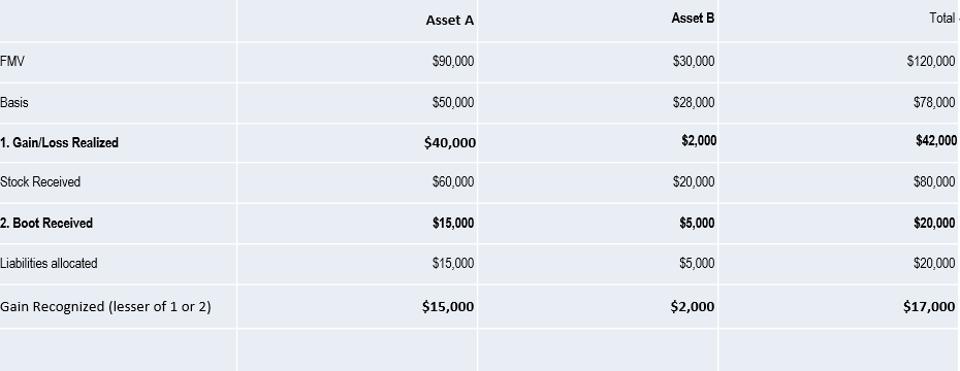

X transfers two assets to Z Co in exchange for Z stock worth $80,000 and $20,000 cash. The transfer qualifies as a Section 351 transfer. The character of each asset and its fair market value and adjusted basis is as follows:

Asset A: capital asset held for 3 years, FMV of $90,000, basis of $50,000, and encumbered by a $20,000 mortgage.

Asset B: ordinary income asset with a FMV of $30,000, basis of $28,000.

As a reminder, gain is recognized as follows:

Basis computation

The basis in the stock received, pursuant to Section 358, would be computed as follows:

Basis in the property contributed ($78,000) + gain recognized ($17,000) less boot received ($20,000) less liabilities assumed ($20,000), or $55,000.

OK, so that’s the mechanical way to compute basis. But I would encourage you to embrace the common sense “sanity check” approach. How does that work?

On the transfer, there was $42,000 of realized gain. We know that this gain needs to be deferred rather than excluded. On the transaction, $17,000 of the gain was recognized. This means that there is $25,000 of gain remaining to be recognized in the event that the stock is sold by the shareholder immediately after the transfer. The FMV of that stock is $80,000. So if the stock would fetch $80,000 and we need the sale of that stock to generate the remaining $25,000 of gain, what must the basis of that stock have to be? That’s right: $55,000. The system works. Use this common sense approach EVERY TIME. It will not let you down.

One other trick: if you have to recognize Section 357(c) gain because liabilities exceed basis, by definition, the shareholder’s basis in the stock will ALWAYS be zero.

Ex.: A transfers property with a basis of $20,000, a FMV of $100,000, and subject to a liability of $30,000 in exchange for stock worth $70,000. Under Section 357(c), A is required to recognize $10,000 of gain. A’s basis in the stock received is equal to $0 ($20,000 + $10,000 gain – $30,000 liabilities).

Corporation’s basis in assets receipts

Under Section 362, the basis of assets received by the corporation is the basis in each asset PLUS the gain recognized for each asset.

Thus, in the example in the table above, the basis to the corporation is $95,000, the basis of the assets transferred ($78,000) plus the gain recognized by the transferor ($17,000). You can use a sanity check here as well: as we determined above, there is $25,000 of deferred gain remaining on these assets. Their value is $120,000. Thus, upon the sale, in order to trigger the gain the basis would need to be $95,000.

Ancillary Considerations

As we said in the introduction, one of the times you’re most likely to use Section 351 is when you wish to convert a partnership into a corporation. The easiest way to do this is to file a Form 8832 and “check the box.” If you do that, Reg. Section 301.7701-3 provides that the result is an “assets over” transaction, in which the partnership transfers its assets to the corporation in a Section 351 transfer before then liquidating by distributing the stock out to the partners. Easy enough, right?

While a check the box election is administratively simple — it doesn’t require the partnership to undergo the actual steps, but rather provides for a formless transaction — it might not be the right choice for you. For example, what if you have liabilities in excess of the basis of the assets transferred? Section 357(c) would apply, and because the Section 351 transfer is forced in this situation, there’s nothing you could do to avoid it.

The option, then, would be to eschew a check the box election and opt instead to undergo the actual steps necessary to convert the partnership to a corporation, as provided by Revenue Ruling 84-111. For example, you could use the “assets up” method, where the partnership FIRST liquidates, and then the partners contribute the assets to the corporation in a Section 351 transfer. In this transaction, the partners could kick in the additional cash or assets necessary to overcome the Section 357 issue.

Finally, remember that sometimes, you don’t WANT a transfer of property to a corporation to be tax free. You may want to recognize a loss on the transfer. You may want to trigger gain to use an expiring (pre-2018) net operating loss. Or you might want to achieve a stepped-up FMV basis for the corporation. Or perhaps you might want to “lock in” capital gain before the corporation then converts a capital asset into ordinary income producing assets (see this article on land banking).

If you transfer the assets to the corporation for stock, you’re locked into Section 351 treatment. So if you want to force sale treatment, you’re going to want to, you know…do a sale. Sell the property for cash or property rather than stock. Have a sale agreement. You get the idea. Or, you could transfer the assets for stock pursuant to a binding written commitment to sell enough stock to drop you below the 80% control standard, taking the transaction outside the ambit of Section 351.

Time, they say, is a flat circle. Embrace it. Form a corporation. Buy a fanny pack. Watch the U.S. and Iran threaten each other with nuclear annihilation. The 80’s are back!