Skip to content

Skip to content

We first discussed Latin America a few years ago here –

https://www.mooresrowland.tax/2016/01/latin-american-tax-treaties-regional.html

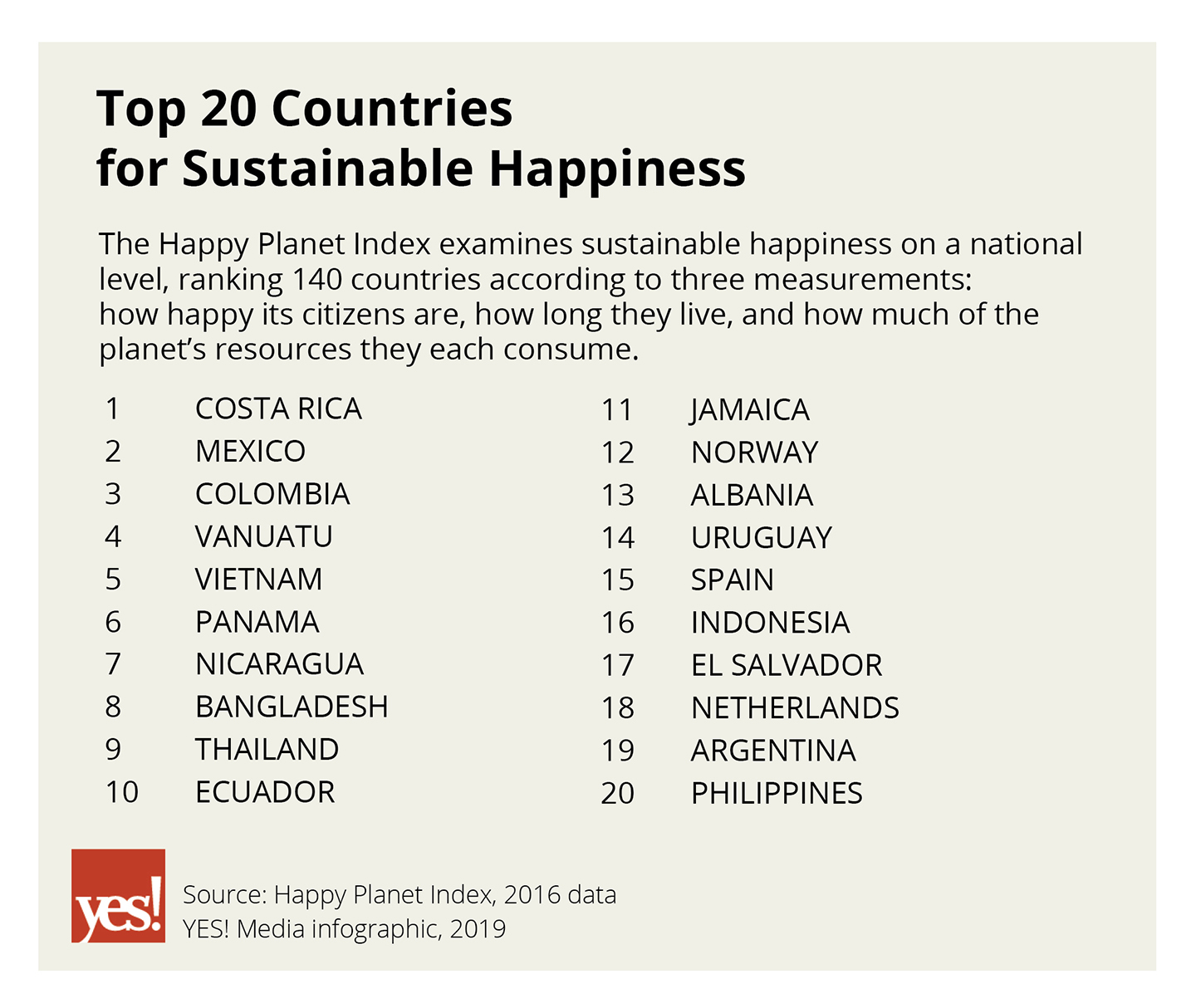

Latin America has it’s share of location independent business owners. One key attraction of Latin America is how happy a region it is. See the chart below –

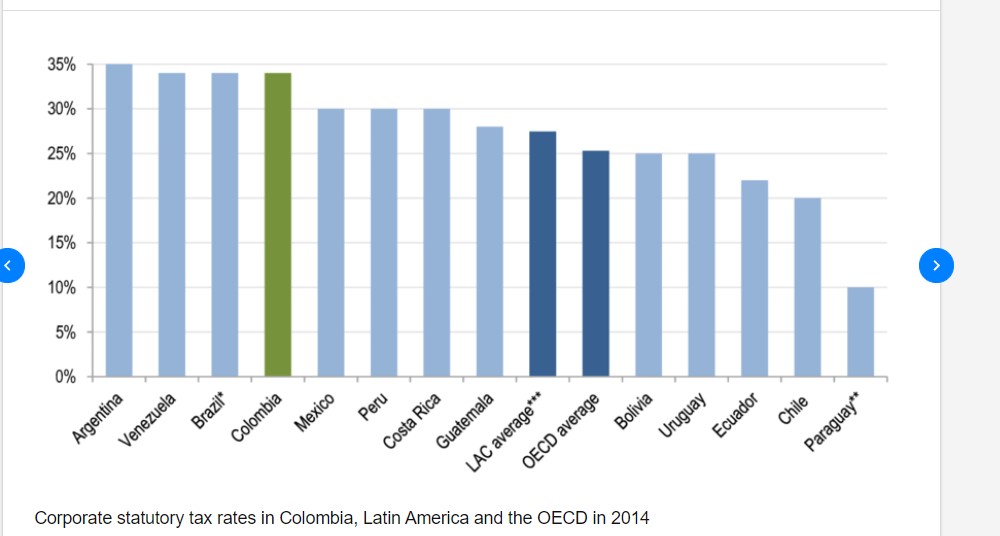

Unfortunately, Latin America is not the most tax efficient of regions. The average rates tend to be higher than Europe and Europe has pretty high tax rates –

Yes the chart above is dated but the point is well made.

It is not enough to just look at absolute corporate tax rates though. We need to consider whether the country taxes worldwide income or not. A domestic company is liable to be taxed on its worldwide

income in Argentina, Brazil, Chile, Colombia, Mexico and it is granted tax

credits for taxes paid abroad.

Fortunately, there are 5 countries in Latin America that have territorial tax regimes as opposed to worldwide tax regimes.

The following countries either have a traditional territorial tax system or elements of one at the time of this writing:

Andorra- Territorial taxation, only of nonresidents.

Angola – Territorial taxation.

Anguilla – Territorial taxation.

Bhutan – Territorial taxation.

Botswana – Territorial taxation.

Costa Rica – Territorial taxation.

Cuba – Residential taxation of citizens, territorial taxation of foreigners. Does not tax nonresidents.

Democratic Republic of the Congo – Territorial taxation.

Djibouti – Territorial taxation.

French Polynesia – Territorial taxation.

Georgia – Territorial taxation.

Gibraltar – Territorial taxation.

Guatemala – Territorial taxation.

Hong Kong – Territorial taxation.

Lebanon – Territorial taxation.

Macau – Territorial taxation.

Malawi – Territorial taxation.

Malaysia – Territorial taxation.

Marshall Islands – Territorial taxation.

Micronesia – Territorial taxation.

Namibia – Territorial taxation.

Nicaragua – Territorial taxation.

North Korea – Residential taxation of foreigners, territorial taxation of nonresidents. Does not tax income of resident citizens.

Palau – Territorial taxation.

Palestine – Territorial taxation.

Panama – Territorial taxation.

Paraguay – Territorial taxation.

Philippines – Residential taxation of citizens, territorial taxation of foreigners.

Saint Helena – Territorial taxation.

San Mari – Territorial taxation.

Saudi Arabia – Residential taxation of citizens, territorial taxation of foreigners.

Seychelles – Territorial taxation.

Singapore – Territorial taxation.

Somaliland – Territorial taxation.

Syria – Territorial taxation.

Taiwan – Territorial taxation in general, but residential taxation under the alternative minimum tax.

Tokelau – Territorial taxation.

Tuvalu – Territorial taxation.

Zambia – Territorial taxation.

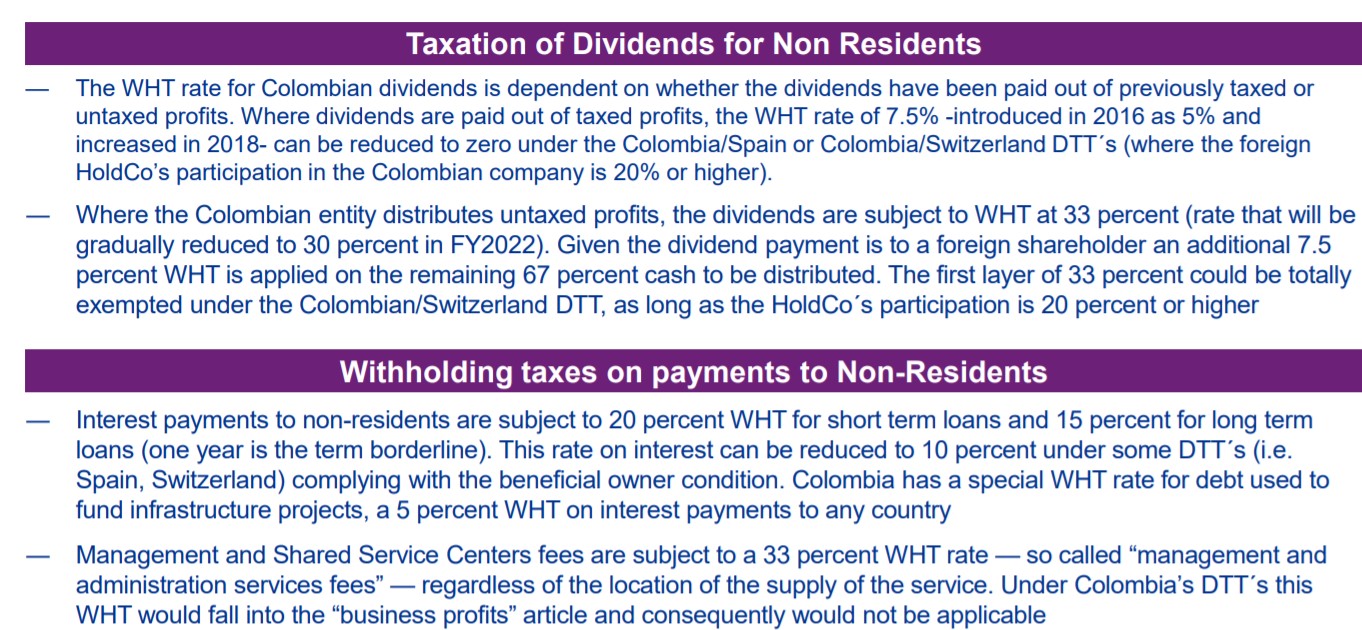

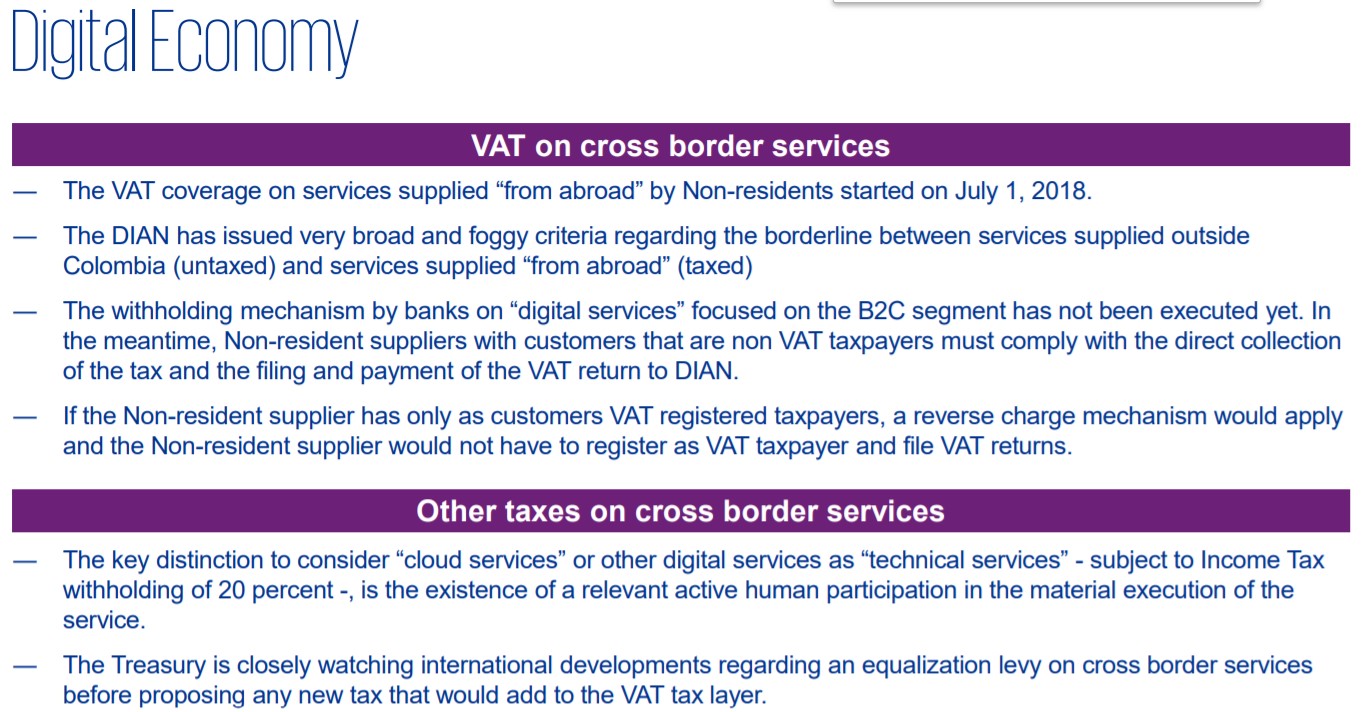

Aside from having a 33% corporate income tax rate, I will say a few on Colombia because it is a rising hub for digital nomads –

For those with PE in Colombia? Please note the following recent development –

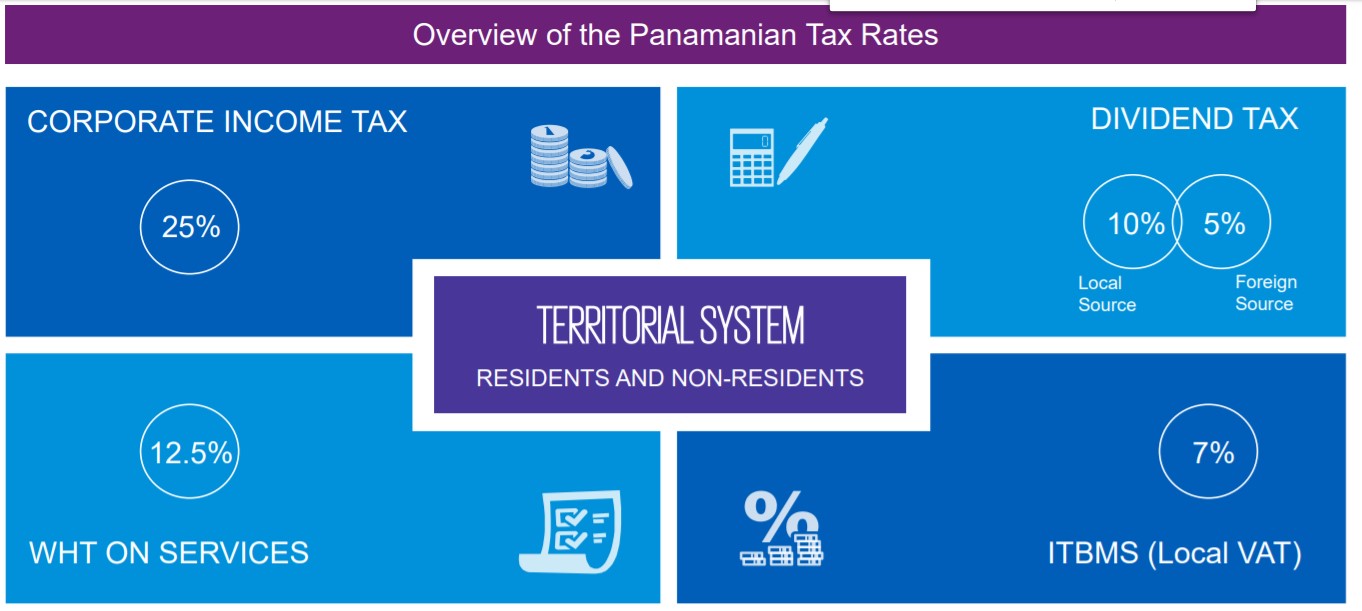

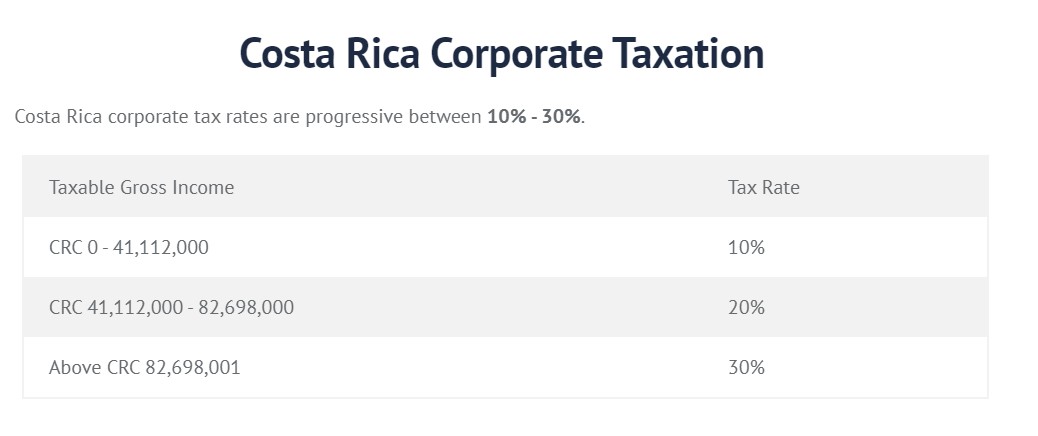

By comparison, Panama and Costa Rica are more interesting because of their territorial tax regimes –

The exchange rate is around CRC 500 to 1 USD. Under the Costa Rica tax system, residents and corporations are taxed only on income earned in Costa Rica. The tax year begins on October 1st and ends on September 30th, for both individuals and corporations in Costa Rica. Companies may request filing returns on a different tax year, subject to the approval of the Ministry of Finance. Unless proof to the contrary exists, the Ministry of Finance establishes a presumptive net income for professionals as well as corporations, and constitutes a minimum taxable base.

Branches and permanent establishments are taxed in the same way as subsidiaries.

- Taxation of dividends– Dividends received from domestic entities are exempt from corporate tax. A 15% withholding tax is levied on dividends paid to individual shareholders and 5% for dividends paid by stock corporations whose shares are registered on an officially recognized stock exchange.

- Capital gains – Capital gains are exempt unless derived from the habitual activity of the seller (i.e. the normal trade of business) or the assets sold are tangible and can be depreciated. Such gains are taxed at 30%.

- Losses – Industrial losses may be carried forward for 3 years (5 years for agricultural losses). Capital losses are deductible only if a gain on the disposal is taxable in the current year.

- Tax Rate – The rate is 10% for corporations earning less than USD 69,080; 20% for corporations earning more than USD 64,809 and less than USD 139,000; and 30% for companies earning more than USD 139,000. The tax rate is 30% for trading and non-trading companies.

- Holding company regime – No

- Tax Incentives – Industrial, processing and service companies located in free zones are entitled to a full exemption from income tax in the first 8 years of operation and a 50% exemption in the next 4 years. Forest sustainability incentives and tourism incentives also are available.

- Costa Rica has a special program called the free trade zone regime, which grants a 100% exemption status to companies that meet minimum fixed-asset investment requirements and that are foreign-market oriented.

- The rate of General Sales Tax (GST) in Costa Rica is 13%.