Skip to content

Skip to content

One frequent complaint from expat American citizens and Green Card holders arises when they marry a non American (known as a a Non Resident Alien or NRA). For many newlyweds, Married Filing Separately is the default option. Unfortunately, compared to other filing status, this could definitely be less tax efficient.

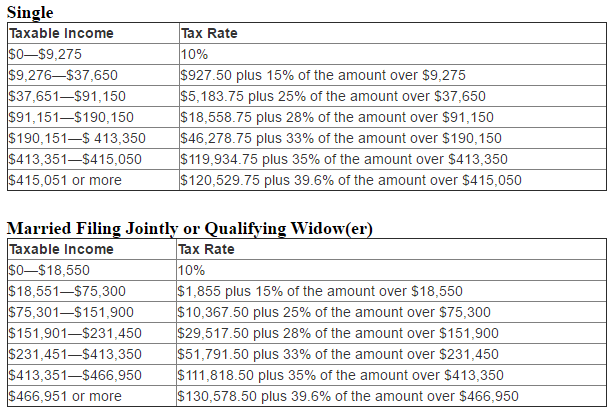

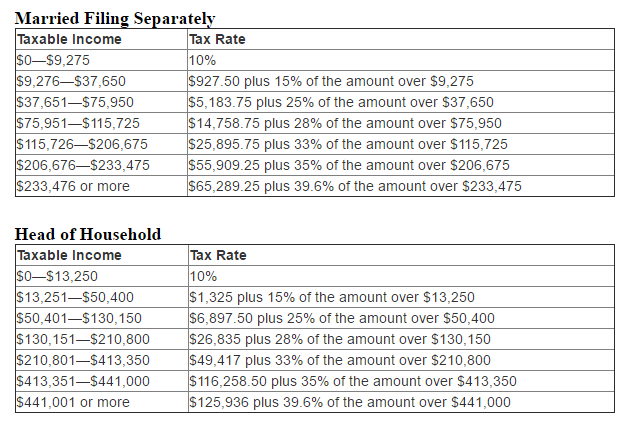

Have a look here for 2016 rates –

One alternative is to consider filing jointly or head of household. Jointly isn’t always an attractive option as most NRAs do not like being exposed to the US tax net. Head of Household is often more attractive.

How do you qualify for Head of Household even if you’re married?

If a taxpayer’s spouse was a nonresident alien at any time during the tax year, and the taxpayer did not choose to treat the nonresident alien spouse as a resident alien, the taxpayer was unmarried for head of household purposes. (IRC § 2(b)(2)(C).)

Only the following relatives can qualify an unmarried taxpayer for head of household filing status.

a. The taxpayer’s birth child, stepchild, grandchild, or adopted child who was:

(1) Single on the last day of the tax year, or

(2) Married on the last day of the tax year, if the taxpayer is entitled to a dependent exemption credit for the child.

(IRC § 2(b)(1)(A)(i).)

b. The taxpayer’s foster child for whom the taxpayer was entitled to a dependent exemption credit.

(IRC §§ 2(b)(1)(A)(ii) and 152(b)(2); Rev. Rul. 84-89, 1984-1 C.B. 5; Treas. Reg. § 1.2-2(b)(3)(ii).

See sections 24 to 26, Foster Child.)

c. Any of the following relatives of the taxpayer for whom the taxpayer is entitled to a dependent exemption credit.

Parent

Grandparent

Sister

Brother

Half-sister

Half-brother

Stepsister

Stepbrother

Stepmother

Stepfather

Daughter-in-law Son-in-law

Sister-in-law Brother-in-law

Mother-in-law Father-in-law

Aunt

Uncle

Niece

Nephew

NOTE: An aunt or uncle must be the sister or brother of the taxpayer’s mother or father. A niece or nephew must be the son or daughter of the taxpayer’s sister or brother. (IRC § 2(b)(1)(A)(ii); Treas. Reg. § 1.2-2(b)(3)(ii).)

Talk to your US qualified tax professional today