Skip to content

Skip to content

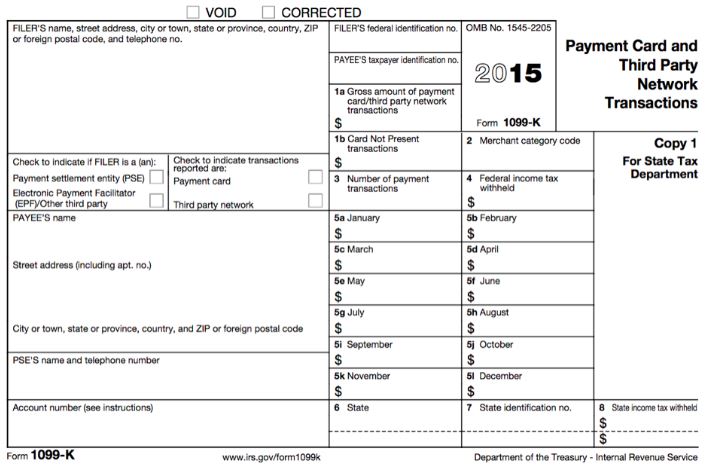

Form 1099-K, Payment Card and Third Party Network Transactions, is an IRS information return used to report certain payment transactions to improve voluntary tax compliance. You should receive Form 1099-K by January 31st if, in the prior calendar year, you received payments:

- from payment card transactions (e.g., debit, credit or stored-value cards), and/or

- in settlement of third-party payment network transactions above the minimum reporting thresholds of –

- gross payments that exceed $20,000, AND

- more than 200 such transactions

What does my Form 1099-K report to me?

A Form 1099-K includes the gross amount of all reportable payment transactions. You will receive a Form 1099-K from each payment settlement entity from which you received payments in settlement of reportable payment transactions. A reportable payment transaction is defined as a payment card transaction or a third party network transaction.

- Payment card transaction means any transaction in which a payment card, or any account number or other identifying data associated with a payment card, is accepted as payment.

- Third party network transaction means any transaction that is settled through a third party payment network, but only after the total amount of such transactions exceeds $20,000 and the aggregate number of such transactions exceeds 200.

The gross amount of a reportable payment does not include any adjustments for credits, cash equivalents, discount amounts, fees, refunded amounts or any other amounts. The dollar amount of each transaction is determined on the date of the transaction.

NOTE: The minimum reporting thresholds of greater than $20,000 and more than 200 transactions apply only to payments settled through a third-party network; there is no threshold for payment card transactions.

What should I do with this information?

It is important that your business books and records reflect your business income, including any amounts that may be reported on Form 1099-K. You must report on your income tax return all income you receive from your business. In most cases, your business income will be in the form of cash, checks, and debit/credit card payments. Business income is generally referred to as gross receipts on income tax returns. Therefore, you should consider the amounts shown on Form 1099-K, along with all other amounts received, when calculating gross receipts for your income tax return.

In addition —

- Check your payment card receipt records and merchant statements to confirm that the amount on your Form 1099-K is accurate

- Review your records to ensure your gross receipts are accurate and reported correctly on your income tax return

- Determine whether you have reported income from all forms of payment received, including cash, checks, and debit, credit and stored-value card transactions.

- Maintain documentation to support both the income and deductions you report on your income tax return

Do any of these statements apply to the Form(s) 1099-K you received?

- The Form 1099-K does not belong to you or is a duplicate

- The payee Taxpayer Identification Number (TIN) is incorrect

- The gross amount of payment card/third party network transactions is incorrect

- The number of payment transactions is incorrect

- The Merchant Category Code (MCC) does not correctly describe your business

If so, consider the following:

- If the Form 1099-K does not belong to you, contact the Payment Settlement Entity (PSE) listed on the Form 1099-K to try determine why you received the document. The name and telephone number should be shown in the lower-left part on the form. If a PSE name and number are not shown, contact the Filer at the number shown in the upper-left corner on the form. Retain any correspondence with the PSE

- If there is an error on the form, request a corrected Form 1099-K from the PSE. Keep a copy of any corrected Form 1099-K you receive with your records as well as any correspondence with the PSE

What should I do when the total gross payment amount shown on Form 1099-K does not belong to me?

In some cases, the total gross payment amount on Form 1099-K may not belong to you. The following examples illustrate such situations and provide information that may help you determine how to account for the amount of gross payments shown on the Form 1099-K you received.

- If you report your business income on Form 1120, 1120S or 1065 and you receive a Form 1099-K in your name:

- If you report your business income on a Form 1120, 1120S or 1065 and you receive a Form 1099-K in your name as an individual (showing your social security number), contact the PSE listed on the Form 1099-K to request a corrected Form 1099-K showing the business’s TIN. In addition, request that the PSE use the business’s TIN on all future Forms 1099-K. Report the income from the Form 1099-K along with any other sources of income on the appropriate income tax return. Retain all correspondence with the PSE to show that this error was corrected.

- If you shared your credit card terminal with another person or business:

- If you shared your credit card terminal with another person or business, your Form 1099-K will include payment card transactions belonging to the person or business that shared your terminal, in addition to your own payments. Where required, you should file and furnish the appropriate information return (e.g., Form 1099-K or 1099-MISC) for each person or business with whom you shared a card terminal. The information return should include the total payment card transaction amount in addition to any other income belonging to the other person or business. You should retain records of payments issued to each person or business sharing your terminal, including but not limited to shared terminal written agreements and cancelled checks.

- If you bought or sold your business during the year:

- If you bought or sold your business during the year, your Form 1099-K may include payments for transactions made before you purchased or after you sold the business. This can occur when the tax identification number and business name associated with a credit card terminal are not updated with the new owner’s information. You should request a corrected Form 1099-K from the PSE/Filer listed on the form. Its name and telephone number are on the form. Also keep a copy of corrected Form(s) 1099-K with your records and retain the purchase or sales agreement that substantiates the timing of the ownership change.

- If you changed your business entity structure during the year:

- If you changed your business structure during the year, such as incorporating or converting from a sole-proprietorship (Schedule C) to a partnership (Form 1065), or vice versa, and continued using the same card terminal, the amount shown on the Form 1099-K will not correspond with your new entity’s tax return. Be sure to timely notify your merchant acquirer of any change to the name and tax identification number that links the terminal to your current business structure. Be sure to maintain documentation to support the correct income and deductions for both business entities.

- If you allow your customers to receive cash back when they use their debit cards for purchases:

- If you allow your customers to receive cash back when they use their debit cards for purchases, the Form 1099-K you receive will include those cash back amounts as part of the gross amount of payment card transactions. Generally, you would not include cash back amounts as part of your business’s gross receipts on your income tax return, nor would you claim such amount paid to a customer as a business expense. It is important that you maintain records of customer cash back activity over the course of your tax year.

- If your business (or businesses) has multiple sources of income:

- If your business (or businesses) has multiple sources of income, you may report business income on more than one line of a return or on multiple returns or schedules. For example, assume you operate a retail business and also have rental income. You accept payment cards for both businesses, but because you have only one credit card terminal to process these transactions, your 1099-K will include gross payment card receipts for both businesses. You should use your books and records to ensure that all gross receipts are reported on the appropriate line or schedule. In this case, the gross receipts from the retail business should be reported on Schedule C, and the amounts related to the rental activity included in the rental income reported on the Schedule E.

More InfoIf you have questions about the amount reported, contact the filer (see the upper left corner of Form 1099-K). If you have questions about the merchant or third party transaction network, find the contact in the lower left corner of Form 1099-K.

- FAQs on Payment Card and Third Party Network Payments

- 1099-K Reporting Requirements for Payment Settlement Entities

- Third Party Reporting Information Center

https://www.irs.gov/businesses/understanding-your-1099-k