Skip to content

Skip to content

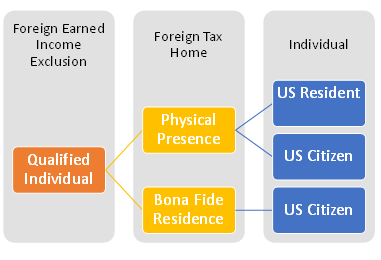

When talking about the Foreign Earned Income Exclusion or FEIE, everyone understands the PPT or Physical Presence Test. The BFT or the Bona Fide Residence test requires more effort to understand.

I had previously written of the Section 911 exclusion here – https://www.mooresrowland.tax/2013/12/us-employee-working-in-iraq-and.html

Here’s another recent article…..

Pilot grounded on foreign income exclusion

The Tax Court held that a pilot who worked for Korean Air and lived at a hotel in South Korea while there for his job was not entitled to the Sec. 911 foreign earned income exclusion because he had not proved that he was a bona fide resident of South Korea for purposes of the exclusion.

Background

Robert Hudson was a commercial airline pilot who flew 26 years for Northwest Airlines before retiring in February 2007. Under the terms of his pension, Hudson was able to work as a pilot for another airline while receiving his pension payment, and after he retired from Northwest, he sought employment with another airline.

He looked for a position with foreign airlines because of these airlines’ policies of maintaining the seniority of pilots. These airlines required that applications for employment as a pilot be submitted through a recruiting agency. Hudson chose to use the agency Global Airline Pilots (GAP).

Through GAP, Hudson submitted an application to Korean Air, and the company ultimately offered Hudson a job as a pilot, which he accepted. On March 19, 2007, he entered into an agreement with GAP (GAP agreement) which stated that he was an independent contractor and was not an employee or agent of GAP and that his flight base was in South Korea. The contract had a term of five years. At the beginning of his employment with Korean Air, Hudson intended to work for the airline for 5½ years until he reached mandatory retirement age and to return to the United States after he retired. However, he ended up retiring from Korean Air at the end of the contract because he failed a physical exam.

During his time with Korean Air, Hudson was based in Incheon, South Korea. Hudson became a registered alien of South Korea and lived in a Hyatt Hotel owned by Korean Air, with the company paying for his lodging. He stored large suitcases of his belongings at the hotel while he was away and would have these belongings brought to his room upon check–in.

Hudson spent considerable amounts of time in South Korea while flying routes for Korean Air. However, he received nine days off a month, typically in blocks, and 24 vacation days a year. During the years he worked for the airline, he spent as much of his time off as possible in the United States with his wife, Eleanor. Eleanor lived during the summer and fall in Minnesota, where the couple owned a home, and the rest of the year in Arizona, where they owned a second home. She also sometimes traveled to places where Hudson spent his layovers between flights.

Korean Air paid Hudson’s salary to GAP, which paid it to Hudson after deducting Korean withholding and fees Hudson owed GAP for its services. Hudson received an annual Korean tax statement listing him as a “nonresident,” and he did not view himself as a permanent resident of South Korea but as a registered alien paying Korean taxes. In addition, when he signed the contract, Hudson consulted an attorney who advised him that by signing the contract he became an employee of Korean Air.

Hudson prepared his returns for 2007 through 2010 with the assistance of a preparer recommended by GAP. Based on the preparer’s advice, Hudson excluded his income from the airline under the foreign earned income exclusion in Sec. 911. For 2011 and 2012, he hired a Minnesota CPA to prepare his returns and also consulted an attorney regarding his eligibility for the foreign earned income exclusion. The attorney advised him, based on his answers to a questionnaire provided by the attorney, that he was entitled to the exclusion, and his income from the airline was excluded from gross income on both his 2011 and 2012returns.

Unfortunately, the IRS did not agree with this position. In a notice of deficiency, the IRS disallowed Hudson’s foreign earned income exclusions for both tax years because of his failure to establish either bona fide residence or physical presence in a foreign country for the relevant period. It also determined that he was liable for self–employment tax on his airline income. Hudson challenged the determination in Tax Court.

Sec. 911

Sec. 911(a) allows a “qualified individual” to exclude from gross income “foreign earned income.” Foreign earned income is “the amount received by such individual from sources within a foreign country or countries which constitute earned income attributable to services performed by such individual.” A qualified individual is defined in Sec. 911((d) as an individual whose tax home is in a foreign country and who is either a bona fide resident or physically present in the country for a certain time.

The Tax Court’s decision

The Tax Court held that Hudson was not entitled to the foreign income exclusion for his income from Korean Air. Hudson did not argue that he had been in South Korea for a sufficient amount of time to satisfy the physical presence test, so the court analyzed whether Hudson qualified for the exclusion under the bona fide resident test.

In its analysis, the Tax Court used the factors set out by the Seventh Circuit in Sochurek, 300 F.2d 34 (7th Cir. 1962). These factors include:

- intention of the taxpayer;

- establishment of his home temporarily in the foreign country for an indefinite period;

- participation in the activities of his chosen community on social and cultural levels, identification with the daily lives of the people and, in general, assimilation into the foreign environment;

- physical presence in the foreign country consistent with his employment;

- nature, extent, and reasons for temporary absences from his temporary foreign home;

- assumption of economic burdens and payment of taxes to the foreign country;

- status of resident contrasted to that of transient or sojourner;

- treatment accorded his income status by his employer;

- marital status and residence of his family;

- nature and duration of his employment; whether his assignment abroad could be promptly accomplished within a definite or specified time;

- good faith in making his trip abroad; whether for purpose of tax evasion. [Sochurek, 300 F.2d at 38]

The Fifth Circuit in Jones, 927 F.2d 849 (5th Cir. 1991), opined that the most significant of these factors is the taxpayer’s intent. The Tax Court adopted this position in Cobb, T.C. Memo. 1991–376, citing the Fifth Circuit in Jones.

Hudson argued that his situation was analogous to those of the taxpayers in Jones and Cobb, in which the courts applied the Sochurek factors and found that the taxpayers, who were pilots for Japan Airlines (JAL), met the bona fide resident test. In both cases, the taxpayers lived in hotels in Japan, had families residing in the United States, had made no significant attempts to integrate into Japanese culture, and paid Japanese income tax. In addition, the taxpayer in Jones was away from Japan only when work required or he was on vacation, and the taxpayer in Cobb was only in the United States for flight layovers, during which he frequently visited his family.

However, both taxpayers testified credibly that they intended to be residents of Japan during their employment with JAL. In addition, the taxpayer in Jones had once turned down a dividend check from the state of Alaska (where he had previously lived) because he said he was not a resident of Alaska, and the taxpayer in Cobb had documentary evidence of his intent to be a Japanese resident. The courts held in both cases that the taxpayers intended to be residents of Japan and, based on the Sochurek factors, were bona fide residents.

The Tax Court found that, while the facts of the taxpayers in Jones and Cobb were similar to Hudson’s, and Hudson credibly testified that he intended to work for Korean Air until his retirement, he had not proved that he intended to be anything more than a transient and had demonstrated that he always intended to return to the United States. Thus, applying the Sochurek factors, Hudson was not a bona fide resident.

The critical difference, according to the court, was that Hudson, unlike the taxpayers in Jones and Cobb, intended to spend all of his time off work during the years he worked for Korean Air in the United States and had spent as many as 132 days a year in the United States. Citing Vento, 715 F.3d 455 (3d Cir. 2013), the court found that extensive absences, unless justified by good–faith reasons (e.g., travel requirements of the taxpayer’s profession) would negate a finding of bona fide residency. Thus, it concluded that his extended absences from South Korea, along with his limited contacts with Korean culture, precluded a finding that Hudson was a bona fide resident of SouthKorea.

Reflections

Over the summer, the Tax Court decided another Korean Air pilot’s foreign earned income exclusion case on similar grounds (Acone, T.C. Memo. 2017–162). As the number of cases dealing with this issue shows, the question of whether a pilot working for a foreign airline qualifies for the foreign earned income exclusion is not an isolated issue. When it arises, the taxpayer often leaves it to a practitioner to decide whether the exclusion applies. Based on the various cases, it is clear that verifiable actions (such as the taxpayer’s refusal of Alaska fund dividends in Jones) that objectively show an intent to be a resident of the country the taxpayer is living in for work can go a long way toward proving the taxpayer passes the bona fide residency test under the Sochurek factors.

Thus, a practitioner who becomes aware that a client is going to work for a foreign airline (or any foreign company) under terms similar to Hudson’s should be proactive and inform the client upfront, based on the case law, what the client can do to help ensure that the foreign earned income exclusion will apply to his or her compensation income.

Hudson, T.C. Memo. 2017–221

Source: https://www.thetaxadviser.com/issues/2018/jan/pilot-grounded-foreign-income-exclusion.html