Skip to content

Skip to content

#Estonia is a jurisdiction often discussed among #entrepreneurs

and #businessowners. It is especially popular

with #locationindependent entrepreneurs or #digitalnomads.

Estonia is the only country in the EU where corporate

profits are not subject to current income tax. Instead a corporate income tax

is imposed only upon the payment of a dividend to the company’s shareholders.

Unfortunately there is much misunderstanding.

Here are 7 key points to consider before

using Estonia as a jurisdiction in your corporate structure.

- If you’re US exposed, and control an Estonian

entity, you may not be able to defer taxation until profit distribution because

of Subpart F and GILTI rules. In fact, because

of Subpart F and GILTI, distributions may be taxed at ordinary rates despite

the US – Estonia Tax Treaty –https://www.mooresrowland.tax/2018/02/us-exposed-owner-of-international.html - If you’re US exposed, and are a shareholder in

an Estonia entity (may be a minority shareholder), you may not be able to

invoke the benefits of the US – Estonia Tax Treaty because of Article 22 or the

Limitation on Benefits clauses. Here’s a

link to the treaty and please pay attention to the residency rules –https://www.irs.gov/pub/irs-trty/estonia.pdf - Being an e-resident of Estonia is not the same

as being tax resident or resident for immigration purposes. https://learn.e-resident.gov.ee/hc/en-us/articles/360000721597-Estonian-tax-basics - If you are a controlling person of an Estonia

entity and are tax resident elsewhere, then you may create nexus or permanent

establishment (depending on whether or not, you reside in a treaty

jurisdiction) in your country of residence and local tax rules may apply to

both yourself and the Estonia entity. If

this happens, then both the country of effective management and Estonia will

want to tax the worldwide income of the Estonia company. Be careful -https://learn.e-resident.gov.ee/hc/en-us/articles/360000721597-Estonian-tax-basics - Should you decide to be properly tax resident in

Estonia, please note that, like most of Europe, they tax residents on 100% of their

worldwide income https://learn.e-resident.gov.ee/hc/en-us/articles/360000721597-Estonian-tax-basics - Taxes may be due on Director’s fees (if any) https://www.emta.ee/eng/business-client/income-expenses-supply-profits/tax-rates

- If you cross the threshold, which is presently

turnover in excess of EUR40k, then VAT becomes payable – https://learn.e-resident.gov.ee/hc/en-us/articles/360000871738-VAT-registration

Now let’s get into the details of Estonia.

Estonia is not a tax haven – https://medium.com/e-residency-blog/heres-why-tax-evaders-are-disappointed-in-estonian-e-residency-2322644f5f59

Some see Estonia as the number one start-up technology country in Europe and one of the

top in the world. The most recognizable technology company with Estonian

roots is Skype, which was acquired by Microsoft in 2011 for $8.5

billion.

There are a number of reasons why a country as small as Estonia is

producing this many technology companies, including a stable economic

environment (i.e., Estonia’s economic freedom is regarded as one of the highest in

the world and the best in the Central and Eastern European (CEE)

region); the population of Estonia has the highest average level of education

in the CEE region; and the country is supported by a tech-savvy government (an

example of this is Estonia’s “e-residency” program, which allows non-residents

to establish local businesses and bank accounts, and operate them remotely

after only a single visit to Estonia).

Another significant advantage offered to companies doing business

in Estonia is its unique corporate income tax system. Estonia

is the only country in the EU where corporate profits are not subject to

current income tax. Instead a corporate income tax is imposed only upon the

payment of a dividend to the company’s shareholders (and upon payments deemed

equivalent to dividends, such as certain gifts and donations, fringe benefits

to employees, etc.) This allows companies to defer paying corporate income tax

indefinitely so long as the profits are retained or reinvested. Once a dividend

payment is made, a flat corporate income tax will be imposed at the effective

rate of 20 percent.

https://learn.e-resident.gov.ee/hc/en-us/articles/360000721597-Estonian-tax-basics

It is important to note that, while the corporate income tax is triggered

upon the payment of a dividend, the tax is imposed on the corporation itself,

not the shareholder. Therefore, it cannot be reduced pursuant to the EU

parent-subsidiary directive or an income tax treaty that Estonia is a party to

(although the corporate income tax can be reduced by any income tax withheld on

payments received by an Estonian entity).

Profits can, however, be repatriated without triggering corporate

income tax if the amounts are paid in the form of interest, royalties or other

types of payments, so long as they are not actual or deemed dividends. Profits

also may be loaned to third parties or within corporate groups without

triggering corporate income tax, which allows for tax efficient opportunities

for intra-group finance activities. Note

that proper Transfer Pricing policies may be advisable

Other notable tax benefits available in Estonia include the lack of

thin capitalization rules (i.e., no debt to equity requirements); no

withholding tax on interest or dividends to non-residents (or on royalties

paid to EU residents or Switzerland); and a wide network of income tax treaties

with countries around the world.

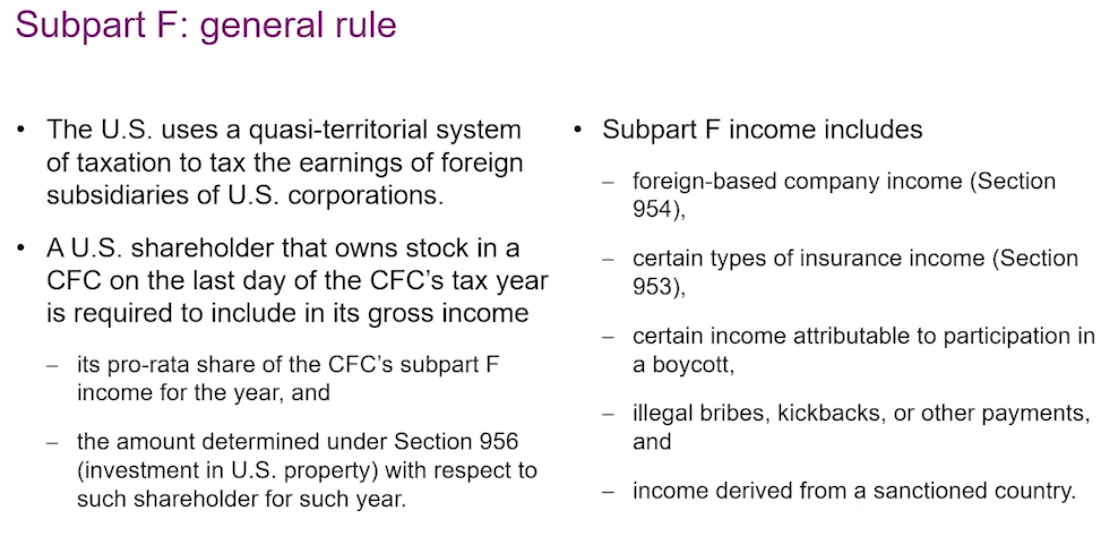

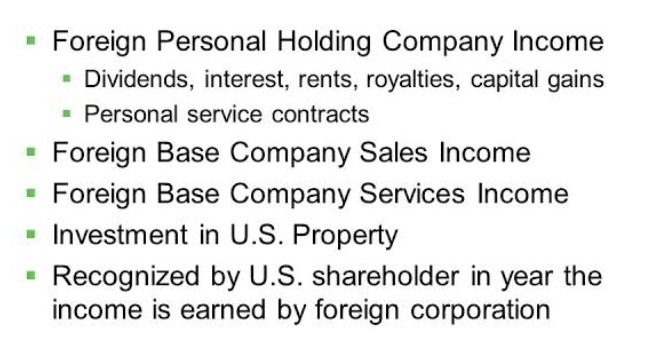

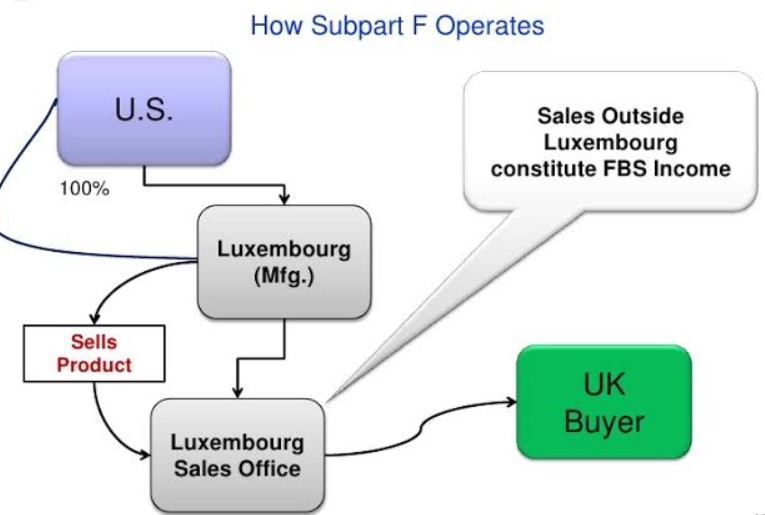

Use in U.S. Tax Planning

Income earned through a U.S.-controlled foreign corporation typically

will not be subject to U.S. federal income tax until such time as its profits

are repatriated to the United States in the form of a dividend. An important

exception to this rule exists for income classified as “subpart F” income under the controlled foreign

corporation (CFC) rules.

Talk to your adviser before making important financial decisions