Skip to content

Skip to content

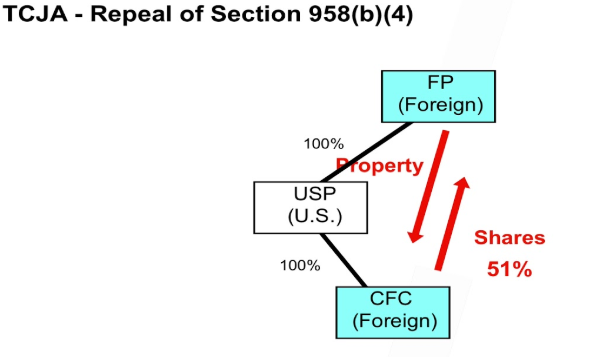

Most tax rules have unintended consequences. That much is obvious. One of the unintended consequences of the Tax

Cuts and Jobs Act (TCJA) was the repeal of Section 958(b)(4). It was repealed by TCJA in an effort to

narrowly target “de-control” transactions in which a foreign parent of a U.S.

shareholder with a CFC sheds the CFC status by acquiring the CFC’s stock.

But in effect, the full repeal of Section 958(b)(4) without additional statutory limits significantly expanded the scope of the downward attribution rules beyond what was intended. How? Let me explain.

The new tax law expanded the definition of U.S. Shareholder to include a U.S. person that owns at least 10% of the value of the CFC. The new “vote or value” U.S. Shareholder definition applies to tax years beginning after December 31, 2017, and a foreign corporation is a CFC when it is more than 50% owned by U.S. Shareholders. For this purpose, ownership is determined under the attribution rules of sections 958(a) and 958(b).

Section 958(b) generally adopts the constructive ownership rules in section 318 (with certain modifications) to attribute foreign stock ownership of one person to a related person. Before the new tax law was enacted, section 958(b)(4) turned off the downward attribution rules in 318(a)(3) such that, for example, a U.S. corporation was not considered to own stock that was owned by its foreign parent. By removing section 958(b)(4), the new statute now requires “downward attribution” from a foreign person to a related U.S. person.

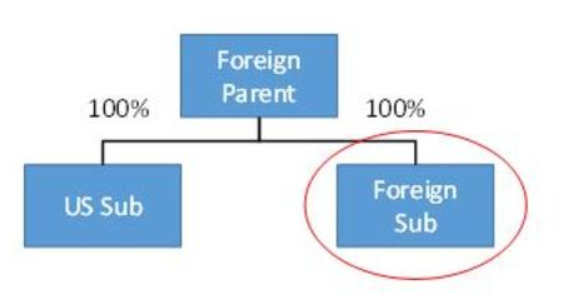

As a result of expanding the section 958(b) constructive ownership rules, the number of U.S. Shareholders and, therefore the number of CFCs, will increase.

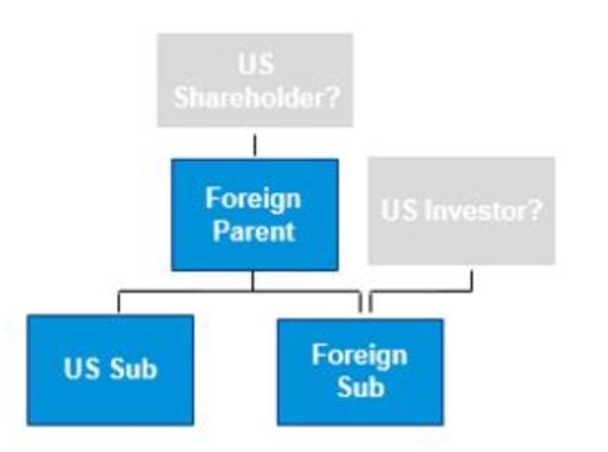

As noted in the diagram, before the repeal of section 958(b)(4), Foreign Parent’s ownership of Foreign Sub was not attributed to US Sub. However, under current section 958(b), Foreign Parent’s ownership in Foreign Sub is attributed to US Sub. Thus, Foreign Sub is a CFC in which US Sub is a U.S. Shareholder.

The section 958(b) rules do not apply, however, for purposes of determining the amount that a U.S. Shareholder includes in income under the subpart F provisions, including the new global intangible low-taxed income (GILTI) rules. As a result, notwithstanding its U.S. Shareholder status, US Sub would not be subject to tax under the subpart F regime (including GILTI) with respect to Foreign Sub because it does not own—directly or indirectly under the section 958(a) attribution rules—any interest in Foreign Sub.

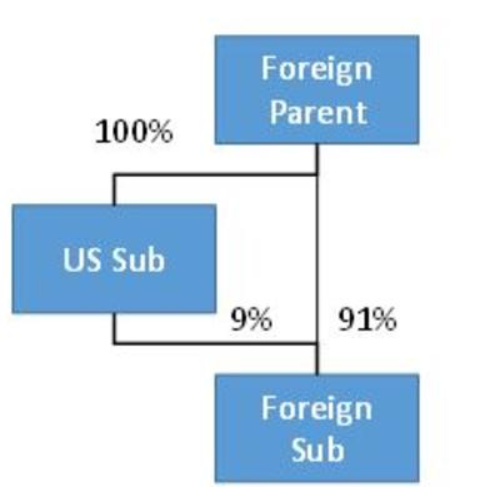

The diagram below illustrates the effect that the downward attribution rules (which apply as a result of the repeal of section 958(b)(4)) have on increasing the number of U.S. persons subject to the mandatory repatriation regime:

As a result, US Sub would have to include in income its pro rata share of Foreign Sub’s post-86 E&P pursuant to the mandatory repatriation rules, although the amount of US Sub’s mandatory repatriation inclusion would be based solely on its direct and indirect ownership (9%) of Foreign Sub, and only take into account E&P earned by Foreign Sub during periods that Foreign Sub was an SFC.

Note that foreign income taxes paid or accrued by Foreign Sub would not be attributed to US Sub’s mandatory repatriation inclusion because US Sub own less than 10% of Foreign Sub’s voting stock (as determined under the relevant rules).

But US Sub has no Form 5471 filing obligation for Foreign Sub unless US Shareholder—which would indirectly wholly own Foreign Sub—exists, or US Investor exists and owns at least 10% of Foreign Sub.

The IRS released proposed regulations (REG-104223-18) on Oct. 1 2019 addressing a number of unintended consequences brought about by the repeal of Section 958(b)(4) by the TCJA. It also concurrently released a revenue procedure (Rev. Proc. 2019-40) to help certain U.S. taxpayers determine whether a foreign corporation is a controlled foreign corporation (CFC) and calculate their Subpart F inclusions and global intangible low-taxed income (GILTI) inclusion amounts. The revenue procedure provides a number of safe harbors aimed at taxpayers that have limited ability to obtain detailed information regarding certain corporate foreign investments.

Notably, the proposed regulations do not provide broad relief for U.S. income inclusions of minority U.S. owners of foreign corporations that became CFCs solely because of downward attribution.

Talk to your tax team today to see whether these rules impact you and your organizations.