Skip to content

Skip to content

Introduction

The UAE is a constitutional federation formed on 2 December 1971 between the seven emirates of Abu Dhabi, Dubai, Sharjah, Ajman, Fujairah, Umm al-Quwain and Ras al Khaimah. Formerly a part of the British protectorate known as the “Trucial States” or “Trucial Oman,” the emirates gained autonomy when the British withdrew from the Gulf region in 1971. The UAE is strategically located in the Arabian Peninsula and covers an area of approximately 82,880 square kilometers. It shares borders with Saudi Arabia, lying at the southwest of the country, and Oman, situated at the north and southeast of the UAE. The country also lies between the Arabian Gulf and the Gulf of Oman.

Arabic culture is part of everyday life in the UAE and it influences the country’s business norms. The country is largely open to foreigners and strives to create an environment that is favorable to foreign investment and economic growth, and which promotes tolerance, diversity and multiculturalism. The population of the UAE is estimated to be 9.4 million. Approximately 80% of the population is composed of expatriates, with a large percentage residing in Dubai. Arabic is the country’s official language—however, English is generally used in business and everyday life. Hindu, Urdu and Persian are also widely spoken. The majority of the population is Muslim. The UAE is a dynamic hub for global commerce and has won the right to host the World Expo in Dubai in 2020. This will be the first time that the World Expo is staged in the Middle East, North Africa or South Asia.

But I don’t want to talk about Dubai in general. I want to discuss Dubai from a tax and privacy perspective.

Business

Businesses operating in Dubai are not allowed to be controlled by foreigners and are subject to restrictions. The UAE implements a legal framework of free zones which foster an attractive environment for businesses by offering companies—primarily 100% foreign-owned companies— incentives such as zero tax rates on their income and exemption from foreign exchange controls. However, free zone companies are subject to a number of restrictions and are only permitted to conduct their activities within the vicinity of the respective free zone. Such free zones include economic free zones, such as the JAFZA, and financial free zones, such as the DIFC and, more recently, the ADGM. These restrictions should be carefully considered by investors when evaluating whether incorporating a company in a free zone is consistent with their objectives.

Taxation and VAT

The UAE does not currently have a federal tax system. Individual emirates have passed their own tax

decrees dealing with corporate income tax but corporate income tax is only imposed on oil companies and branches of foreign banks. There is currently no sales tax or value added tax in the UAE (you may check the article about American tax Dubai). However, the GCC countries

announced in February 2016 that a unified value added tax at the rate of 5% will be imposed by 1

January 2018 or 1 January 2019, depending on the readiness of the respective GCC country, and

draft legislation is underway.

There are no personal income taxes in the UAE. Only government employees are required to pay

social insurance contributions. However, it is worth noting that individuals may be subject to other fees

or levies. For instance, the Dubai Municipality applies a housing fee amounting to 5% of the annual

rental value of property leased by Dubai residents, payable alongside the water and electricity bill.

There are no capital gains taxes levied on the sale of shares. Real estate transfer tax, referred to as

“registration fees,” is levied on the transfer of ownership of real estate in the UAE (including where

there is an indirect transfer in a company holding real estate in the UAE). The amount varies

depending on the emirate and the location of the real estate. In Dubai, the transfer tax is currently 4%,

although the DIFC charges 5%.

The UAE has entered into an extensive network of treaties to ensure the avoidance of double

taxation.

Moreover, the UAE became a FATCA partner in 2015 and signed an intergovernmental agreement

with the United States setting out guidelines for the application of FATCA by financial institutions

regulated by the UAE Central Bank, the Insurance Authority, the ESCA and the DIFC.

Privacy

As banks in the UAE turn more demanding, many are using ‘insurance wrappers’ and the time-tested services of nominee directors to ensure privacy.

For opening accounts of companies, banks in Dubai are insisting on the tax ID of the home country, copies of passport, and, occasionally, the presence of shareholders of these entities. Banks, according to an expert in foreign currency regulations, are taking more than a month to open accounts compared to 3-4 days before.

Since early 2016, banks are looking into remittances to and from entities in the UAE Free Trade Zone, while the UAE central bank is questioning so-called pass through transactions. CRS begins in the UAE from January 2018.

Clearly regulations are tightening but Dubai does not yet have any requirement for entities to maintain a register like Hong Kong and Singapore. Is Dubai more attractive than other jurisdictions such as Hong Kong and Singapore when it comes to privacy?

Hong Kong

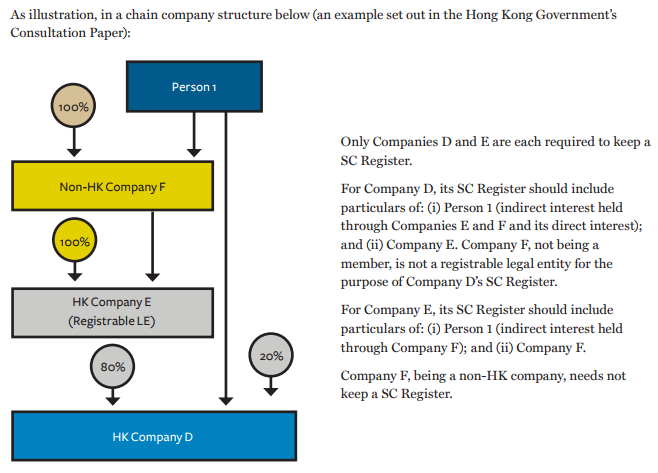

The Companies (Amendment) Bill 2017 (“Bill”) requires Hong Kong companies to keep and maintain a register of significant controllers (“SC Register”). The Bill was published together with the Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) (Amendment) Bill 2017. The intention is to bring Hong Kong’s regulatory regime up to date in line with international requirements as promulgated by the Financial Action Task Force (FATF), an inter-governmental body that sets international standards on combating money laundering and terrorist financing.

Only companies “formed and registered” under the Hong Kong Companies Ordinance, with limited exceptions, will be caught. Non-Hong Kong companies, despite having registered in Hong Kong, are not required to keep a SC Register. This echoes the position stated in the Hong Kong Government’s Consultation Conclusion of April 2017, which says “… as regards foreign companies registered in Hong Kong, we are mindful that they may be subject to disclosure requirements of the jurisdictions in which they are incorporated. To place these companies under the proposed regime may dissuade them from coming to Hong Kong for fear of regulatory overlap…” (paragraph 2.8).

Other exceptions to the requirement of keeping a SC Register under the Bill are listed companies (which are yet subject to disclosure requirements under the Securities and Futures Ordinance) or companies that fall within a type or class of companies exempted by future regulation. In other words, save for the mentioned exceptions, dormant companies, financial institutions, charitable organisations and any other types of companies incorporated in Hong Kong (“applicable companies”) will each be required to keep a SC Register.

A person has significant control if it:

1. holds, directly or indirectly, more than 25% of the shares;

2. holds, directly or indirectly, more than 25% of the voting rights;

3. holds, directly or indirectly, the right to appoint or remove a majority of the board of directors;

4. has the right to exercise or actually exercises, significant influence or control; OR

5. has the right to exercise or actually exercises, significant influence or control over a trust or firm which is not a legal person, but whose trustees or members meets one or more of the conditions specified above.

Singapore

The Companies (Amendment) Act 2017 requires Singapore companies and limited liability partnerships, as well as foreign companies registered to do business in Singapore, to keep registers of significant controllers and nominee directors. Other amendments include changes to the requirement for Singapore companies to execute deeds by affixing their common seal.

The requirement to keep registers of significant controllers and nominee directors applies to the following entities:

- All companies and limited liability partnerships (LLP) incorporated / registered in Singapore will be required to maintain registers of controllers and registers of nominee directors at prescribed places (e.g. company’s registered office).

- Foreign companies registered in Singapore will also be required to maintain registers of controllers but not registers of nominee directors.

Entities exempted from the requirements include Singapore-incorporated companies listed on an approved exchange, Singapore financial institutions, and their wholly-owned subsidiaries. Also included in the exemption are companies (Singapore as well as foreign) listed on a foreign securities exchange with regulatory disclosure requirements and requirements relating to adequate transparency in respect of beneficial owners. For such companies, however, their wholly-owned subsidiaries are not exempted.

The registers will not be open to inspection by the public but must be available for inspection by the Accounting and Corporate Regulatory Authority (ACRA) and law enforcement authorities. For a company, a controller is an individual or corporate body that has a significant interest in, or significant control over, it:

- A person has “significant control” if he has the right to appoint or remove a majority or directors or has the right to exercise (or actually exercises) significant influence or control over matters that may be prescribed.

- A person has “significant interest” if he has an interest more than 25% of the shares held and/or 25% of voting rights. In determining whether a person has an interest in shares, the tests set out in section 7 of the Companies Act apply.

The application of these rules to determine whether a particular person appears on a company’s register of registrable controllers can be complex.

Find out more about our US tax experts in Hong Kong and US tax experts in Dubai, UAE.